Churchill Downs Entrance – Kentucky Derby Broadening apeak by adding three major upscale club facilitieds. google

Above: Reversing a 60-year trend, CHDN’s investments in reviving racing have contributed to thoroughbred racing’s revival.

We have watched the shares of Churchill Downs Incorporated (NASDAQ:CHDN) for seven years since June 2017, when it traded at $57.10. In the early months post-covid ’21 it moved to $114.78. At writing, it has nudged up $135 today. This has been a nice run for long-time holders. CHDN has traded above $100 since ’21. The rationale has been built off the sustaining solid performance of this niche gaming operator in producing accelerating earnings from what is essentially a small footprint in the overall gambling sector.

Google

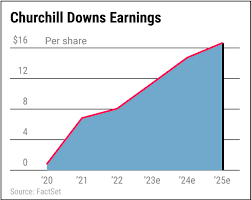

Above: Slow and steady is winning the earnings race over 12 years or more.

CHDN has achieved consistent revenue and net income growth over more than ten years from three business units: Live and historical racing from 12 tracks, including the eponymous Churchill Downs track, home of the Kentucky Derby. The unit produces over 42% of the total annual revenues.

Twin Spires—The company’s online race betting site, which also has a B2B data feed deal with the industry’s two leaders, DraftKings (DKNG) and FanDuel (FLUT). Two years ago, management discontinued its full-bore sports betting business, believing it could not produce returns consistent with the costs as well as the intense competition from as many as 15 sites

So they stopped taking action on all sports, except their familiar territory of horse racing. Add to that its B2B data business, and today TS represents near 19% of total group revenues and 12% of Adj. EBITDA. It has proven a great decision, an expression of corporate strategy, best characterized as knowing when to hold ‘em and know when to fold ‘em. More on this later.

Gaming: The company owns 10 casinos in the U.S. and has positions in 22 more, who lease its Historical Racing Machines. (FYI: HRM are slot machines with video screens that replay unidentified horse races from a vast film and video library going deep into history that players can bet on with various wagers. It was once a fringe staple of most casino floors in Nevada that died. But CHDN has revived it with updated graphics and features, with great success.)

Its casino business is mostly cited in metro areas away from head-to-head daily revenue combat with major operations. This to a degree insulates it from the heavy marketing costs of going head-to-head with scaled up big name properties. It represents 39% of revenue and near 45% of Adj. EBITDA. Its revenue growth moved at a CAGR of 12.55% over more than a decade.

google

Above: Fair value a modest rise above trading compared to pees, but CHDN is closer to fully valued because its biggest holders are in for the long pull.

CHDN Revenue growth

Pre-covid 2019: $1.33b

2024E: $2.72b

Pro: 2024: $3b

Earnings E24: $6.09 – P/E 22.08 YOY 23+10%+

Trending growth pace to 2026: $8 – P/E 15.60

Payout ratio: $0.38 or 7.49%

Market cap: $9.89b

Enterprise value: $14.6b

Trading volume: (3 months) 477,537.

Shares outstanding: 73.5m, 72% of which are owned by institutions. Herein lies the tale: CHDN is by any measure a diverse, savvy capital allocator with proven skills both in acquisitions and disposals of businesses it had bought with high hopes for building revenue and diversifying its products.

A perfect example is CHDN’s purchase for $885m in 2014 of the Seattle based Big Fish social media business. Much happy talk rhetoric emanated from CHDN at the deal. The company saw its pivot into the red-hot sector as a major growth move with more to come. But it didn’t take long for the Seattle bro work culture to clash with the CHDN belt and suspenders pros across many strategic decisions.

There were other reasons, of course, but in the main it amounted to results not bearing out potential. In 2017, CHDN saw the writing on the fiscal wall that it did not find enlightening, so it sold Big Fish to Aristocrat of Australia for $990m, pocketing the $150m in the process. (Big Fish revenues today are ~$270m).

There are other forays CHDN has acquired or disposed of on the way. We cite them to reinforce our conviction that the company, with its off-the-center state of the gaming industry’s big moves, has shown prudence in assembling assets that have produced results. As such, it has earned a place in the hearts of holders that remains to this day. Clearly, CHDN’s share price history is, to a great extent, also a product of its relatively small outstanding of public shares.

There is little question that the company could get far more aggressive by seeking many sector moves to accelerate its growth by a more expansive program of lending for acquisitions. But it is clear that management has elected to keep the company in a safe zone where it doesn’t bump into competitive pressures on growth, leading it to uncomfortable pastures. It is not unfair, I believe, to characterize CHDN management as content populating its home-grown, somewhat low visibility status as a solid performer with a stable board and a shareholder group pleased with its progress.

CHDN’s EV/EBITDA ratio at 18 at 12/23 is nearly double what most analysts believe to be “healthy” at 10. But one of the factors here springs from a debt profile. The company is sitting on $4.93b in debt, mostly due to an aggressive capex policy to spend on acquisitions like its new Terre Haute property in Indiana and the expansion of it historic horse racing slot population. Its thin trading volume not only springs from its small outstanding, but its longtime holders are a happy tribe. Relatively speaking, its cash position at $149m is a bit sparse relative to its debt. Its financial leverage at writing is 5.96, high but manageable. But in its recent earnings call, management indicated that given the opportunity, it would not hesitate to raise leverage if the promise ahead was really enticing.

We find this a positive overall. Its track record in producing accretive EBITDA on expansion or acquisitions is sound. It record of earnings growth proves its astuteness in both making choices and abandoning poor returns on investment quickly. So, is this a case made for the stock at $135, a general range it has inhabited for years? Earnings growth will continue unabated from its strategy of being a big guy in a smaller pond with an eagle always open to smart chances.

Signposts for the road ahead for investors

From a pure analysis of the performance of CHDN shares over the last decade, we see a strong bull case from investors happy with yield, confident that growth will be both organic and from deal making. When so many of its biggest holders have been around so long, it is difficult to conclude that the downside risk is very low and yield will justify holding the position.

What does trigger a head scratcher on CHDN is whether going into the second decade since 2000, the company’s narrow, but effective vision, for its future suggests it is a sound rocking chair stock not for investors seeking big time returns on betting stocks with bigger eyes ahead?

We look at the shares of Flutter Entertainment (FLUT), parent of online sector leader FanDuel. At writing, the shares are $191.55 propelled by its dominant 47% share of the U.S. sports betting market, and its expected turn to be profitable. Consensus analyst PT today shows a 36% upside for FLUT based on revenue growth, earnings gains on a scale and a forecasted $11.7b this year in revenue from its US and global businesses.

The analyst average PT for CHDN stock is $148, a 10% upside valuation vs 36% for FLUT. Unquestionably, both stocks have powerful BUY rationales for different reasons. FLUT will participate in the double-digit growth of sports betting until the sector reaches $30b in annual revenue by 2030.

CHDN will have to produce a quantum leap combining issuing more equity, reaching for a split, or massive borrowing to scale its current $3bE annual revenue and EPS performance way above its current footprint. Its real-world growth save a merger or acquisition will be nice, but incremental. They’ve invested heavily, bringing great new feature space to the mother track. But you can only add so many bells and whistles until audiences begin to say, been there, done it.

So investors need to examine whether their overall strategy has room for a first class rocking chair stock or go all in on a skyrocket like FLUT that could well materialize once it gets sustaining profits. Holding both in a well-balanced gaming portfolio isn’t a half bad an idea, either. You have a low-risk yield above 7% or more, an effective, proven management, and long-range conviction that it will continue as a reliable producer of rising earnings year over year.

Read the full article here