Shares of Citizens Financial Group (NYSE:CFG) have been a strong performer over the past year, as the bank has recovered from the Q1 2023 regional banking crisis. Shares now sit near a 52-week high, up 36%. I last covered CFG in January, rating it a “buy,” and while shares have returned 14%, approaching my $37.50 target, that return has lagged the market’s 16% gain. With the company set to report earnings July 17th, now is a good time to preview results and determine how to best position in shares. I am cautious into earnings.

Seeking Alpha

Q1 Results Were Solid, But Reserves Are Low

Before considering what to look for in Citizens’ Q2 earnings, we should revisit the company’s Q1 results. In the company’s first quarter, it earned an adjusted $0.79. Net interest income (NII) declined by $46 million sequentially to $1.44 billion. This decline was primarily driven by lower interest earning assets as the bank’s net interest margin (NIM) was 291bps, stable sequentially though down 39bp from last year given increased funding costs.

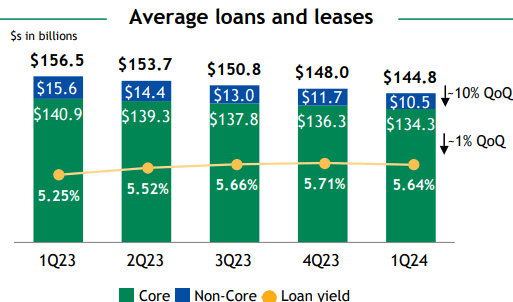

Citizens has been transforming itself, shedding non-core assets and growing a new private bank. The wind-down unit continues to shrink assets, which has reduced loan balances and NII. As you can see below, non-core loans fell by 10% while core loans were down a more modest 1%. Total loans were down 2% sequentially. Core loans declined due to weak customer demand as high rates have reduced the appetite to borrow. I hope to see loans bottom during Q2 as the impact of its run-off unit begins to diminish.

Citizens

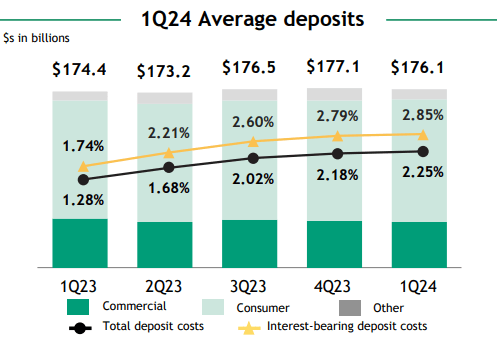

Aside from lower loan balances, funding costs continue to be in focus. As I have written about previously, I view stable deposits as essential when investing in regional banks as deposits are the lifeblood of a bank’s finances. CFG’s deposits are up about 1% from last year. They did fall by $1 billion sequentially, due to weakness in commercial accounts with consumer deposits rising by $1.5 billion.

Citizens

Now, Q1 typically sees commercial balances come under pressure as cash tends to build during December and is then spent. I view this modest sequential decline as consistent with broadly stable deposits. We are also seeing cost pressures diminish. The 6bp rise in interest-bearing deposits was the smallest in over 18 months. We also may be at the peak. In March, $3 billion of 5+% CDs matured, and it rolled 75% between 3 and 4%, which should benefit Q2 deposit costs. After declining last year, we also saw non-interesting bearing balances stabilize. With average account sizes back to pre-COVID levels, most of this outflow is likely behind CFG.

Citizens

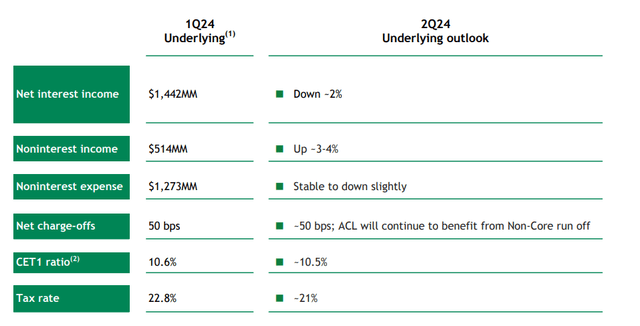

Aside from these factors, other highlights of Q1 included non-interest income rising by 3% to $514 million, thanks to improved capital markets. Non-interest expenses rose by less than 1%, excluding its $35 million FDIC assessment, speaking to strong cost discipline even as it invests in its private bank.

Looking at results across units, the “Core” bank earned $425 million, including a $15 million loss on its private bank. Within the private bank, it spent $38 million on non-interest expenses as it invests to scale up operations. It will take some time for this unit to generate profits, but private banking can generate very strong returns once scaled. Its run-off operation lost $0.13. There was $1.2 billion of run-off to $9.9 billion of interest earning assets at quarter-end.

Finally, on credit quality, CFG had net charge-offs of 50bps, and it took $171 million in provisions for credit losses, similar to prior quarters. Its allowances of $2.3 billion now cover 1.61% of loans, including 10.6% of general office loans. CFG has $1.47 billion of nonaccruals, up $105 million sequentially, due to weakness in General Office. That means there is just 157% ACL coverage of nonperforming assets, down from 229% last year.

This is a relatively light level of coverage, and I generally like to see at least 200-250% coverage, and so it remains an area to watch. CFG does have $3.4 billion of office exposure. Its reserves here assume a 71% peak-to-trough price decline and a 24% default rate, which do feel conservative. While overall reserves are a source of caution, I am comforted to see strong reserving within the most vulnerable segment of its loan book.

CFG also is well capitalized with a 10.6% common equity tier one (CET1) ratio, above its 10-10.5% target. Now, its unrealized losses on its securities portfolio would be a $2.8 billion headwind to CET1m if included. CFG’s CET1 would be 8.9% including AOCI; however, it has several years to phase this impact in. Because its fixed income portfolio is relatively short-dated, its AOCI loss will also naturally fall over time, dropping to $2.4 billion by year-end and $1.7 billion by the end of 2026, further reducing the capital impact.

Overall, CFG reported solid Q1 results that showed stable funding but slow asset growth. Capital is strong, but reserves are potentially a little light.

A Big Q2 Beat Appears Unlikely

Now as we look to next week’s earnings release, there are several items, I will be focusing in on. First, I would note that in Q2, analysts are expecting CFG to earn $0.79. CFG has beaten estimates in 3 of the past 6 quarters. Prior to that, it had beaten for eight straight quarters, so results have been a bit choppier since the regional banking turmoil began in late 2022/early 2023.

Based on CFG’s guidance, revenue is likely to be down about $10-$15 million sequentially, though a lower tax rate should be about a $5-7 million tailwind. In order to meet analyst consensus, based on these guidance items, we would need to see expenses and/or credit reserves fall by about $8 million. This strikes me as aggressive, and in order to meet estimates, we are likely to need to see some top-line surprise.

Citizens

Now, I am cautiously optimistic we see slightly improved net interest income vs guidance. In Q2, I will be looking to see deposits at least flat, to validate that the Q1 drop was a seasonal factor. Given favorable CD renewals, I would expect deposit costs to increase by less than Q1’s 6bp and ideally be close to flat. With a September rate cut appearing likely, I will also expect commentary that Q2 represents a peak in deposit costs.

The loan side will be more difficult to judge. Citizens is down to an 81% loan-to-deposit ratio, giving it capacity to accelerate lending. However, we also want to see run-off declines continue. With many expecting the Fed to begin cutting later this year, clients may be waiting to borrow until conditions are more favorable. Currently, I expect loan growth to be down 1-2%, but I expect to see core loans decline by less than $2 billion in Q1. Over the medium term, CFG is targeting a 325-340bp NIM, which will require core loan growth.

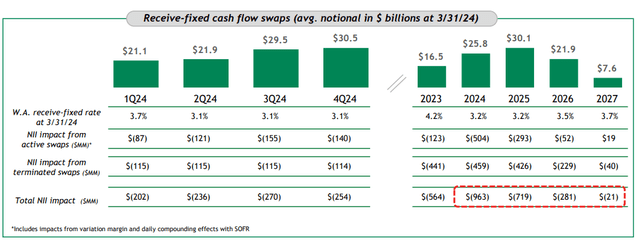

One favorable item for NIM is that we should be near the peak “pain” quarter for its fixed rate swap positions. As you can see below, it has swapped out some floating rate exposure back to fixed at much lower yields. Q3 is likely to be the worst quarter, and the pressure will ease into 2025 as its swap rates gradually rise and as the Fed also cuts rate. Its swap position will cost CFG nearly $1 billion this year, dropping to $700 million next year and then below $300 million. These swaps are reducing EPS by about $1.70 this year. Ultimately, CFG management was too quick to lock in rates and did not expect the Fed to hike as much as it did. I would hope to see limited growth in its swap positions in Q2, given how painful they have been.

Citizens

Now, the private bank is quite small at about 1% of assets, and I expect it to continue to lose money this year as CFG builds staff, marketing, and infrastructure. Here though, management commentary will be interesting. CFG is trying to expand in the NYC metro area in particular. Given the challenges at New York Community Bancorp (NYCB), there may be an opportunity to take clients or financial advisors here.

The other big question is what CFG does on credit provisions. Just given the pressure on commercial real estate, I would expect another quarter of ~$170 million in provisions. All else equal, I would like to see CFG continue to build reserves, as its ACL coverage does appear a bit light. I would be more concerned about a larger reserve build if not for the bank’s stress test performance.

Citizens fared well on the Federal Reserve’s most recent stress test. Interestingly, the Fed’s test resulted in CFG facing less commercial real estate losses than a year ago, as it has been allowing office loans to shrink and has already taken a 6% default rate over the past year. The fact CFG saw better credit performance than last year, does make me feel a bit more comfortable that it has not built more reserves more aggressively. Still, I expect this to be an ongoing focus point.

Indeed, CFG performed so well on the stress that it announced a $1.25 billion share repurchase program. Based on its performance in the stress test, CFG needs to maintain a 9% CET1 capital ratio whereas it expects to end Q2 around 10.6%, just above its 10-10.5% target. CFG also pays a 4.6% dividend. I would expect CFG to repurchase about $150-$225 million in stock per quarter over the next year.

Conclusion

Overall, I expect CFG to earn $0.77-$0.81 in Q2, as I see some upside risk relative to guidance on NII but also the potential for reserves to be higher. With analysts having raised estimates a bit in recent weeks, CFG appears poised to deliver an in-line quarter, and I would be surprised to see a significant beat. That said, as we begin moving past the worst of the swap headwind and the drag from non-core run-off, CFG should be well positioned to begin growing earnings more aggressively in H2 and particularly in 2025 when the bank should have $3.75-$4.00 in earnings power.

9.4x 2025 earnings is not particularly cheap in the regional banking sector, and there are still some questions in my mind about the adequacy of reserves, which may keep quarterly provisions higher for longer. Additionally, while the swap headwind will begin fading, it will take until 2026 for it to really dissipate more materially. I continue to view ~$37.50 as fair value, or 1.25x tangible book value and 10x the low-end of my 2025 estimates, given these concerns.

That gives shares only about 2.5% upside or about a 7% total return potential, including its dividend. As such, I am downgrading shares to a “hold” ahead of earnings, as I do not view a big beat as likely and do expect questions about reserves to dominate. Now, if we see faster loan and deposit growth, this could prove overly cautious, but I view a hold rating as now appropriate. With shares still below 10x and its favorable stress test, I do not see shares as a sell, though I am tactically cautious into earnings. I would wait until after Q2 results to consider adding CFG. There is not an urgency for long-term investors to sell ahead of earnings given valuation, but more tactical investors may consider lightening positions.

Read the full article here