In the last few days, it was reported that Costco Wholesale Corporation (NASDAQ:COST) is cracking down on membership sharing which has obviously become an ever-increasing problem for the retailer. And when reading about the illegal use of memberships, one will think of Netflix (NFLX) right away as the streaming giant made a similar move a few months ago.

In the following article, I will take a closer look at Costco’s decision and try to put it into context – not only by looking at Netflix, but also by looking at other retailers like Target (TGT). And we will discuss what implications this might have on the business and the stock’s valuation.

Quarterly Results

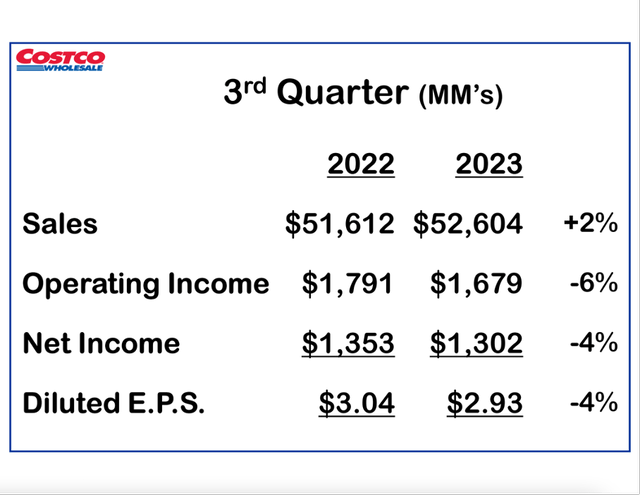

Since my last article was published, Costco reported third quarter results. And although this is not the main topic of this article, I like to give a quick update. Costco missed revenue estimates by $930 million but could beat non-GAAP EPS estimates by $0.12.

When looking at the twelve-weeks ended on May 7, 2023, Costco increased its total revenue slightly from $52,596 million in the same quarter last year to $53,648 million this quarter – resulting in 2.0% year-over-year growth. And while the top line still increased, operating income declined from $1,791 million in Q3/22 to $1,679 million in Q3/23 – resulting in 6.3% year-over-year decline. And diluted earnings per share also declined 3.6% year-over-year from $3.04 in Q3/22 to $2.93 in Q3/23.

Costco Q3/23 Presentation

Looking at comparable sales for the third quarter, we see a slight increase of 0.3% and when looking at the adjusted numbers (which are excluding the impact of changes in gasoline prices and foreign exchange rates), comparable sales increased 3.5%. And it is worth mentioning that e-commerce sales declined 10% YoY.

And when looking at revenue, net sales increased 1.9% to $52,604 million and membership fees increased 6.1% to $1,044 million. I mention this as the membership fees (and number of memberships) will be one of the topics we will focus on in this article.

Costco Membership

I assume most are familiar with the Costco membership business model and therefore its privileges and conditions. And so far, they have not changed. However, the problem that apparently was arising in the last few months is people and “customers” misusing membership cards. The New York Times described the loophole customers found:

But for friends and relatives of members, there was a well-known hack for scoring Costco’s low prices without paying an annual fee: the self-checkout lanes. Some users found they could borrow a member’s card, or a member’s QR code from the Costco app, and avoid the identification requirements of the regular checkout lanes.

But now, Costco employees are asking shoppers to show a member card with their photos at self-checkout or if it is a card with a photo, they are asking for additional ID. This was already custom for “regular” checkout lanes, but not at the self-checkout lanes.

Additional Shoppers are Great News, Right?

This might be a question one might ask right away. And what could be true for most other retailers, is not true for Costco. There is a reason you need a membership at Costco, while you don’t need a membership at most other retailers for shopping.

And when looking at the numbers above, membership fees are only responsible for about 2% of revenue. But in the first three quarters of 2023, membership fees were responsible for 75% of net income. I know this is a daring statement, but it is Costco’s business model that the company is generating most of its net income from membership fees and will profit only slightly from sales. Costco is passing on the low prices to the consumer and is basically selling most items at cost (of course, including all Costco expenses).

Other businesses might tolerate such strategies as they might be profitable for a business. Misusing membership cards could lure in new customers that will increase revenue and profits. But in case of Costco, it is only increasing revenue, but not the company’s profits. On the other hand, the damage for Costco is also limited as the company also won’t lose money: The expenses of the business should be covered by the generated revenue from sales (speculative statement).

Drawing Parallels: Netflix

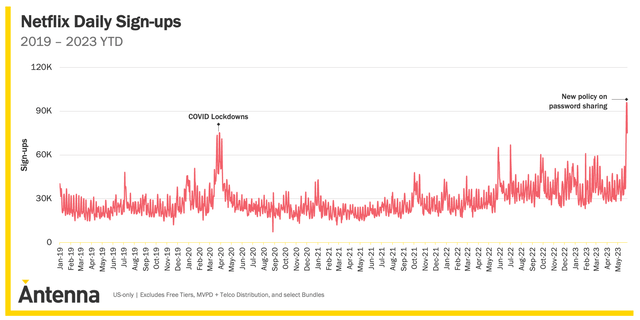

A parallel that comes to mind – and was often drawn in the last few days – was Costco becoming the new Netflix as the streaming giant also cracked down on accounts being used by too many people without paying. Netflix began to curb password sharing in the United States on May 23, 2023. And according to data from Antenna, Netflix saw nearly 100k users signing up daily on May 26 and May 27 – this is the highest number in the four and a half years that Antenna has been measuring this data (even higher as during the COVID-19 lockdowns).

Antenna

But we can not only look at a few days after Netflix actually prevented subscribers from sharing passwords. We can also look at the last few quarters – Netflix already talked in its Q3/22 shareholder letter (released in 2022) about the issue and since then the topic was all over the news. And in Q4/22 and Q1/23 the company could add more subscriptions again than expected and one of the reasons might have already been the announcement.

Drawing Parallels: Retail

Switching from Netflix to a competitor is not so easy. Netflix has a lot of content that is exclusive and if you want to watch Netflix original programming you must continue paying for Netflix. In case of Costco the situation is different – you can easily switch to a competitor as retailers usually don’t have high switching costs. Prices might be different, but the products are also available at another retailer.

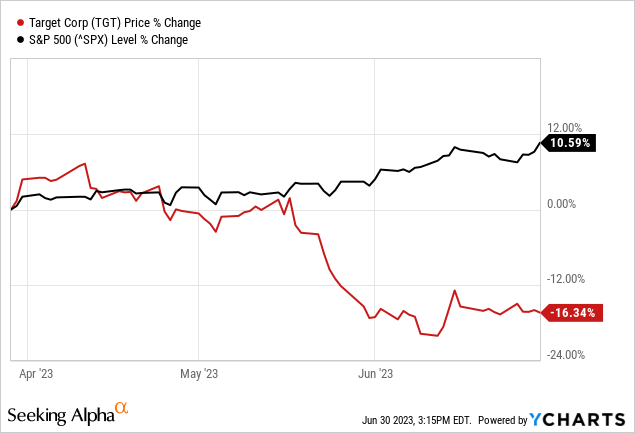

And here we can look at other retailers – and a recent example might be Target. The company has had a clear political opinion for decades and is not afraid to express its opinion. And for years, Target rolled out its Pride merchandise. However, this year, its workers were threatened and there were violent confrontations. As a result, Target removed items that were causing that outrage and the stock lost $10 billion in market capitalization.

But we should also be cautious about interpreting share price performance. Markets are extremely complex and while the boycott story seems like a solid explanation it is probably not true or not the only reason for the stock declining. So far, Target did not report any results to see if the boycott had a real impact on the business – the last reported numbers have been first quarter results for the quarter ending April 29, 2023.

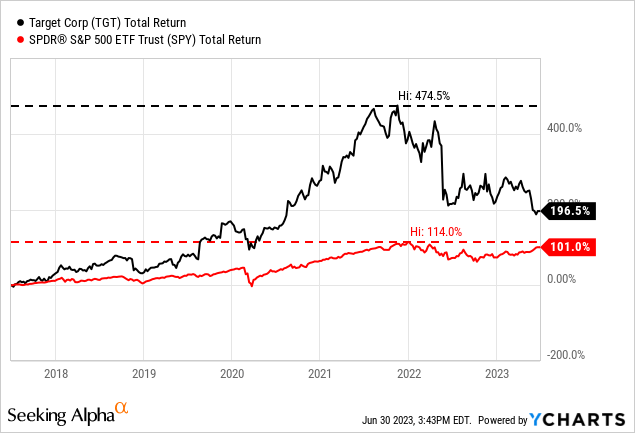

In my opinion, we should not pay much attention to such political issues. Do you remember the bathroom issue in 2016? Back then when Target’s stock declined as low as $50 and many were arguing this was due to the bathroom issue, we could read articles about Target being doom and a horrible investment. Well, we know what happened next.

Target extremely outperformed in the following years. And I think people should not have been blinded by this nonsense bathroom issue. I assume, sentiment among investors or consumers can have short-term impacts, but over the long run, we should not focus on the Pride collection or bathrooms, but rather how well a company is executing, how well management is performing and what economic moat a company has around its business.

And of course, I am also aware of the stories around Bud Light and while we don’t know what potential impacts on Target’s business might be, we know that Bud Light actually lost market share and its spot as top U.S. beer. We should therefore not underestimate the influence social media can have.

Impacts on Costco

After we have provided some context and saw Netflix probably profiting from its move but retailers like Target or brands like Budweiser being negatively affected by angry customers, we should look at potential consequences for Costco.

First, while Netflix can rather easily crack down on people using Netflix without paying for it, Costco will always need additional personnel to check IDs at the self-checkout and this is actually undermining the concept of self-checkouts a little bit. And it might lead to increasing expenses for Costco.

And I can see Costco’s move going in two different directions. I could see customers getting angry and annoyed by Costco and they might feel like they are constantly monitored by Costco. And as the switching costs are – in theory – rather low, customers might go to other retailers. On the other hand, I could also see these customers starting to pay for Costco membership as they want to continue shopping there.

When looking at the total paid members of Costco over time, we see more or less stable growth rates between 2014 and 2022.

|

Year |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|---|---|---|---|---|---|---|---|---|---|

|

Total Paid Members |

42.0 million |

44.6 million |

47.6 million |

49.4 million |

51.6 million |

53.9 million |

58.10 million |

61.7 million |

65.7 million |

|

YoY growth |

7.7% |

6.2% |

6.7% |

3.8% |

4.5% |

4.5% |

7.8% |

6.2% |

6.5% |

(Data from Annual Reports)

One assumption might be that growth rates are slowing down in the recent past as less customers were paying for the Costco membership and instead using the cards of friends. But according to the growth rates above, that seems not to be the case. We can only speculate what the reasons might be – the extreme inflation rates could lead to people searching for ways to shop cheaper. And when being on social media (Twitter for example) one might get a feeling that shoplifting and looting is exploding in the United States – and shopping without being a member might also fit this pattern. But it seems like data is not backing up that subjective point of view.

And so far, there is obviously no clear data how this might impact the business. We have only pieces of information, but they must be seen as anecdotal. There seem to be different opinions about customers understanding the move or pointing out that other retailers – like Sam’s Club – aren’t as strict. But reactions seem to be very different so far and I can’t identify a pattern so far. Some customers are also seeing Costco’s behavior as intrusive. When using Google Trends for example, I also can’t identify any patterns. The search volume for “Costco membership sharing” has exploded in the last two weeks and the search for “Costco membership” also increased during June and is about 50% higher than in previous months. But aside from an interest for the topic, it is hard to draw conclusions.

I can also imagine Costco raising the membership fee in the foreseeable future. When asked about raising the membership fee during the last earnings call, CFO Richard Galanti responded:

As it relates to membership fees, nice try, Michael, but at the end of the day with the headline being inflation, we feel very good about if we want to do it, we do it without impacting in any meaningful way renewal rates or sign-ups or anything. And at some point, we will, but our view right now is that we’ve got enough levers out there to drive business and we feel that it’s incumbent upon us to be that beacon of light to our members in terms of holding them for right now. It’s not a matter of a big time, but we’ll let you know as soon as we know.

And even when Costco won’t raise its membership fee right now, it would not be unreasonable to do so – the last hike was six years ago in 2017. Of course, Costco could raise membership fees as reaction to the damage done by customers shopping there by using a friend’s card. This is part of the “free rider problem” – those sticking to the rules often must pay for those that don’t to cover the costs (and the damage done by people who are shoplifting, ride the train without tickets and so on). I don’t think Costco will raise membership fees in 2023, but it might be a move in 2024.

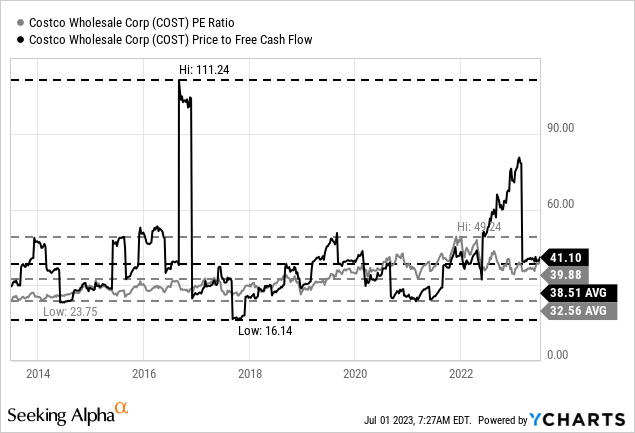

Intrinsic Value Calculation

In my last article – published in May 2023 – Costco was still too expensive. And although Costco reported quarterly results in the meantime, I don’t see much reason to update my intrinsic value calculation. And even if we assume that Costco might generate 5% to 10% more net income (and free cash flow) due to additional members from the “crackdown” in the coming quarters – and this seems like a very optimistic assumption – this is offset by the 8% higher stock price.

And Costco is still trading for 40 times earnings per share and 41 times free cash flow. There are clearly stocks trading for higher valuation multiples, but a stock trading for 40 times earnings and free cash flow is certainly not cheap.

Conclusion

It is interesting that Costco is trying to stop customers from misusing cards. And this might have an impact on the membership fees in the coming quarters as some of the customers shopping there right now by using the card of friends might still want to shop at Costco and might be willing to pay $60 annually. It seemed to have worked for Netflix and could also work for Costco. On the other hand, customers could also be outraged, and a company could face backlashes – like Target or Budweiser.

But no matter how the story will play out, it doesn’t change my assessment of Costco. The stock is overvalued at this point and even with increased net income due to additional memberships I still don’t see Costco stock as a “Buy”.

Read the full article here