Introduction

Citigroup (NYSE:C) is one of the largest banks in the world, and known as a “too big to fail” bank. I’ve covered Citigroup over the years, but most recently, I wrote about the bank’s 9.5% yielding preferred shares back in October. Since then, the preferred shares have been called and the bank’s common shares have rallied by more than 50%. Despite the rally, I believe that investors should consider taking a long position in Citigroup.

Citigroup Financial Results

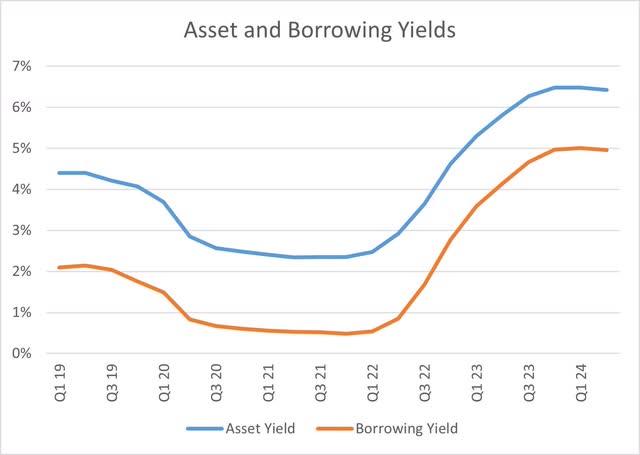

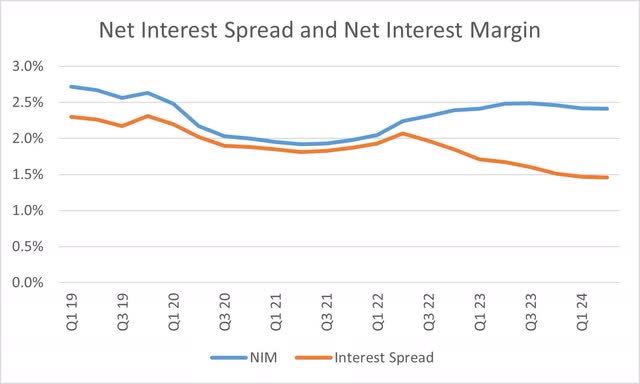

Like any other bank, Citigroup is not exempt from the changes in interest rates. During the pandemic, unprecedented easing drove the bank’s borrowing yields down to around 0.5% while asset yields were below 2.5%. As the Federal Reserve aggressively increased interest rates to fight inflation, the bank saw its asset yields climb to over 6%, but its borrowing yields also grew to over 5%. Despite the net interest spread (asset yield less borrowing yield) falling to under 1.5%, the bank has managed to reduce leverage and keep its net interest margin above pandemic era levels.

Company Financials Company Financials

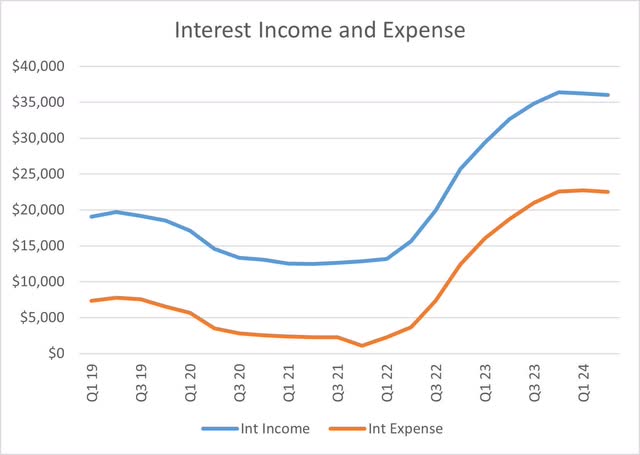

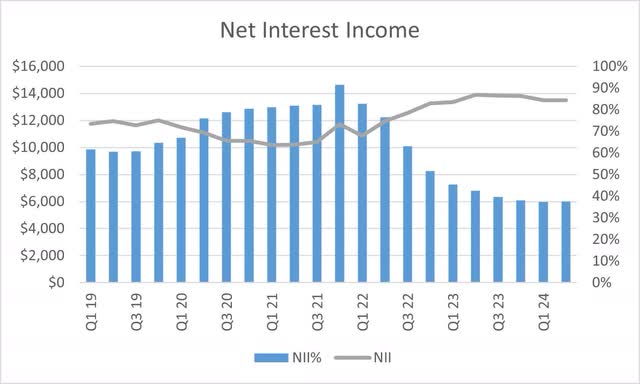

With respect to earnings, Citigroup saw its interest income and interest expense trend with asset and borrowing yields over the last five years, although each fell slightly in the second quarter. Despite the headwinds of higher interest rates, net interest income (interest income less interest expense) remains well above pandemic and pre-pandemic levels and only slightly off the highs achieved late last year.

Company Financials Company Financials

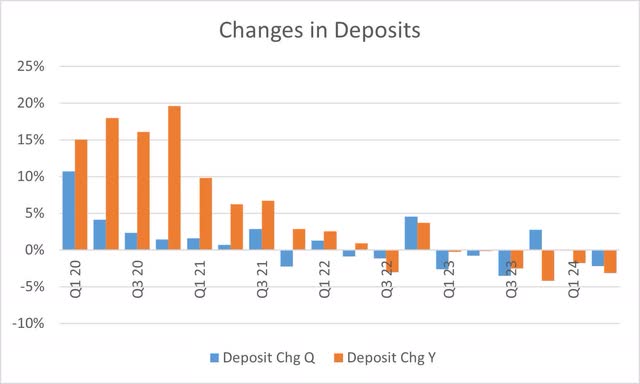

Loans and Deposits

When the regional banking crisis hit last March, media outlets reported that deposits were fleeing regional banks and ending up in “too big to fail” banks. The only problem with that theory is that it wasn’t true, especially for Citigroup. The bank has seen deposits decline on a year-over-year basis for six consecutive and seven out of the last eight quarters.

Company Financials

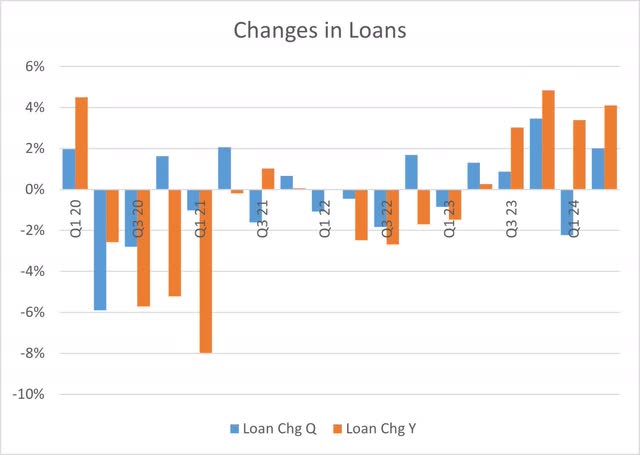

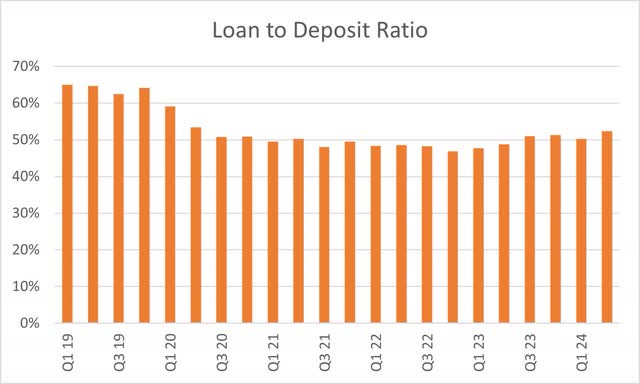

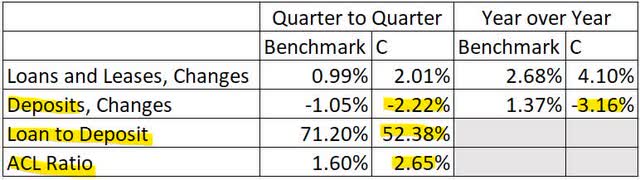

On the loan side, Citigroup saw a rebound in loan growth after declines in 2022 and early 2023. Loan growth currently stands above 4% on a year-over-year basis. One challenge with loan growth when deposits are shrinking is that it increases the bank’s loan to deposit ratio, which can increase the bank’s dependence on external financing and create earnings headwinds. Fortunately, Citigroup has one of the lowest, if not the lowest, loan to deposit ratios in the industry at 52%. Despite the increase in the loan to deposit ratio, Citigroup has managed to reduce its long-term debt by more than $6 billion in the first half of 2024.

Company Financials Company Financials Federal Reserve & Company Financials SEC 10-Q

The Risks and the Future

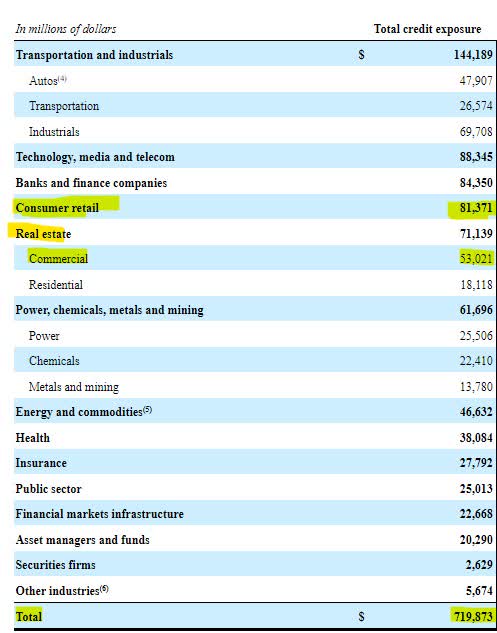

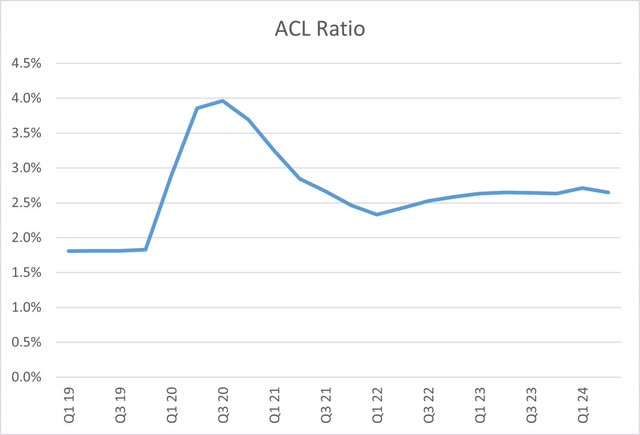

The loan composition and performance of banks are going to be under scrutiny as the commercial real estate sector undergoes changes relating to the pandemic. Fortunately, Citigroup’s $719 billion loan exposure only includes $53 billion to commercial real estate, or just under 8% of the entire portfolio. Investors should be more concerned with the bank’s $81 billion exposure to consumer retail, which has performed just as poorly as the office space for an extended period. Fortunately, Citigroup is buffered by an allowance for credit losses equaling 2.5% of gross loans, which is 90 basis points higher than the average commercial bank.

SEC 10-Q Company Financials

Analysts are confident in Citigroup’s ability to trim costs and grow earnings as they are currently estimating 2025 earnings at over $7 per share, or 21% higher than 2024 earnings estimates. For 2026, a smaller group of analysts is estimating earnings of over $8 per share, placing today’s share price at just under 7.5 times 2026 earnings.

Yahoo Finance

Valuation Relative to Peers

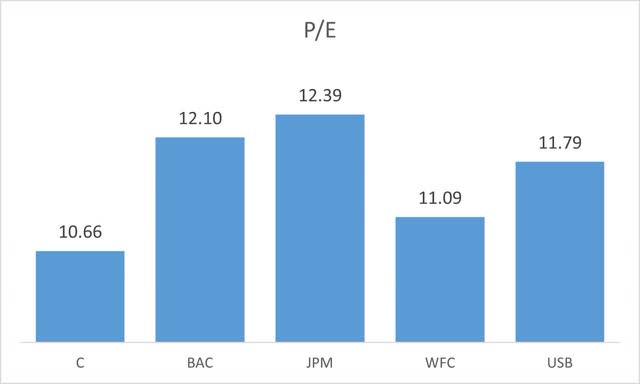

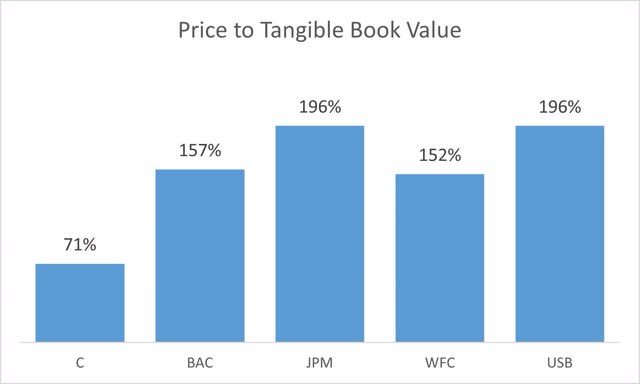

Despite the 50% run up in share price over the last year, Citigroup is still cheap when compared to its peers. Citigroup is among the top five banks in the US by asset size. When comparing Citigroup to the other four peers, the bank is currently trading at the lowest price to forward earnings, but that isn’t the most glaring comparison. When looking at price to tangible book value, Citigroup is well below its peer institutions. If the turnaround succeeds and Citigroup grows earnings, the bank’s shares will begin to move towards their peers and share price growth should outpace earnings growth.

Seeking Alpha Earnings Releases

Conclusion

Citigroup’s conservative balance sheet is going to be the cornerstone of its earnings growth over the next couple of years. The bank has sufficient loan diversity to ride out a storm and an ample allowance for loan losses to protect earnings. A low loan to deposit ratio will allow it to finance its loan growth as demand rises with lower interest rates. The cheap valuation compared to peers is icing on the cake. I’m expecting Citigroup to succeed in its turnaround initiatives over the next three years and for shareholders to be the primary beneficiaries.

Read the full article here