The tech stock rally we’ve seen so far this year has been nothing short of epic. That has dragged numerous stocks to relative highs, as this bull market has taken no prisoners, and is a rising-tide-raising-all-ships kind of situation. The broader market is extremely overbought, and so are countless stocks, including Cloudflare (NYSE:NET).

While I’m not trying to stand in front of this bull market, I do think there are prudent times to take profits when risks are elevated, and for Cloudflare, risks are quite elevated right now. For that reason, I’m slapping a sell rating on the stock.

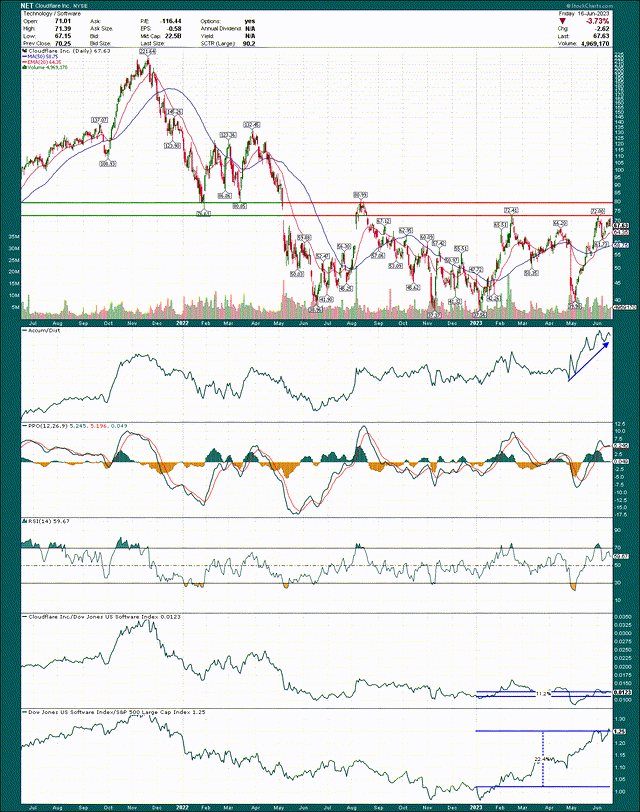

Heavy resistance ahead

Let’s begin with a look at the chart, which to me shows a lot of cause for concern if you’re bullish.

StockCharts

I’ve drawn in a zone of resistance that extends from roughly $72 to $80 and is the product of relative lows set in 2022, as well as relative highs this year. This zone of resistance should be extremely difficult to get through, given the length of time that the stock has spent below it. Should there be a breakout, the stock could be off to the races given the importance of this zone, but that’s not something I’d be willing to bet on at the moment.

The stock has massively outperformed this year, the product of the rally since the start of May. But the PPO and 14-day RSI are showing signs of weakness after being overbought a few trading days ago. As the stock approaches resistance with these negative divergences, the risk of selling increases.

From a technical perspective, if we get a breakout, you can ignore everything I just said. Should the stock breakout, use the breakout point as support. I do not think that’s likely given the state of the chart, and the bearish case is intact so long as shares remain below the $72/$73 level.

Growth in revenue, but is it enough?

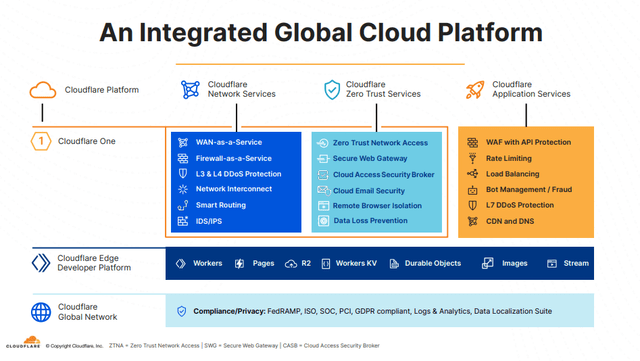

The company’s security platform works and its growth has been strong in recent years. During the COVID bull market, Cloudflare’s stock absolutely exploded and was building in obscene levels of growth in revenue. Those have since been unwound to what should be more reasonable (and achievable) levels of growth, but more on that in a bit.

Cloudflare investor presentation

The company’s platform offers a wide variety of security services, and while that’s great, it’s not exactly the only one that does this. The company continues to face rising competition, as it became clear years ago that cloud-based security services would be increasingly important, and countless companies jumped right in to grab a piece of the pie. Cloudflare has built a strongly integrated cloud security platform, but I’m not seeing a huge amount of advantage here over competitors.

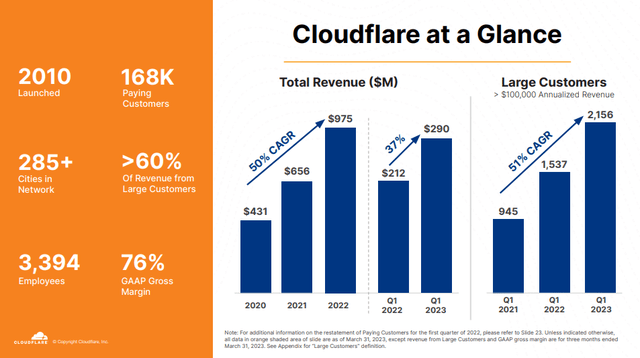

Revenue growth has been good, to be fair, and Cloudflare is building its book of large customers.

Cloudflare investor presentation

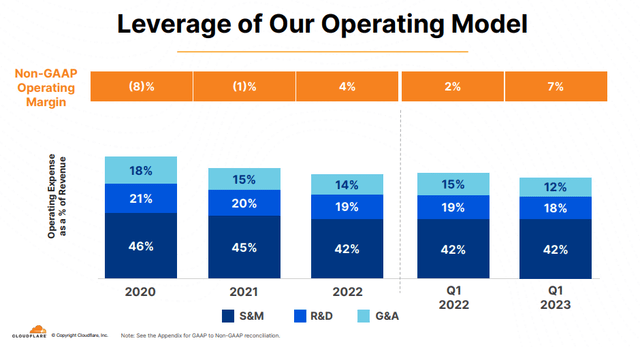

This is not to be overlooked, given large customers are the ones that help drive the topline the quickest. In addition, large customers can help leverage down costs, and Cloudflare’s gross margins are outstanding. The problem is that the company has been endlessly investing in future growth, and the profits simply aren’t coming.

Cloudflare investor presentation

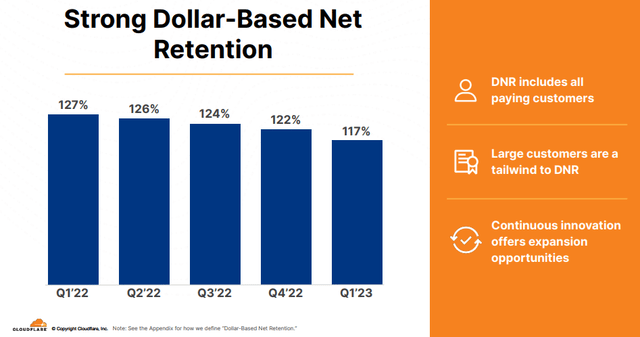

Dollar-based net retention is also declining and has been for some time. That will keep a lid on future growth as it means that future growth will rely more and more on new customers, rather than existing customers spending more. For me, this stat is one of the biggest things to be cautious about with Cloudflare’s topline potential.

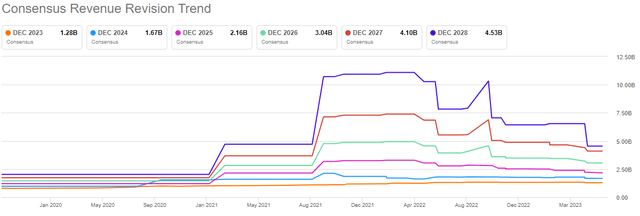

If we look at the estimates analysts have in place going forward, we can see the extent of the damage from the COVID peaks.

Seeking Alpha

We now see much more reasonable targets, but this is not a good look. Cloudflare may be a buy again when/if these start to turn up, but buying a revenue growth stock when revenue growth is flat to down like this is not a great strategy.

Cloudflare investor presentation

I mentioned margins above, and while the company has been able to leverage down some of its costs on an adjusted basis, it’s barely profitable on an operating basis, even with 75%+ gross margins. The company’s long-term plans call for reduced marketing spending, and we should see reduced SG&A as a percentage of revenue over time, but those things are a long way out. For that reason, sustained, meaningful profitability seems to be more of a hope than a reality at the moment.

This stock is still expensive

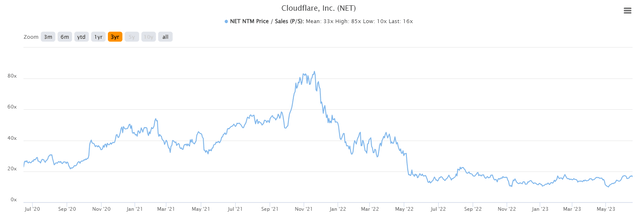

Cloudflare achieved one of the most expensive valuations I ever recall seeing during 2021 as it hit an eye-watering 85X forward sales. While those days are long gone, Cloudflare is still at 16X sales today, and I’m not sure I can justify that.

TIKR

Shares have hit 10X forward sales at the relative lows in the past year, so there’s potential for meaningful downside if the stock does indeed get rejected off of the zone of resistance we looked at on the chart. Eighteen times sales has been the relative top for this year, so the risk – to my eye – is lower on the valuation. Could the stock get more expensive? Absolutely it could, and that’s why we respect price support and resistance levels. But, in my view, it’s more likely we have downside risk than upside risk.

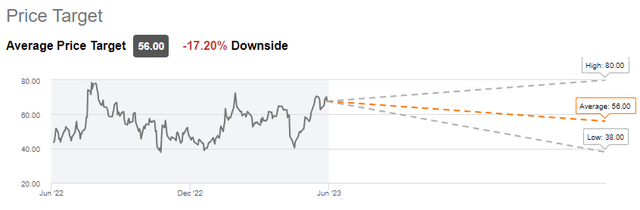

I’m apparently not the only one, as analysts are actually pretty bearish here.

Seeking Alpha

There aren’t many stocks that show double-digit downside in terms of price targets, but I get it. The chart is looking like it has stiff headwinds ahead, and the valuation is getting stretched again relative to price action in 2023.

If Cloudflare was seeing rapidly improving profitability, or had rising revenue estimates, maybe I’d feel differently. But those things aren’t happening, and I just see a stock that’s weakening into stiff price resistance, declining dollar-based net retention, and flat to down revenue revisions. At 16X forward sales, it is my opinion that Cloudflare is too expensive, and I’m hitting it with a sell rating. This is about managing the risk/reward equation, and for me, the risk is simply too high to buy or hold this stock.

Read the full article here