Cleveland-Cliffs Inc. (NYSE:CLF) announced their intent to acquire Stelco Holdings Inc. (OTCPK:STZHF) on July 15, 2024, for $2.5b split between cash and equity. The deal is anticipated to provide significant synergies between the two North American producers, as Stelco is among the lowest cost-per-ton producers of steel. Despite the optimism for the acquisition, Cleveland-Cliffs, along with the rest of the steel industry, is finding itself in a cyclical downturn in the face of a challenging macro environment.

Given the near-term headwinds, I will be downgrading CLF to a HOLD rating with a near-term price target of $18.46/share and will be lowering my long-term price target of $21.75/share.

You can read my previous coverage of Cleveland-Cliffs here:

Cleveland-Cliffs is expected to report eq2 ’24 earnings on 7/22/24, which will likely provide additional insight into the Stelco acquisition. I anticipate some improvement to steel production volumes paired with more challenging pricing, which I forecast to provide a -6% revenue growth rate and a 7% aEBITDA margin.

Cleveland-Cliffs To Acquire Stelco

Cleveland-Cliffs announced their intent to acquire Canadian steelmaker Stelco on July 15, 2024, for $2.5b USD for an EV/EBITDA multiple of 4.8x, a significant premium above the 2.5x valuation at which the market was pricing the company. This deal is expected to be highly accretive, with annual cost savings in the range of $120mm with next to no adjustments to business operations. In addition to cost synergies, the acquisition will provide Cleveland-Cliffs more access to the steel spot market and broaden the firm’s industry exposure outside the automotive industry. The deal remains in the early stages with an expected close date in eq4 ’24, but already has approval from USW and both Boards of Directors.

At this point, the biggest hurdles will be regulatory and antitrust approval, which management believes should follow through as both businesses operate in different segments of the steel industry. In addition to this, the deal is subject to approval by Stelco shareholders, which, I believe, will not be heavily challenged given the substantial premium to the firm’s pre-announcement valuation.

Financing of the deal will be split between cash and equity for a total consideration of CAD$60 and 0.454 shares, or CAD$10 in share equivalent for a total per-share value of CAD$70. Cleveland-Cliffs will finance the deal through a combination of unsecured notes and their existing ABL Facility to prioritize paying down debt immediately after close. This allows for the firm to manage down the expected 2.4x net leverage ratio EV/aEBITDA from the get-go. Stelco is net cash positive at $595mm with only $50mm in debt outstanding in their ABL Facility.

Corporate Reports

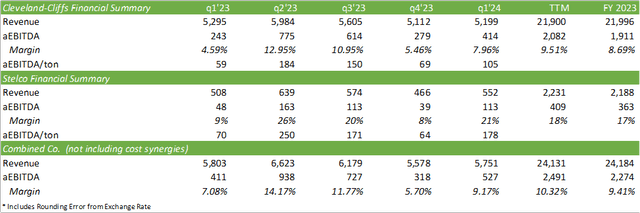

Stelco is said to be one of the lowest-cost steel producers in North America with a cost per ton of $480/ton USD for hot-rolled coil, or HRC, ~26% lower than the North American average of $650/ton. On a trailing twelve-month basis, Stelco generated $572mm in aEBITDA with a 19% margin. This is well above Cleveland-Cliff’s 10% margin for q1’24 on a TTM basis. Stelco makes up roughly 9% of the combined company’s revenue and 16% of aEBITDA.

One of the foundational strengths of our business is our ability to control our costs and drive revenue through to the bottom line.

-Alan Kestenbaum, Executive Chairman & CEO of Stelco.

Mr. Lourenco Goncalves, Chairman of the board, President, & CEO of Cleveland-Cliffs, anticipates significant operational synergies between the two firms as each has components to trade. Cleveland-Cliffs will be supplying HBI to the Lake Erie Works facility to improve throughput while maintaining operational capacity. This will likely reduce the amount of coking coal needed to produce their steel at this facility, as HBI is already reduced. In turn, Stelco has 2 coke plants that can feed excess capacity to Cleveland-Cliff’s blast furnaces in the US.

This intercompany trade may help push the deal through, as it provides support for minimal overlap between the two steel producers. Mr. Goncalves on the call announced that:

Stelco is a plug-and-play asset for Cleveland Cliffs

-Mr. Goncalves.

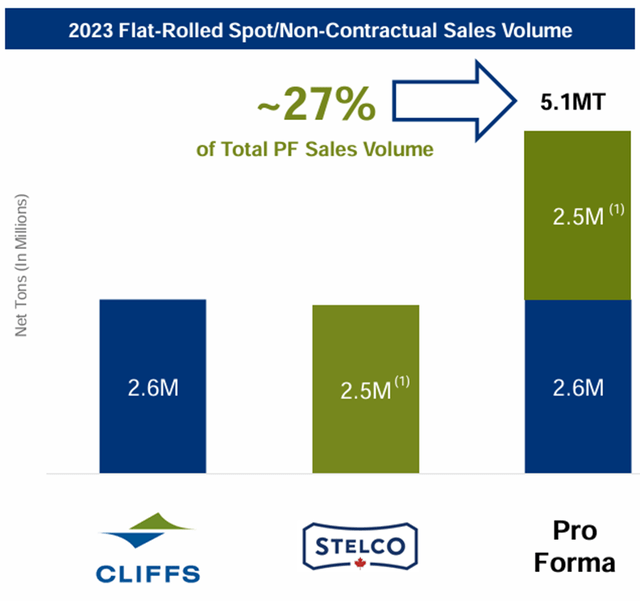

Though Stelco also caters to the automotive industry by supplying high-performance steel, the firm has a strong presence in the energy and construction industries in supplying HRC for tubular steel and line pipe. The breakdown of Stelco’s end-market mix is 2% automotive, 54% distributors & converters, 31% infrastructure & manufacturing, and 13% across other industries. Stelco will also provide Cleveland-Cliffs with more commoditized steel and provide more access to the steel spot market. This allows the combined firm to take advantage of price volatility and potentially provide greater flexibility to manage production volumes in the instance of a less-than-appealing pricing environment.

It should be noted that Mr. Goncalves emphasized on the call that capacity will not be assuaged as a result of the business combination. Using 2023 figures, the combined company would have a total of 19mm net tons of steel shipped.

Corporate Reports

USS Is Still On The Table

Despite the announced acquisition of Stelco, Mr. Goncalves spent a few minutes throwing in his two cents worth on the United States Steel Corporation (X) and Nippon Steel Corporation (OTCPK:NPSCY) deal. He briefly discussed his thoughts on the challenges faced in receiving approval, as the deal is considered a national security threat. To reiterate information from my previous coverage of the matter, Nippon Steel’s business practices in 2021-2022 resulted in anti-dumping duties imposed on the Japanese steelmaker.

Mr. Goncalves apparently believes the deal will fall through and did voice Cleveland-Cliffs’ continued interest in an acquisition of USS; however, Mr. Goncalves will be reengaging with a much lower purchase price.

Corporate Reports

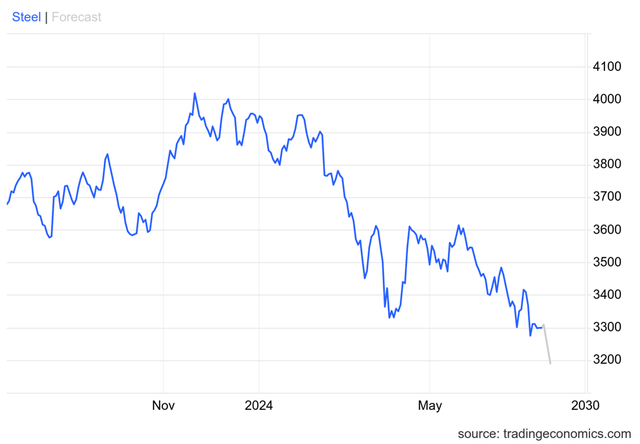

Concluding with financials, I anticipate the cyclical downturn to continue as steel prices are forecast to continue their decline.

TradingEconomics

My financial outlook for eFY25 includes the additional tons as a result of the Stelco acquisition, as well as some margin accretion resulting from the operational synergies discussed above. Though the wider aEBITDA margin Stelco brings forth won’t provide as broad of an impact as I’d like, the incremental improvement still makes a large difference on a per-ton basis.

Valuation & Shareholder Value

Corporate Reports

CLF is currently trading at 5.45x trailing EV/aEBITDA, a relative discount to its peer steel producers. Using an enterprise value-weighted multiple, we can come up with an average trading multiple of 5.96x. Plugging this figure into my forward estimate for eFY25 EBITDA, we can come up with a price target of $18.46/share.

Corporate Reports

Using an internal valuation metric, I believe Cleveland-Cliffs Inc. shares remain undervalued and will have room for growth in the long term. Though I do not anticipate any near-term excitement from shareholders as the industry undergoes a cyclical downturn, the firm remains opportunistic in growing their capacity through M&A at a time of low valuation multiples. Given the cyclical downturn and my optimism for the company, I will be downgrading my recommendation to a HOLD rating with a near-term price target of $18.46 based on TTM EV/aEBITDA. From a long-term perspective, I value CLF shares at $21.75/share at 6.34x EV/aEBITDA.

Corporate Reports

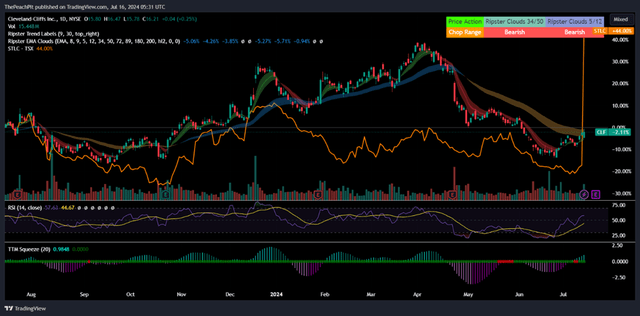

On a final note, it appears shareholders rewarded CLF shares post-announcement with an intraday gain before waning down to +25bps.

TradingView

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here