Introduction

CoreCard (NYSE:CCRD) is an American technology firm specializing in financial technology services, and it’s been in business since 1973. With its primary base in Norcross, Georgia, the company provides technology solutions and data processing services specifically designed for the FinTech sector. The company has extended their global reach through strategic partnerships in various countries, including Romania, India, the United Arab Emirates, and Colombia. While the primary administrative tasks, including human resources and executive decision-making, are carried out at the Georgia headquarters, the overseas subsidiaries focus mainly on software development and data processing tasks.

Revenue Streams and Business Growth

CoreCard’s financial performance is closely tied to two main factors: the sale of software licenses and the acquisition of high-value service contracts. Interestingly, the company has seen more robust growth in its data processing segment than in its software licensing, leading to a consistent increase in revenue. CoreCard has a strong financial footing, thanks largely to its contract with Goldman Sachs, which accounts for 70% of its total revenue. This strong dependency has led to a steady revenue stream but also brings up concentration risk—a significant portion of CoreCard’s financial health hinges on this relationship.

Key Takeaway

Investors should closely monitor CoreCard’s dependency on Goldman Sachs for revenue. Although this partnership has been lucrative, it poses a significant concentration risk.

Revised Agreement with Goldman Sachs

CoreCard has made a strategic move by revising its Statement of Work agreement with Goldman Sachs. The payment structure has been converted from a Time and Material model to a fixed monthly fee adjusted for inflation. While this brings in a more stable, recurring revenue from Goldman Sachs, it’s essential to note that the financial outcomes of this change are subject to multiple uncontrollable variables, like fluctuations in Goldman’s number of active accounts. If Goldman Sachs sees a decrease in its customer base or shifts its priorities, this could trickle down CoreCard’s expected revenue, making it a less predictable income stream than it initially seems.

Key Takeaway

This revised agreement is particularly important for investors because Goldman Sachs accounts for a significant portion of CoreCard’s total revenue. The potential concentration risk here is twofold:

-

If Goldman Sachs decides to sever or downgrade its partnership with CoreCard, it could seriously impact CoreCard’s financial health.

-

The fixed monthly fee model introduces new external risks that can affect CoreCard’s expected revenue, making future performance harder to predict.

Operational Scalability and Cost Structure

CoreCard has built a business model that can effortlessly adapt to the influx of more customers. While this strategy has contributed to its ability to service an increasing customer base, it also presents challenges tied to talent management and operational costs.

The company has strategically expanded their international footprint by opening offices in Dubai in 2020 and Colombia in 2021. These locations don’t just cater to existing clients but also allow CoreCard to tap into new markets. The setup seems ideal for handling increased volumes of business without sacrificing efficiency.

On the upside, CoreCard’s new international offices can lead to diversified revenue streams, making the company less susceptible to local economic downturns. However, these expansions also mean that CoreCard must now navigate different labour laws, business environments, and cultural challenges, adding complexity to its operations.

While scaling operations looks good on paper, success largely depends on CoreCard’s ability to hire the right talent and train them effectively. The company’s primary expenses come from employee salaries across various international locations. Thus, the cost of a bad hire or ineffective training isn’t just a short-term problem; it could affect long-term operational scalability.

Key Takeaway

While CoreCard seems well-positioned for scalability, success correlates directly with effective hiring and talent management, particularly in international locales.

Financial Resilience

CoreCard has a solid financial cushion, with $36 million in cash reserves as of the most recent reporting, providing stability and room for growth. The company aims to use these reserves to bolster its primary business functions. This could mean anything from improving existing services and products to ramping up marketing activities. Moreover, CoreCard is open to using this liquidity for potential acquisitions of complementary businesses, thus diversifying its offerings and expanding its customer base.

Stock Buybacks

The company’s board has greenlighted a stock buyback program worth $10 million. So far, they have spent $0.4 million in the first half of 2023 and $3.7 million during the first half of 2022. While these figures don’t fully utilize the allotted budget, they indicate a steady commitment to the program. They still have approximately $17.9 million allocated for future stock buybacks, showcasing their confidence in the company’s value.

Performance Metrics

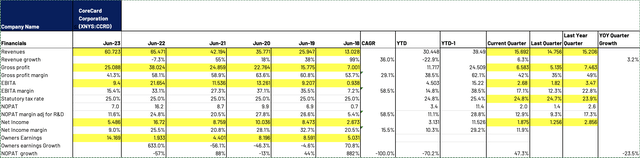

For the first quarter of 2023, CoreCard earned $15.69 million, a modest 3% growth compared to the same quarter last year. However, the revenue for the first six months was $30.448 million, marking a 23% decline year-over-year. These numbers underline the unpredictable nature of CoreCard’s business, influenced by myriad factors such as market demand, competition, and cost of goods sold. Most of their revenue comes from services, which have shown promising growth, particularly in transaction handling and software maintenance. However, forecasting future earnings from professional services remains a challenging task.

Software Licensing

The company generated $1.794 million through software license sales in the first half of 2023, plummeting from $14.28 million in the same period last year. This is a massive drop because last year’s numbers included a big, one-time deal.

Key Takeaway

Revenue streams at CoreCard are a mixed bag. While the services sector shows strength, revenue from other sectors has fluctuated more, making the overall income less predictable. This raises questions about the long-term stability of the company’s revenue streams.

Expense Metrics

Costs comprised 59% and 63% of total earnings for the first three and six months of 2023, a noticeable jump from last year. This increase is mainly attributed to additional hiring and capital investment in technological infrastructure, including server spaces and computer equipment.

Research and Development

Interestingly, the company has restructured its R&D spending. They’ve cut back on employee bonuses but have hired more tech talent domestically and internationally. This suggests that CoreCard is doubling down on innovation.

Advertising and Customer Acquisition

Spending on advertising saw a surge of 24% in the first quarter and 15% in the first six months year-over-year. However, the company has effectively leveraged online platforms for customer acquisition, allowing them to spend comparatively less on traditional advertising channels.

Key Takeaway

CoreCard’s increasing investment in technology and human resources is a double-edged sword. While it indicates the company’s commitment to growth, it also threatens short-term profitability.

Cash Reserves and Liquidity

As of June 30, 2023, CoreCard boasted a healthy cash reserve of $31 million, up from $20 million at the end of the previous year. Between January and June 2023, operational activities generated $15 million in cash flow, significantly higher than last year. This increase is mainly due to improved accounts receivable and deferred revenue management.

Investments and Future Plans

The company invested $4 million to upgrade its technological infrastructure, particularly in their Indian office. They have also continued to buy back shares, indicating confidence in the company’s growth prospects.

Valuation

Last 5 year Financials

Historical Revenue Growth

In the past decade, the company has showcased impressive growth. Specifically, the firm grew at a 36% Compound Annual Growth Rate for the last 5 years and at 15.6% for the last 10 years. This historical growth trajectory gives investors confidence in the firm’s ability to generate revenue consistently.

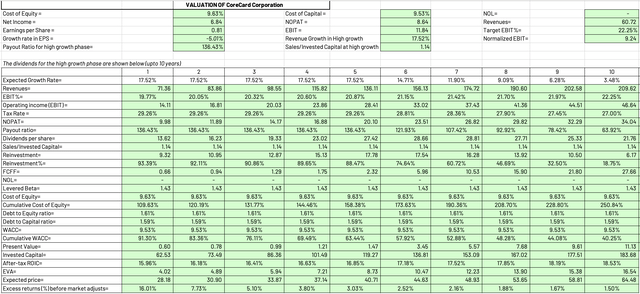

The company actively invests in employee skill development and tech infrastructure, which are key pillars for future revenue growth. Based on these factors, my Discounted Cash Flow valuation projects a reasonable growth rate of 17.5% over the next five years.

Return on Invested Capital has been rising for the last three years, mainly because of those healthier gross margins and efficient use of capital. But this year, the ROIC dropped to 21.4% from 47% due to increased competition and market changes.

EBITA Margin Analysis

Over the past five years, the company’s EBITA margin grew at a staggering 58.5% CAGR. However, the last year saw a dip, with margins falling to 15.5% from an average of 33% during 2019 to 2022 TTM (Trailing Twelve Months). Fortunately, this dip may be temporary. The company has revised its payment terms with Goldman Sachs, moving to a recurring revenue model that should reduce General and Administrative (G&A) costs. As a result, I predict an improvement in EBITA margins from 15.5% to 19.7% in 2024, and eventually to 22.25%, fueled by continual investments in human and tech resources.

Capital Efficiency

The company’s Sales-to-Invested Capital ratio is another key indicator of its efficiency and profitability. Over the last five years, the company has had an average Sales/Invested Capital of 2.1, meaning it generated $2.1 in revenue for every dollar invested. However, this ratio has declined to 1.5 in the last year and I assume the same in my DCF model. While the company expects this metric to remain stable due to less capital-intensive growth in its professional services segment, competition could eat into profit margins. Therefore, I’m aligning my expectations for their EBIT margin with the industry average of 22%.

Finally, the cost of capital I’ve calculated is 9.53%, with a 4.31% equity risk premium, a 3.5% risk-free rate, and a levered beta of 1.43.

DCF model

Based on these numbers, I’ve calculated an intrinsic value of $22.53 per share, while the current stock price is $22.43. Therefore, I consider the stock fairly valued. In light of the associated risks—primarily the heavy dependency on Goldman Sachs—the stock appears to be a risky bet for conservative investors.

Conclusion

-

Dependency on Goldman Sachs: CoreCard has a significant portion of its revenue from Goldman Sachs, marking it as a potential risk factor. While dependency on a single client is not necessarily bad, it does bring about questions about the diversification of the client base. Mitigating this risk would involve broadening the customer portfolio.

-

Business Model Scalability: The company has the potential for scalability, evident from its international presence through multiple global offices. However, the crux of successful scaling lies in effective hiring and talent management. Operational efficiency is tightly knit with the company’s ability to find and train the right people.

-

Financial Resilience: With $36 million in cash reserves, CoreCard is in a solid financial position. This can be advantageous for future growth and even to weather business downturns.

-

Unpredictable Revenue: CoreCard’s revenue streams are a mixed bag. Although showing strong performance in the services sector, there are fluctuations that make the revenue somewhat unpredictable. This volatility could be a concern regarding the company’s long-term stability.

-

Costs and Investments: They’re spending more on technology and human resources, which is good for growth but might impact short-term profitability.

Until CoreCard can demonstrate a more diversified client base and a clearer path towards stable, long-term revenue, it remains a volatile yet potentially rewarding investment option for those who can stomach the risk.

Read the full article here