By Derek Deutsch, CFA, & Mary Jane McQuillen

The Circular Economy Is a Growth Business

Market Overview

U.S. equities rose in a challenging quarter for diversified portfolios as market leadership remained concentrated in a few mega cap companies perceived to be the biggest winners in the growing AI market. The benchmark Russell 3000 Index returned 3.22%, largely thanks to growth stocks as the Russell 3000 Growth Index (7.80%) outpaced its value counterpart by over 1,000 basis points. Small caps, which are more sensitive to elevated Treasury yields, were also weaker compared to large caps.

Information technology (‘IT’) and communication services dominated the Russell 3000 on mega cap AI-related enthusiasm, while utilities and consumer staples performed well, in part rebounding from oversold levels but also, in the case of utilities, as some began to get some credit for their role powering AI data centers. Softly deteriorating economic data, meanwhile, weighed on cyclical sectors like materials, industrials and financials.

The Strategy trailed the Russell 3000 Index benchmark largely due to our diversified positioning, although we maintain a considerable portfolio allocation to large cap AI-related companies. These positions were indeed among our top contributors in the quarter, such as Microsoft (MSFT). The company is finding more ways to deploy AI for sustainability objectives such as its ability to better measure, predict and optimize complex systems, which can help its partner communities reduce wildfire risk. Also driving the phenomenal growth of AI were contributors Broadcom (AVGO), a leading semiconductor company and increasingly a hybrid software company after a series of strategic acquisitions, and Dell Technologies (DELL), which is enjoying high demand for its AI-optimized servers.

“Faster delivery times through reduced freight, miles and packaging can reduce waste.”

Consumer staples holdings were also standouts in the quarter, such as Costco (COST), which continues to execute well and delivered better than expected earnings, helped by strong traffic driving better expense leverage. Customers also looked to be shifting toward more discretionary purchases. Colgate-Palmolive (CL), added to the portfolio in 2023, started outperforming materially toward the tail end of last year as growth, margin and market share momentum began to turn favorably, and that momentum has continued year to date as the stock has nicely outperformed the large cap staples group. The fundamental upside has been driven by a combination of healthy organic growth (with positive volumes), good gross margin progression, and strong re-investment spending supporting market share gains and future growth.

Weakness among cyclical sectors and some stock-specific fundamentals were behind the portfolio’s main detractors in the quarter. Industrials holdings Regal Rexnord (RRX) and TREX were down amid slowing macro sentiment: Regal Rexnord reported lower than expected revenue growth in its most recent results, citing recent market headwinds for its power efficiency solutions segment and its factory automation business; building suppliers like Trex, which makes composite residential decking, traded down as remodeling activity slowed amid persistent higher interest rates.

In IT, Salesforce shares were lower as its latest earnings report revealed slowing momentum and the company provided second-quarter guidance below consensus. Software spending by enterprises has slowed as companies have re-prioritized IT spending toward AI-related infrastructure, a phenomenon we believe is likely to prove cyclical and not structural.

CVS Health, meanwhile, is coping with a prolonged uptick in the utilization of medical services by its Medicare Advantage clients, which has coincided with government pressure on payer reimbursements. The short cycle nature of managed care insurance along with the company’s focus on margins, however, gives us confidence that it will be able to grow earnings over the next few years.

Portfolio Positioning

We added two new names to the portfolio in the quarter.

Amazon.com (AMZN) operates the world’s leading e-commerce marketplace and the largest public cloud platform and has a burgeoning advertising business. We expect to see sustained margin improvement as Amazon’s retail regionalization efforts are bearing fruit and as its advertising business continues to scale ahead of peers. We believe the profitability ramp is still in the early innings as the company turns its attention to improving costs. One area will be inbound shipping, where faster delivery times through reduced freight, miles and packaging can reduce waste. We also see generative AI tailwinds and infrastructure modernization driving re-acceleration in growth at AWS, further enhancing Amazon’s free cash flow compounding potential. In addition, following our early 2024 ESG engagements with Amazon (after multiyear engagements) we were positively inclined to see continued improvements in labor relations (health and safety metrics, benefits and wages), as well as in environmental stewardship (climate targets, reducing packaging materials, electric delivery trucks) and innovation (commitments to responsible AI and data privacy). One of the newly announced initiatives on the retail side is consolidating deliveries into fewer boxes, which reduces packaging.

“AI can aid sustainability through better measuring, predicting and optimizing complex systems to help reduce wildfire risk.”

Republic Services (RSG) is a waste disposal company in the industrials sector whose services include non-hazardous solid waste collection, waste transfer, waste disposal, recycling and energy services. It is a stable-through-the-cycle compounder in a consolidated industry. The company’s end market is resilient, which gives us some confidence in the stability of its earnings through a recession. In the next few years, cash flow should grow at the high end of the range as Republic Services benefits from high-returning sustainability investments in polymer recycling and renewable natural gas, which also improve the company’s emission and circularity profile. Republic Services continues to set ambitious goals around sustainability targets, such as increasing its renewable energy generation by 50% through the beneficial reuse of biogas. In addition, its 74 recycling centers process five million tons of materials per year and include a major polymers center for plastics. Notably, it is the first North American waste and recycling company with an emissions reduction goal approved by the Science-Based Targets initiative (SBTi).

Outlook

Looking ahead, we see a mix of positives and negatives for equities, with slowing economic growth and political uncertainty balancing strength in corporate margins and potential monetary easing in the coming quarters. We continue to be active in positioning the portfolio amid a period of unusual market concentration, in which we believe quality businesses with reasonable valuations are being overlooked. We are quite constructive about the companies we own, meanwhile, and their ability to execute in a variety of economic scenarios.

Portfolio Highlights

The ClearBridge Sustainability Leaders Strategy underperformed its Russell 3000 Index benchmark during the second quarter. On an absolute basis, the Strategy had gains in four of 10 sectors in which it was invested (out of 11 sectors total). The main contributors were the IT and consumer staples sectors, while the industrials, health care and consumer discretionary sectors were the main detractors.

On a relative basis, overall stock selection detracted the most, in particular stock selection in the IT, consumer discretionary, health care, industrials and real estate sectors. Stock selection in the consumer staples sector and a lack of energy holdings, by contrast, proved beneficial.

On an individual stock basis, Apple (AAPL), Alphabet (GOOG,GOOGL), Microsoft, Costco and Broadcom were the largest contributors to absolute performance in the quarter. The main detractors from absolute returns were positions in CVS Health, Regal Rexnord, Trex, Walt Disney (DIS) and Salesforce (CRM).

Besides portfolio activity mentioned above, during the quarter we exited SolarEdge Technologies (SEDG) in the IT sector and Shoals Technologies (SHLS) in the industrials sector.

ESG Highlights: Dispatches from the Circular Economy

The Ellen MacArthur Foundation lists three basic principles of the circular economy: eliminating waste and pollution, circulating products and materials, and regenerating nature. These principles align with some key parts of ClearBridge’s fundamental ESG framework, notably factors such as resource efficiency, recycling, product life cycle management, renewable generation and land usage, which we engage on as part of ongoing company research. By reducing energy use, stress on the environment and pollution, the circular economy is also linked to mitigating climate change and conserving biodiversity.

Many ClearBridge holdings thus contribute to the circular economy as they either execute on best practices or make improvements in these areas. We have often highlighted Trex as exemplary of the circular economy. Trex is the market share leader of wood-alternative composite decking. Trex’s low-maintenance and high-quality decking products are composed of 95% recycled wood fibers and plastic, making use of waste that would otherwise end up in landfills. Trex has continued to innovate and advance plastic recycling processes. Recently, as the demand for “clean streams” of plastic waste has increased in different parts of the economy, Trex has upgraded technology to be able to accept “dirtier” streams of plastic waste into the manufacturing process. This allowed Trex to begin using additional quantities of waste plastic that would otherwise never be recycled, without compromising product quality standards. Trex products are more durable and have a longer life than traditional wood decking, therefore reducing overall raw material usage and end-product manufacturing. Finally, the quality and durability of the product saves consumers money through less frequent replacements and lower maintenance and upkeep costs.

Molecular Recycling Takes a Step Forward

While companies like Trex are making clear gains on plastic recycling, a circular economy that solves for plastics use remains a challenge. Regulatory bodies are stepping up requirements, such as the EU’s new rules to reduce, reuse and recycle packaging, provisionally agreed upon in March 2024. Under the new rules, plastic packaging must also include minimum recycled content.

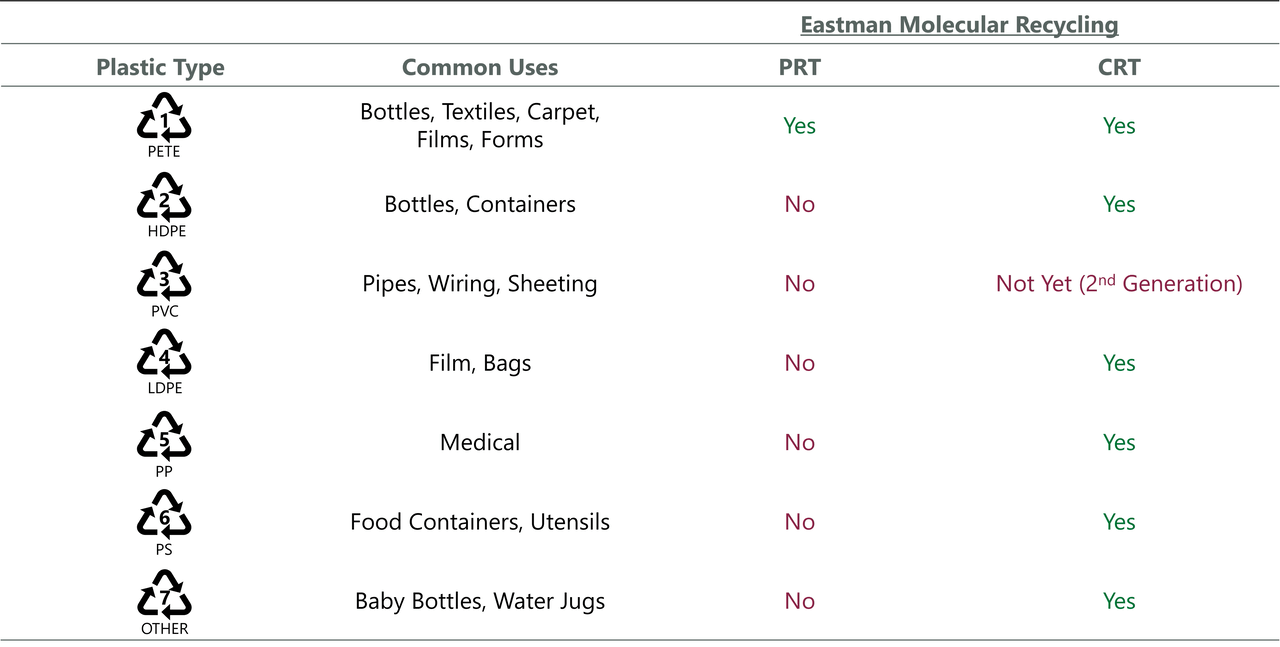

Helping companies meet these new rules will be ClearBridge holding Eastman Chemical (EMN), which makes a range of advanced materials, chemicals and fibers for everyday purposes, among them plastics for food packaging. In a recent engagement with Eastman Chemical we discussed two different chemical recycling technologies it has developed: polyester renewal technology (‘PRT’) and carbon renewal technology (‘CRT’). PRT recycles polyester-based materials such as soda bottles, carpet fibers and even clothing, breaking down their basic molecules until they are indistinguishable from materials made from virgin or nonrecycled content. CRT operates in a similar way but can take a broader range of plastic types and replaces the use of coal as a feedstock to make fibers. Combining these two technologies gives Eastman a competitive advantage in molecular recycling, as it can take most types of waste plastics (Exhibit 1). Ironically, securing feedstock (i.e., waste plastic) has been a bottleneck to scaling molecular recycling as competitor technologies not using Eastman’s dual technologies often require the waste plastic to be separated purely according to grade, which waste and recycling companies do not readily offer. Eastman’s dual technology approach allows it to accept most plastic grades, making it less reliant on waste companies’ sorting.

Eastman’s first recycling plant is now operational in Tennessee, which will supply its internal Advanced Materials lines while also proving out the technology. The company is already working toward a second plant in Texas that will have Pepsi (PEP) as its anchor customer. In the second plant, not only will Eastman help Pepsi meet its recycled content goals, but it is also expected to receive long-term, take-or-pay volume commitments, for doing so. This should greatly improve earnings visibility, and in turn, potentially valuation.

Exhibit 1: Eastman Chemical’s Molecular Recycling Methods

Source: Eastman Chemical.

Sustainable Food Needs Sustainable Plastic

As the case of Eastman Chemical suggests, plastic is central to sustainable food. Accordingly, companies in the food industry can advance the circular economy through practices such as recycling, reducing or improving the sustainability of packaging and reducing landfill waste.

Canadian grocer Loblaw (OTCPK:LBLCF) can make an impact with all three of these practices. In a recent engagement with Loblaw, we discussed its goal of making 100% of its control brand and in-store plastic packaging recyclable or reusable by 2025. This would put it in compliance with the Golden Design Rules (GDR), a set of rules established by the Consumer Goods Forum, made up of leading international retail and consumer goods companies, to benchmark packaging design, emphasizing the reduction of materials and the removal of problematic elements.

Noteworthy steps along the way have involved changes to Loblaw’s protein packaging, which used to come in polystyrene foam trays; the vast majority now are packaged in clear recycled PET trays, which are accepted in all the municipalities in which the store operates and allow for greater detectability in the recycling stream. The shift to PET trays for mushrooms led to 39.9 million trays entering the recycling stream in 2023. Removing the plastic window from 10 kg potato bags allowed 23 million bags to be more easily recycled in 2023. In addition, extending expiry dates for its PC Money Account and PC Mastercard physical cards should prevent more than 10,000 kgs of plastic waste in the next 12 years.

Loblaw’s advances in these areas also speak to its power to use its size to change the industry, as it communicated its GDR standards to hundreds of control brands and national brand vendors, effectively dictating a new national industry standard for plastic packaging. While navigating recycling standards and practices that vary from municipality to municipality, to improve recycling rates overall Loblaw supports extending producer responsibility, a system that give brand owners responsibility of both the cost and performance of recycling systems, incentivizing them to increase the recyclability of their packaging while empowering them with control over the recycling systems themselves.

Food waste is an avoidable crisis that has both environmental and societal costs, and linking food as an organic resource in a circular economy can reduce land use and better support growing populations. Loblaw has set a goal to send zero food to landfill by 2030, a goal supportive of Sustainable Development Goal 12: Responsible Consumption and Production, in particular target 12.3, to halve global food waste by 2030. The company is currently ramping up data collection on food waste but achieved over 78,000 metric tons of diverted food waste in 2023, with most going to composting, animal feed and redistribution of food surplus to food charities.

Supplying the Auto Aftermarket

LKQ is also focused on recycling heavy materials. LKQ is the largest wholesale distributor of alternative parts for the auto aftermarket in North America and Europe. It provides “like kind and quality” (‘LKQ’) auto parts as lower-cost alternatives to those provided by auto OEMs. It is the largest wholesale distributor of collision parts (used to repair vehicle exteriors) in the U.S. and Canada and the largest distributor of mechanical parts (used to repair internal components) in Europe. LKQ also runs its own salvage and recycling operations. As the world’s largest recycler of cars at end-of-life, recovering 90%+ of the materials from scrap cars for reuse or recycling, LKQ supports resource efficiency and responsible consumption as an investable theme.

In a recent engagement with LKQ we had an extensive discussion about how it has become increasingly efficient over time at inventorying and selling more parts from its salvage vehicles, which reduces the amount of parts going for scrap and increases LKQ’s margins, as it earns higher revenues from same fixed cost of goods.

Circular Economies Span All Sectors

One powerful aspect of the circular economy is how, although with differing dynamics and levels of challenges, every sector may contribute. ClearBridge will continue to share key company advances and engagements on the topic as our holdings innovate to operate more efficiently and enable a more resilient economic system, with fewer emissions and less waste.

Derek Deutsch, CFA, Managing Director, Portfolio Manager

Mary Jane McQuillen. Head of ESG, Portfolio Manager

|

Footnotes 1 “AI Will Transform the Global Economy. Let’s Make Sure It Benefits Humanity,” Kristalina Georgieva, IMF Blog. Img.org. Jan. 14, 2024. 2 Barclays Live – 2030 Thematic Roadmap: 150 Trends (Edition 5) – Managing AI’s blind spots (Investment Bank | Barclays). 3 “Retraining and Reskilling Workers in the Age of Automation,” Pablo Illanes, Susan Lund, Mona Mourshed, Scott Rutherford, and Magnus Tyreman, McKinsey. Mckinsey.com. Jan. 22, 2018. Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here