A Quick Take On Cognyte Software

Cognyte Software Ltd. (NASDAQ:CGNT) provides security analytics and related software functionalities to governments and organizations worldwide.

I previously wrote about Cognyte with a Neutral [Hold] outlook.

Cognyte Software Ltd. management is expecting continued improvement in gross margins, but revenue growth may elude the company despite demand for AI initiatives.

I remain Neutral [Hold] on CGNT until revenue growth can show material improvement.

Cognyte Overview And Market

Established in 2020, Israel-based Cognyte has developed a software platform aimed at aiding security investigations for governments and enterprises.

The firm is led by CEO Elad Sharon, former president of Verint Systems.

Cognyte’s key products include an analytical platform that scrutinizes environments such as networks, blockchains, the Internet, cyber threats, and situational intelligence.

The company pursues new customers through direct sales & marketing efforts and collaborations with partners.

Cognyte serves several national agencies, including the U.S. NSA and different law enforcement entities.

A 2021 report from MarketsAndMarkets indicated that the security analytics market was valued at approximately $12 billion in 2021.

Demand for security analytics is projected to exceed $25 billion by 2026, with a robust CAGR of 16.2% between 2022 and 2026.

This expected growth is attributable to the escalating landscape of threat scenarios, characterized by the growth in attack counts and the intricate nature of security infringements.

Also, there is increasing demand among corporations for advanced systems to thwart recurring attacks and uphold regulatory adherence.

The momentum in the adoption of machine learning and AI-powered systems is expected to persist due to the increasing need for enhanced automation in surveillance and reaction processes.

Other key players or significant competitors in this industry include:

-

IBM (IBM)

-

Cisco (CSCO)

-

Broadcom (AVGO)

-

Splunk (SPLK)

-

RSA Security

-

FireEye

-

LogRhythm

-

Securonix

-

Hillstone Networks

-

Exabeam

-

Rapid7

-

Alert Logic

-

Snowflake

-

Others.

Cognyte’s Recent Financial Trends

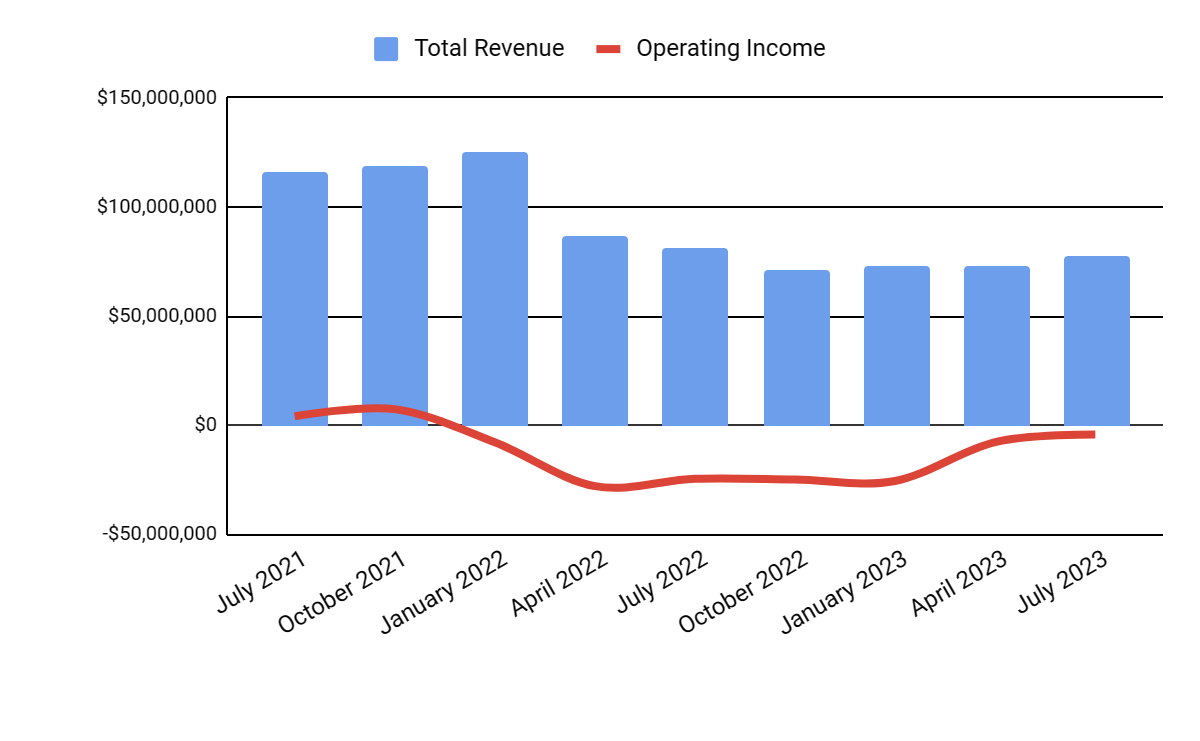

Total revenue by quarter has begun to trend upward again in recent quarters; Operating income by quarter has made progress toward breakeven:

Seeking Alpha

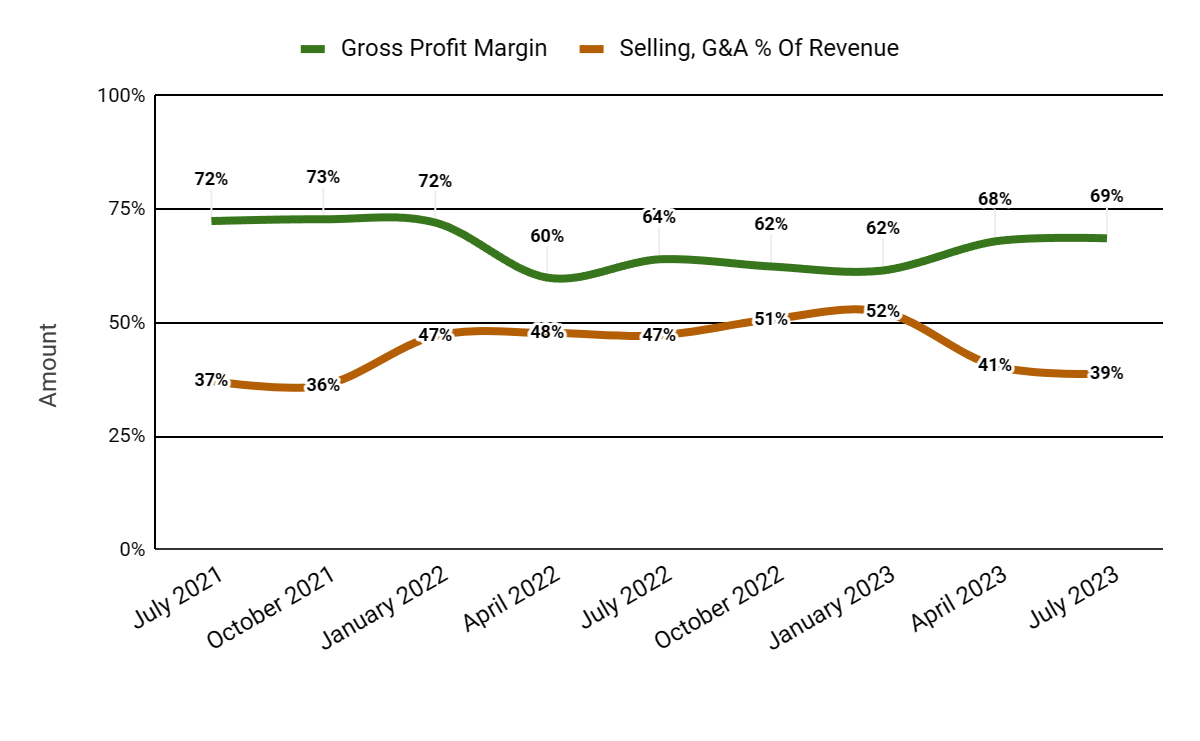

Gross profit margin by quarter has improved in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter have dropped substantially more recently:

Seeking Alpha

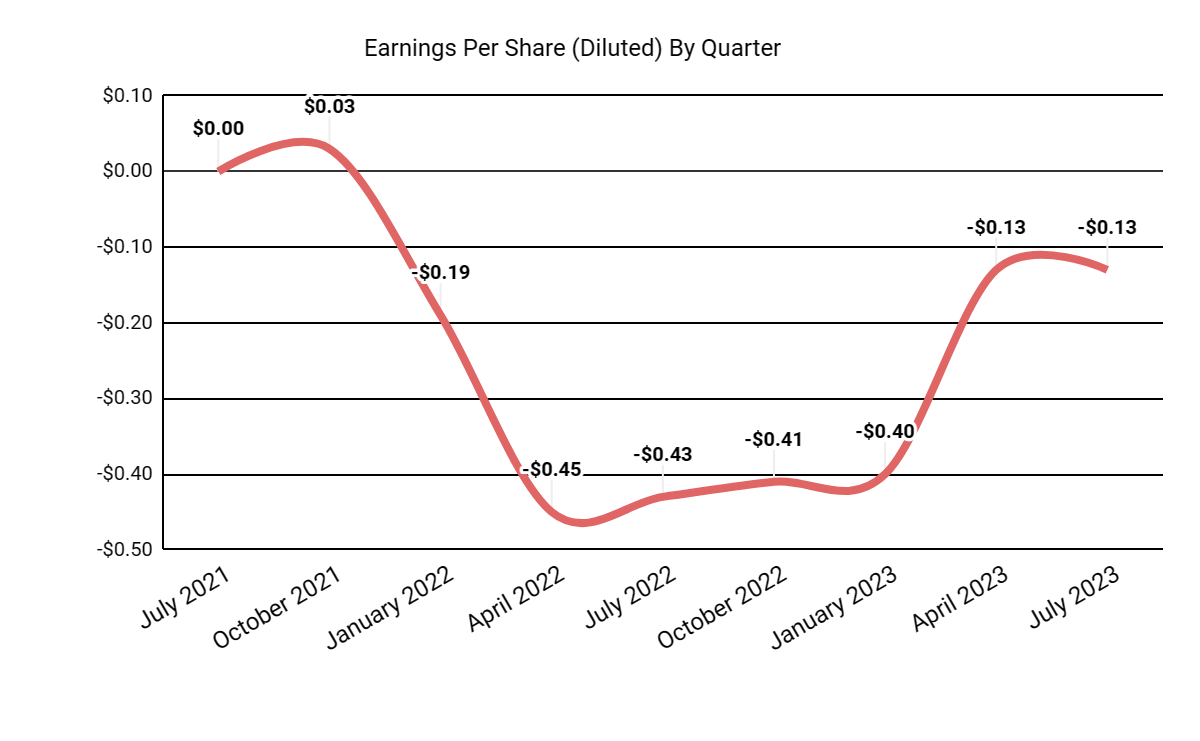

Earnings per share (Diluted) have made significant progress toward breakeven but still have a ways to go:

Seeking Alpha

(All data in the above charts is GAAP.)

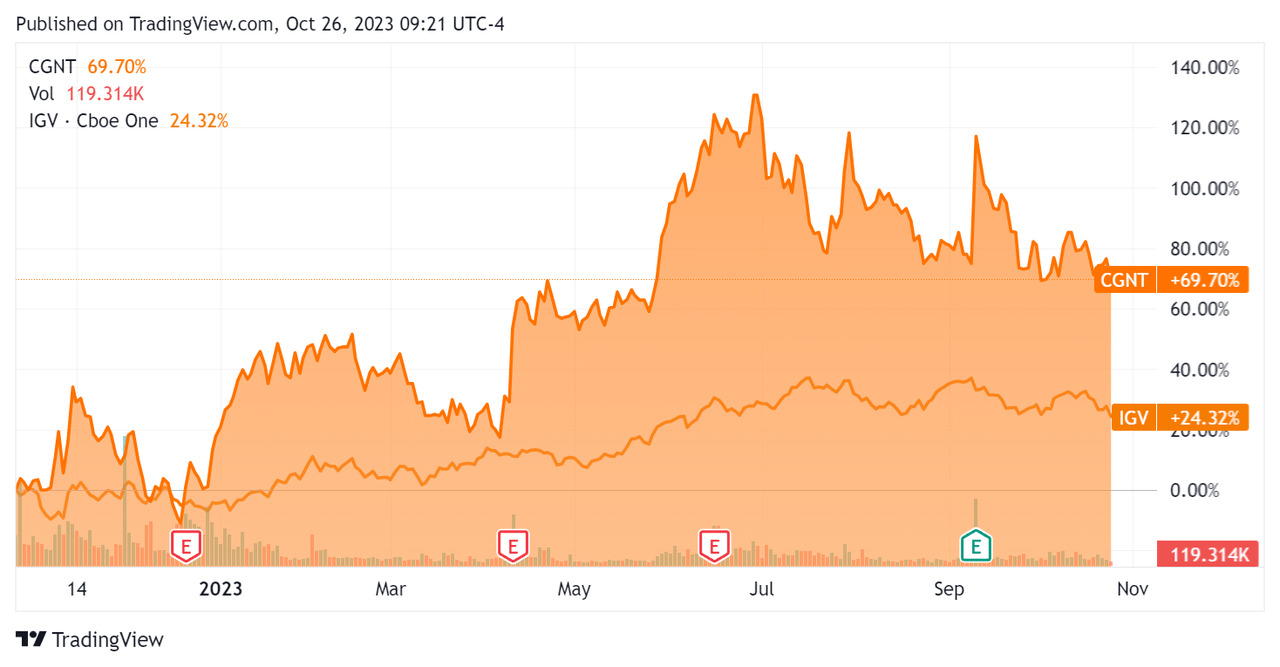

In the past 12 months, CGNT’s stock price has risen 69.7% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) growth of 24.32%:

Seeking Alpha

For balance sheet results, the firm ended the quarter with $72.5 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was $8.7 million, during which capital expenditures were $7.1 million. The company paid $18.4 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Cognyte

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure (Trailing Twelve Months) |

Amount |

|

Enterprise Value / Sales |

1.0 |

|

Enterprise Value / EBITDA |

NM |

|

Price / Sales |

1.1 |

|

Revenue Growth Rate |

-28.2% |

|

Net Income Margin |

-24.8% |

|

EBITDA % |

-16.6% |

|

Market Capitalization |

$327,680,000 |

|

Enterprise Value |

$280,020,000 |

|

Operating Cash Flow |

$15,750,000 |

|

Earnings Per Share (Fully Diluted) |

-$1.07 |

|

Forward EPS Estimate |

-$0.34 |

|

Free Cash Flow Per Share |

$0.08 |

|

SA Quant Score |

Hold – 3.38 |

(Source – Seeking Alpha.)

CGNT’s most recent unadjusted Rule of 40 calculation was negative (33.7%) as of FQ2 2024’s results, so the firm is in need of significant improvement in this regard, per the table below:

|

Rule of 40 Performance (Unadjusted) |

FQ1 2023 |

FQ2 2024 |

|

Revenue Growth % |

-2.0% |

-28.2% |

|

Operating Margin |

-2.0% |

-5.4% |

|

Total |

-4.0% |

-33.7% |

(Source – Seeking Alpha)

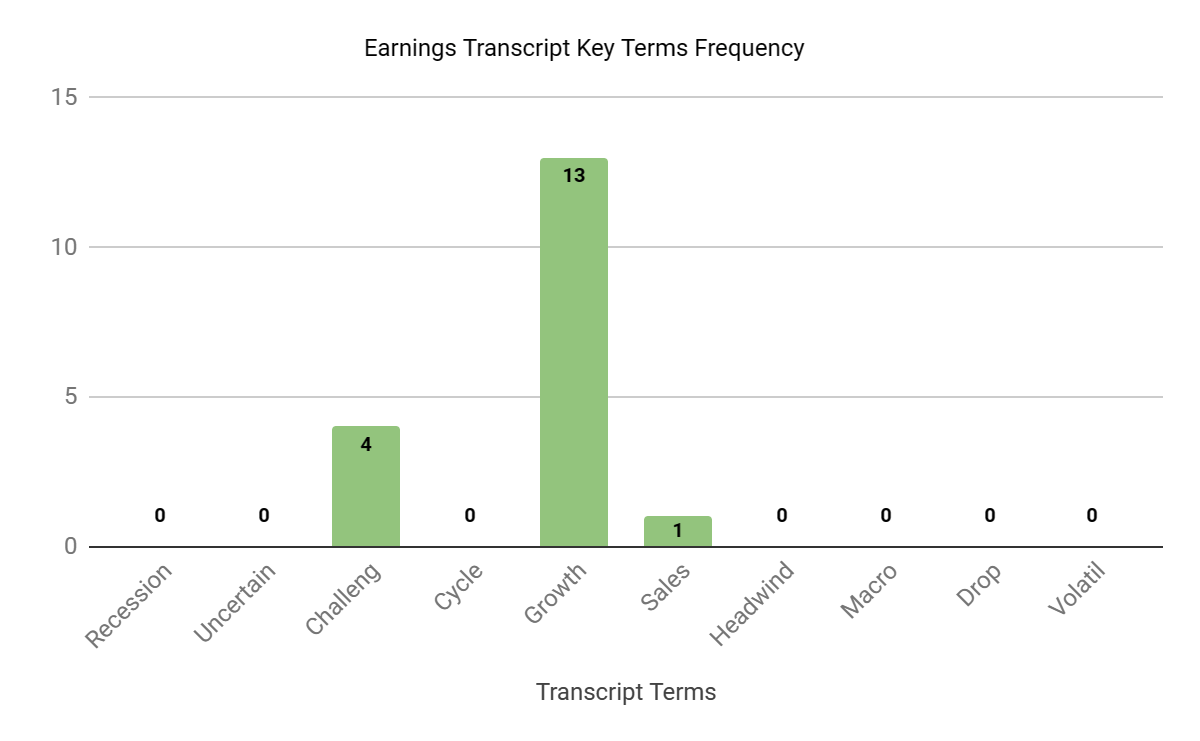

Sentiment Analysis

The chart below indicates the frequency of various keywords in management’s most recent earnings conference call:

Seeking Alpha

Management has taken a number of actions to address the challenges the company has faced with its previous year’s results.

The sole analyst on the conference call asked about the company’s AI capabilities and use cases, an increase in professional services revenue and the reasons for improved gross margins.

Management responded that AI functionalities are helping customers improve the accuracy, speed and success rates of their investigations.

The spike in professional services revenue can vary between quarters, and any larger deals would typically have this type of revenue recognized over several quarters.

On the issue of improved gross margin, management said that their previous actions to reduce the cost structure of their professional services offering have improved gross margins, in addition to the quality of their backlog.

Commentary On Cognyte

In its last earnings call (Source – Seeking Alpha), covering FQ2 2024’s results, management’s prepared remarks highlighted revenue beating expectations and additional improvement in gross margin, up 4.5% year-over-year.

The firm is investing substantially in AI-enabled capabilities, and leadership is seeing these enhancements as key drivers for future growth prospects.

Management didn’t disclose any customer or revenue retention rate metrics.

Selling and G&A expenses as a percentage of revenue fell 8.4%, indicating improving efficiency in this regard while operating losses improved markedly to only ($4.2 million) for the quarter.

The company’s financial position is solid, with plenty of liquidity, no debt and positive free cash flow.

However, CGNT’s Rule of 40 performance has been very poor due to the firm’s declining revenue base over the last several quarters, although the most recent quarter has produced sequential growth.

Looking ahead, management raised its revenue guidance for fiscal 2024 to $307 million, or a decline of 1.7% versus the previous fiscal year.

If achieved, this would represent a reduction in revenue decline rate versus fiscal 2023’s contraction rate of 34.2% versus fiscal 2022.

In the past twelve months, the firm’s EV/Sales valuation multiple has increased by approximately 102%, as the chart from Seeking Alpha shows below:

Seeking Alpha

A potential upside catalyst to the stock could include demand growth from its AI-related initiatives.

Management expects positive adjusted EBITDA for fiscal 2024 due to improved stability in demand.

However, expected revenue growth from AI projects may take several quarters to materialize and show up in the firm’s financial results.

Despite growing gross margins due to reduced professional services costs, given the still-tepid revenue guidance for fiscal 2024, my outlook on Cognyte Software Ltd. stock is Neutral [Hold].

Read the full article here