Over the last couple of weeks, the Mexican ruling party has proposed new reforms aimed at the judicial system, where judges would be elected by popular vote, rather than being selected by merits. Since the news hit the media, the Mexican peso has depreciated by about 4%, which reflects how investors feel about the proposed change to the constitution.

While the reform is controversial and has some investors worried, the nearshoring trend that started a couple of years ago is still in place and can make up for the changes in the political system, and what better way to play the trend than with Corporacion Inmobiliaria Vesta (NYSE:VTMX) (OTCPK:VESTF) a real estate operating company focused on logistics and warehouses properties.

Nearshoring

To understand the value that Vesta offers to investors, it is necessary to first understand what nearshoring is, and we could summarize it as the process of relocating production facilities near or close to the United States. This trend was of particular relevance after COVID-19, as China and other Asian economies were forced to close their borders and manufacturing companies to avoid contagion, this had the effect that many goods that relied on foreign manufacturing came to a halt.

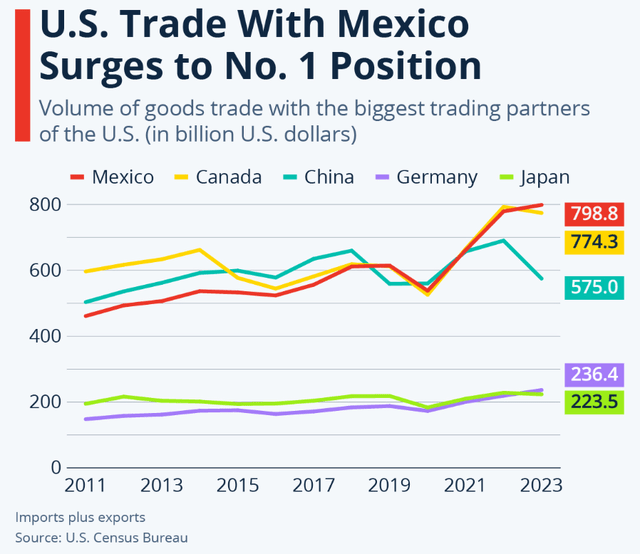

The COVID-19 crisis was one of the main reasons for companies wanting to relocate as cracks began to appear on having a globalized and interconnected economy, nevertheless, the trend started back in 2018 when frictions between the United States and China started materializing and the trade war started. Since the conflict started, Mexico has been slowly increasing its trade with the United States and in 2023 became the number one trading partner after surpassing China and Canada.

Statista

Even if the trend started due to a trade war, the benefits for US companies are too good to be ignored, for instance, a container traveling by ship to New York from China takes approximately 32 days, the same container traveling from Mexico takes only 5 days. That is almost a month difference, which can be the distinction between having happy rather than disappointed customers.

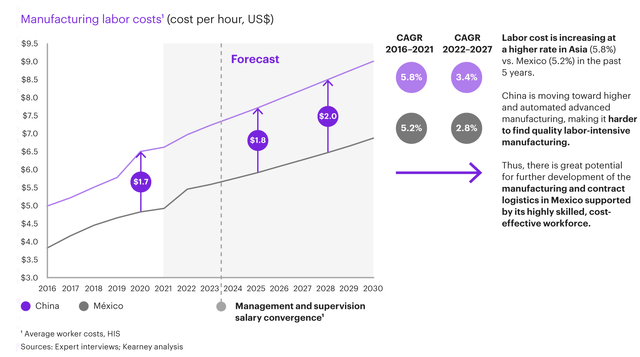

However, not only is distance a huge advantage, but also the differences in labor costs are significant. According to a study done by Kearney analysis, Chinese manufacturing costs are expected to grow at a 3.4% CAGR between 2022-2027, whereas in Mexico, the increase is expected to be around 2.8%. Therefore, in 2027, a Chinese worker could cost $7.5 an hour versus $5.0 an hour for a Mexican worker, which is almost a 50% difference.

Kearney

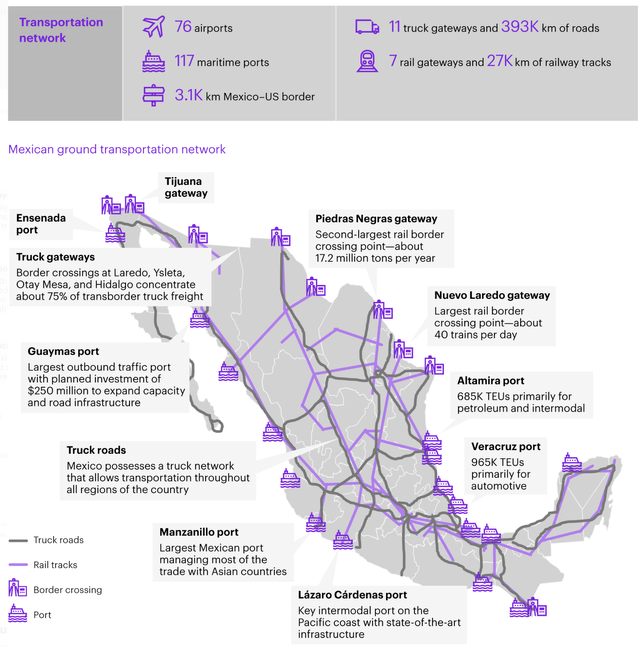

Even if the proximity and cost advantages are better compared to China it would not matter if there is not an efficient way to deliver the products, but the reality is that Mexico offers a wide range of infrastructure and transport options making it a reliable source to take merchandise from point A to point B. The Mexican government committed more than $30 billion in 2022 to update its infrastructure and among those projects is a potential competitor to the Panama Canal, whereby Mexico is linking the Atlantic and Pacific oceans using a new railroad network.

Kearney Analytics

Companies have already started to notice the benefits that Mexico offers, as Walmart already did by buying uniforms from a family-run business in Mexico rather than from its usual supplier in China.

Another proof of the growing business relationship between Mexico and the US is the recent acquisition of Estafeta a 45-year-old logistics and package delivery company by UPS (NYSE:UPS), in the announcement they mentioned that the motivations behind the acquisition were the booming manufacturing sector, relocation of supply chains and growing commerce between North America.

The Company

As detailed below the Nearshoring narrative has already happened and is expected to carry on into the future, nonetheless, who are the players mainly expected to benefit from it? At a glance, this has the potential to positively impact the whole economy and thus most enterprises, nevertheless if we do a zoom in this trend is expected to happen in different phases with the first one being construction, warehouses, and transportation, the second internal consumption and the last one infrastructure and technology.

The first phase is already happening and leaders and beneficiaries are already showing up and within this winner, Vesta is a company worth looking at.

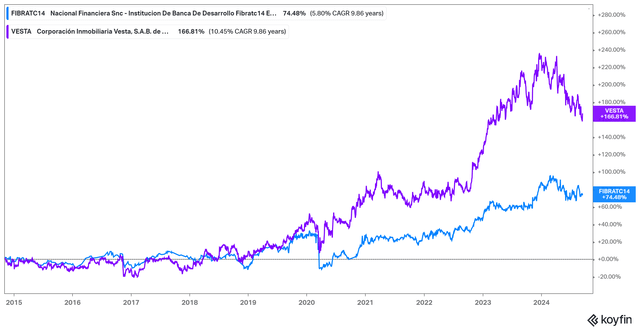

Vesta has been a standout performer in the Mexican real estate market, over the last 10 years it has delivered a 10.45% CAGR return for shareholders, whereas the whole market (measured by the FIBRATRAC ETF) has returned 5.80% CAGR. That’s almost twice the difference, they must be doing something different to earn those superior returns.

Koyfin

Below are the main drivers that have allowed Vesta to differentiate from competitors:

- Vesta has more than 216 properties, and while it’s not the biggest player, it has a location advantage, as all of their properties are located in important manufacturing and distribution hubs, such as the north of the country and the bajio and central region, all of which account for more than 60% of Mexico’s GDP.

- The company offers pre-designed buildings and industrial parks; however, they have the option of constructing custom-made buildings, allowing for more consumer stickiness.

- Their properties portfolios are distributed between 40% logistics and 60% manufacturing, both sectors positively correlated to the nearshoring theme.

- 88%of rental income is denominated in USD, which creates an important hedge to FX movements, especially given the current volatility that surrounds the political landscape.

- Portfolio diversified in more than 10 different industries and no client represents more than 5% of the total leased space.

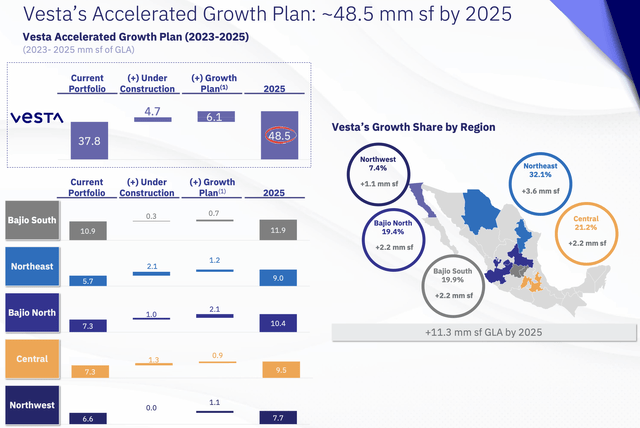

Their current financial position is well positioned for the future, as they have plans to increase their capacity by almost 11.3 million SF by 2025. Their current balance sheet has more than USD 377M and their average CAPEX expenditure is between USD250-300M; thus, they can support 1 year of CAPEX without relying on external financing.

Vesta 2Q Presentation

Leaving aside their strong liquidity position, their current LTV is 23% and their internal policy allows them to reach a maximum leverage of 40%. The Net Debt/Total Assets is 13.5% and their Net Debt/EBITDA is 2.8x; therefore, they have enough room to expand their debt capacity and continue their expected growth.

So far, Vesta is a major beneficiary of the nearshoring trend, offers best-in-class properties, has ambitious growth plans, and a strong financial position to carry their strategy. But what about how their profitability?

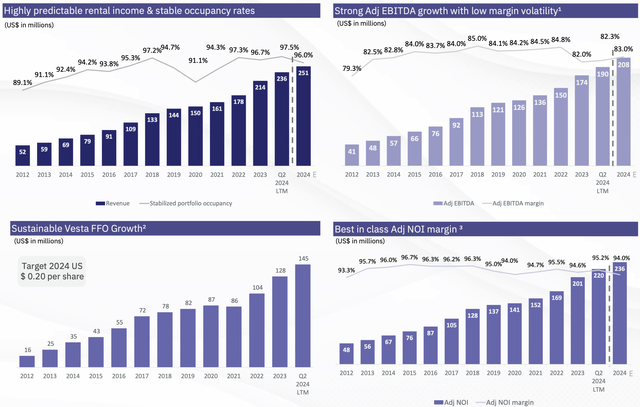

Since 2012 (IPO date) Vesta’s rental income has grown at an annual rate of 14.02% and has had an average occupancy rate of 94.34%, even during the pandemic their occupancy rate was at manageable levels of 91%. Their NOI income has grown at a 14.19% annual rate, very close to rental incomes, suggesting a low-cost structure, and the average NOI margin has been 95%. In summary, what Vesta offers is stable and predictable cash flows in a market with a lot of growth opportunities.

Vesta’s 2Q Presentation

The Value

The task of any manager is to create value for shareholders, which simply implies investing in projects that generate returns above their required return or the company’s cost of capital.

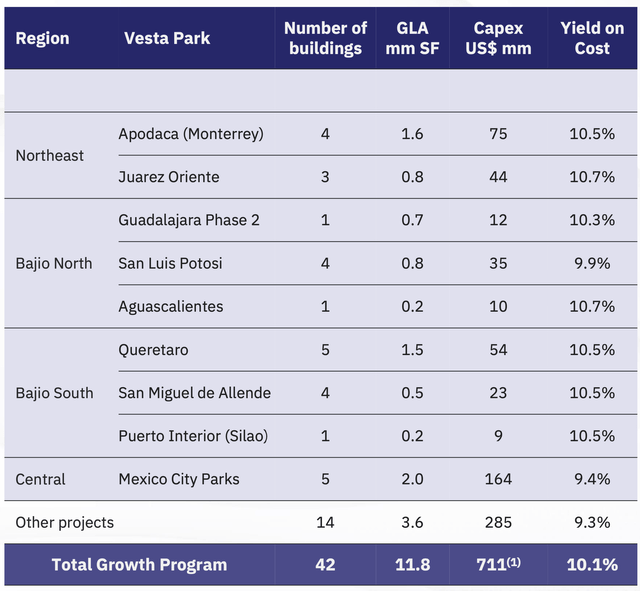

Vesta already has many projects under construction, all of which have an average yield of cost or expected return of 10.1%. For managers to be creating value, the company’s cost of capital should be below this number.

Vesta 2Q Presentation

To arrive at the cost of capital, we use the following data:

- Equity value: The MXN price is $59.9, multiplied by the current shares outstanding of 882.49 and adjusted by an FX of $19.2 yields a market cap of 2,753.18 million USD.

- Debt Value: The current debt is $944.60.

- Cost of Debt: They currently have a weighted cost of debt of 4.48% due in about 4.3 years; however, this debt adjusted by the Mexican marginal tax rate gets us an after-tax cost of debt of 3.14%.

- Cost of Equity: The current yield on a US 10-year treasury bond is 3.66%. The company’s beta is 0.87 and the Equity Risk premium is calculated by using the implied US ERP of 4.06% and adding the Mexican market spread of 1.69%. All of this data used as input in the CAPM formula returns a cost of equity of 8.66%

- Capital Structure Weights: Using the current market cap and debt value, we get that the company finances its operations with 74% equity and 26% debt

- Total Cost of Capital: The cost of capital for the company given the inputs above is 7.25%

The current return that both shareholders and lenders require is 7.25% and Vesta is investing this capital at a 10.1% rate; therefore, the company is value accretive and generating positive shareholder returns. This simple exercise demonstrates that management is taking the right actions and shows their competency in managing the company.

Investing in projects above their required hurdle rates shows management skill, but even if Vesta adds value, if you pay a high price for the stock all these benefits can quickly be diluted. Currently, Vesta shows an attractive entry point as it is trading at a LTM P/BV of 0.90x against its five-year average multiple of 1.00x, which translates into an 11.11% discount. As the graph below shows the company during 2023 and half of 2024 was trading at 1x standard deviation above its mean, since then, it has come down to more attractive buying levels.

Koyfin

Risks

Country Risk:

Mexico is an emerging economy and as such is vulnerable to all the risks this entails, such as economic and political risks. At the beginning of the article, the new changes to the constitution were mentioned, while their impact is yet to be known as the new president, Claudia Sheinbaum is yet to take control and much of the reform hangs on whether she will execute it as it currently is or if she will be more moderate on its execution, nonetheless, the potential impact it can have on the country, in the long run, can be material as it might create conflicts of interest between the legislative and judicial power.

Currency Risk:

Vesta is a Mexican company that trades both in Mexico and USA via an ADR, where each share in Mexico is equal to 10 shares in the United States and adjusted by the USD/MXN parity. The Mexican peso is one of the most liquid currencies in the world and during economic periods of stress, it can quickly lose value. At the beginning of the year, the spot exchange was at 16.80 today is close to 19.20 a 14% depreciation in 9 months. Given the substantial depreciation in 2024 it is less likely that it can depreciate further, but should a risk-off event happen the value of the company can be impacted by the economic and FX volatility.

Productivity Risk:

Mexico offers both a better location and cheaper labor compared to most Asian economies; however, these advantages can evaporate if Mexican workers become less productive, which would mean that they cost less but also produce less.

Competition Risk:

Given the attractive market potential for manufacturing and distribution hubs, many REITs and real estate operating companies are shifting their real estate portfolio, such as Fibra UNO (OTCPK:FBASF) which recently tried to do a Spin-Off of their industrial real estate portfolio to better capture value. Given this competition, the market could get saturated, and be difficult for the company to find profitable investment opportunities.

Conclusion

Economy is the science of studying scarce resources, and there is nothing more scarce in this world than land; you simply can’t create more of it. Companies that own it in strategic locations have the potential to use this scarce and valuable asset in their favor, and Vesta has land and facilities in the best possible strategic location.

Buying the company gets you competent management, attractive valuation, sound financial position, operating stability coupled with predictable income, and finally participation in a trend that has enormous potential and that is no longer a dream but rather a reality that is already happening.

Read the full article here