Introduction

Although the preferred shares issued by banks and financial institutions are traditionally non-cumulative in nature (which means that in case the bank skips a preferred dividend payment, it does not have to make up for it in the future), the perception of a missed preferred dividend payment is so negative that I think the major banks would want to avoid reputational damage at any cost.

I discussed Citigroup’s (NYSE:C) preferred shares in an article last year and I argued some of the bank’s issues offered interesting exposure to higher interest rates due to the floating nature after an initial holding period. There initially was some confusion about whether or not the bank would apply the SOFR benchmark rate to replace the LIBOR but every single major bank has now confirmed the SOFR will be used to determine the floating rates. And this increases the odds of some of the preferred shares being called as the high interest rates on the financial markets make some of that preferred equity pretty expensive.

A closer look at the Q3 results from the perspective of a preferred shareholder

Before having a closer look at the preferred shares, I think it makes sense to take a few minutes to discuss the performance of Citigroup as a company as this ultimately determines how attractive and reliable an investment in its preferred equity is.

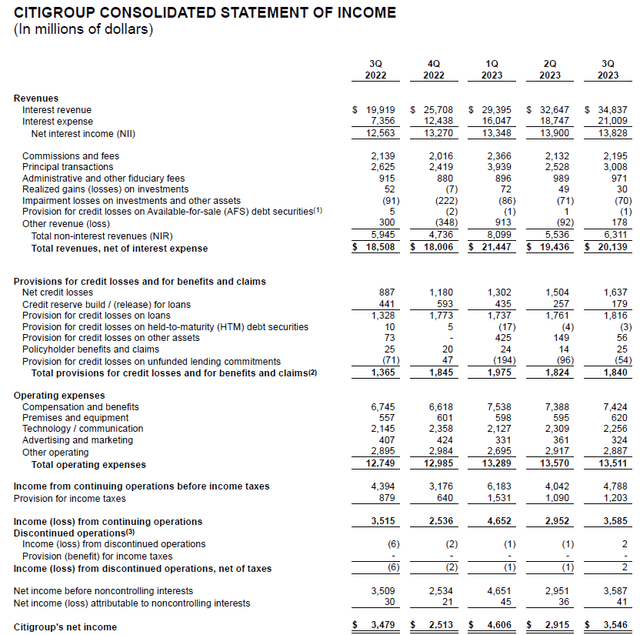

Fortunately the bank performed well during the third quarter. As you can see in the income statement (shown below), the bank was able to keep its net interest income pretty stable: it was about 3.5% higher than in the first quarter of the year and just about 0.5% lower than during the second quarter as the total amount of interest expenses increased by 12% while the interest income increased by ‘just’ 7%.

Citigroup Investor Relations

Additionally, the total non-interest revenue increased by approximately 14% mainly thanks to a serious increase of the revenue related to principal transactions. This boosted the total revenue to $20.1B which is a 4% QoQ increase although it is a lower total revenue than in the first quarter of this year as that quarter contained a few outsized (and non-recurring) tailwinds.

One of the main elements to keep an eye on these days is the cost structure. Several banks have already started to look into cutting costs to protect the profitability of the business. This isn’t an issue for Citigroup as its total operating expenses have remained remarkably stable. While the $13.5B in operating expenses is indeed higher than for instance a year ago, it does represent a small decrease compared to the second quarter of this year. Meanwhile, the pre-tax income jumped to $4.8B after also taking the $1.84B in credit loss provisions into account.

After making the relevant tax payments and crediting the non-controlling interests with the $41M in net income that is attributable to them, the bottom line showed a net profit of $3.55B in the third quarter. That’s a great result, but we still need to deduct the $333M in preferred dividends from that amount to ultimately end up with a net income of $3.17B attributable to the common shareholders of Citigroup, and that represents approximately $1.63 per share. The 9M 2023 EPS now stands at $5.15.

Citigroup Investor Relations

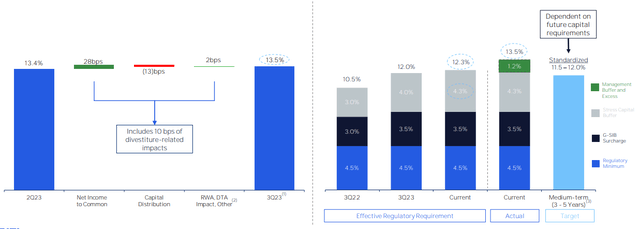

Also important is the continuously increasing CET1 ratio of the financial institution. Whereas the bank ended Q3 2022 with a CET1 ratio of 12.26%, it has boosted this to 13.5% just one year later and that is a pretty remarkable improvement thanks to a lower amount of Risk-Weighed Assets. With 13.5% as its new CET1 ratio, the bank now exceeds the regulatory capital requirement by 120 bp or $14B and that will for sure help to mitigate the impact of a tougher business environment. On its conference call, management clearly indicated it expects more tailwinds to the CET1 ratio thanks to further reductions in the RWA.

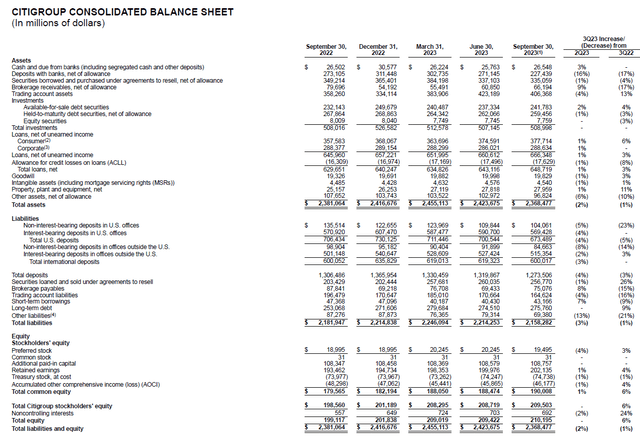

Meanwhile the tangible book value increased to $86.90 per share, an increase of $6.56 per share compared to the third quarter of 2022.

Additional clarity on the use of SOFR increases call option ‘risk’

Looking at the financial results of Citigroup, the preferred dividends of $333M during the third quarter are still very well covered by the earnings. Citigroup needed just 9% of its attributable net income to cover the preferred dividends and this ratio will likely improve a little bit as Citi has started to call some of its preferred shares.

From an asset coverage ratio perspective, the balance sheet of Citigroup contained about $190B in equity, of which $19.5B is preferred equity. This means there is a cushion of about $171M of common equity which ranks junior to the preferred shares. That’s a comfortable position to be in, especially knowing the bank is currently retaining about $1.5B per quarter in equity.

Citigroup Investor Relations

A year ago, there was a lot of uncertainty about how certain issuers would deal with abandoning the LIBOR as a reference rate for floating rate dividends. Most issuers agreed to use the SOFR as replacement and only a handful of companies decided to fall back on the strict interpretation of their IPO documents which fixes the preferred dividend rate based on the preceding payments rather than replacing the LIBOR with the SOFR.

But as mentioned, Citigroup did the right thing and followed the guidelines in the sector (again, the reputational damage would be worse than the few million dollar Citigroup would be able to save) and this already resulted in the bank calling the Series K of the preferred shares. That series is trading with (NYSE:C.PR.K) as ticker symbol and I already highlighted this series in an article in 2022 explaining how a high interest rate on the financial markets increases the call ‘risk’. The bank has now notified the Series K shareholders the securities will be called in November of this year.

That makes sense as the quarterly reset of the preferred dividend would have cost the bank close to 10% given the formula for the floating rate dividend was the 3-month SOFR + 0.26161% + 4.13%. With the 3M SOFR currently at 5.3-5.4% Citigroup clearly didn’t feel like paying $147M per year on this $1.5B issue.

This also means some of the other preferred shares may be called. The Series J for instance, which is trading with (C.PR.J) as ticker symbol is also callable right now and is currently paying a preferred dividend based on the same 3M SOFR increased by the standard 0.26161% and 4.04%. This means that the yield on the Series J is currently close to 9.7%. That’s not a day dream as Citi has effectively declared a quarterly dividend of $0.606/share, payable in December.

Seeking Alpha

This is a smaller sized issue with a slightly lower mark-up (404 bp versus 413 bp), but this security could be the next in line to be called by Citigroup and that explains why the preferred share is trading with a premium to its principal value of $25/share.

Investment thesis

Citigroup’s financial performance is much stronger than what the share price would make you think. The bank will likely see its full-year EPS come in north of $6 which means it is trading at an earnings multiple of less than 7x. Meanwhile, the high capital retention further boosts the capital ratios and the bank adds about 10-15 bps per quarter (likely the lower end of that range if you’d exclude the impact of divestitures) to its CET1 ratio.

Given the relatively strong earnings profile and the continuous focus on the balance sheet and capital ratios in combination with the stock trading at a discount of approximately 55% to its tangible value, I am getting interested in the common shares of Citigroup as well as some of its preferred shares. I currently have no position in either equity class, but I am keeping an eye on Citigroup’s performance.

Read the full article here