Investment Thesis

Coursera, Inc. (NYSE:COUR) has good growth prospects ahead. The company’s revenue growth should benefit from strong demand for professional certifications driven by the rising need for reskilling and upskilling. This demand should further be supported by increasing certifications by renowned industry partners, which should continue to boost new learner registration and help revenue growth. Additionally, strength in the government and campus businesses, traction towards online degree courses, and implementation of AI tools and technologies to scale the offering and improve user experience should also support revenue growth.

On the margin front, the company should benefit from operating leverage and cost-saving initiatives. Further, the company is also trading at a discount to its peer Udemy (UDMY) as well as the sector median. It also has a healthy balance sheet, which should help it overcome any temporary near-term headwinds. This along with a positive growth outlook provides a good contrarian buying opportunity. Hence, I have a buy rating on the stock.

Coursera’s Revenue Analysis and Outlook

In my previous article in August last year, I discussed the company’s good growth prospects benefiting from good demand for entry-level courses. While the company has posted good growth since then, the stock price has corrected meaningfully as investor sentiment around the Edtech sector have soured and the company continues to see temporary weakness among its enterprise customers as corporate clients have reduced their training budgets due to the tough macroeconomic environment.

In the first quarter of fiscal 2024, the company’s revenue growth continued to benefit from healthy demand for entry-level professional certificates, good new learner registrations, high net customer retention rate, and growth of new degree students. This helped the company more than offset lower volume in North America due to delays in content launch by key educational partners within the consumer segment. The company posted 14.6% Y/Y growth and its revenues increased to $169 million.

On a segment basis, the Consumer segment revenue grew by 17.9% Y/Y. However, this growth came in lower than expected as good demand for entry-level professional certificates and AI content was partially offset by a temporary volume slowdown in North America due to a delay in content launch by key educational partners. In the Enterprise segment revenue grew by 10.2% Y/Y driven by strong demand within the government and campus verticals which more than offset the demand slowdown from corporate enterprise customers. Lastly, the Degree segment posted revenue growth of 10.4% Y/Y driven by a 23% Y/Y increase in new students globally and good scaling of recent program launches.

COUR’s Historical Revenue (Company Data, GS Analytics Research)

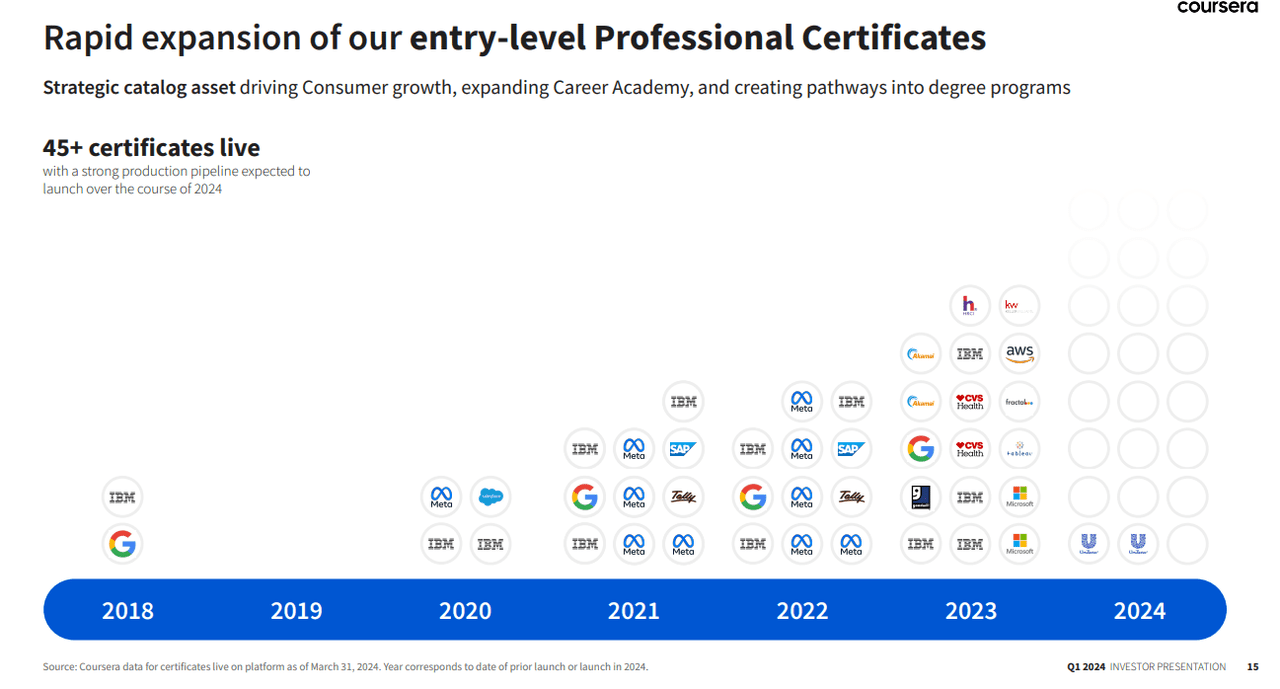

Looking forward, the company’s revenue growth prospects look positive. Before the pandemic, Coursera had content from top-notch universities. However, one area where it lagged was content from industry. This is fast changing and the number of professional certifications available on the website from industry leaders like Microsoft (MSFT), Meta (META), and Alphabet (GOOG) have been rapidly rising. The job-relevant certifications in high-demand fields such as AI, data science, cloud computing, and cyber security provide a valuable resource for both individuals as well as employers as the need for upskilling and reskilling continues to rise. I believe a continued increase in the number of such certificates available on Coursera’s platform as well as strong demand for them from both employers/individuals should be a good driver for the company’s sales moving forward.

Entr-level professional certificates on Coursera platform (COUR’s Q1 2024 Earnings Call Presentation Slide)

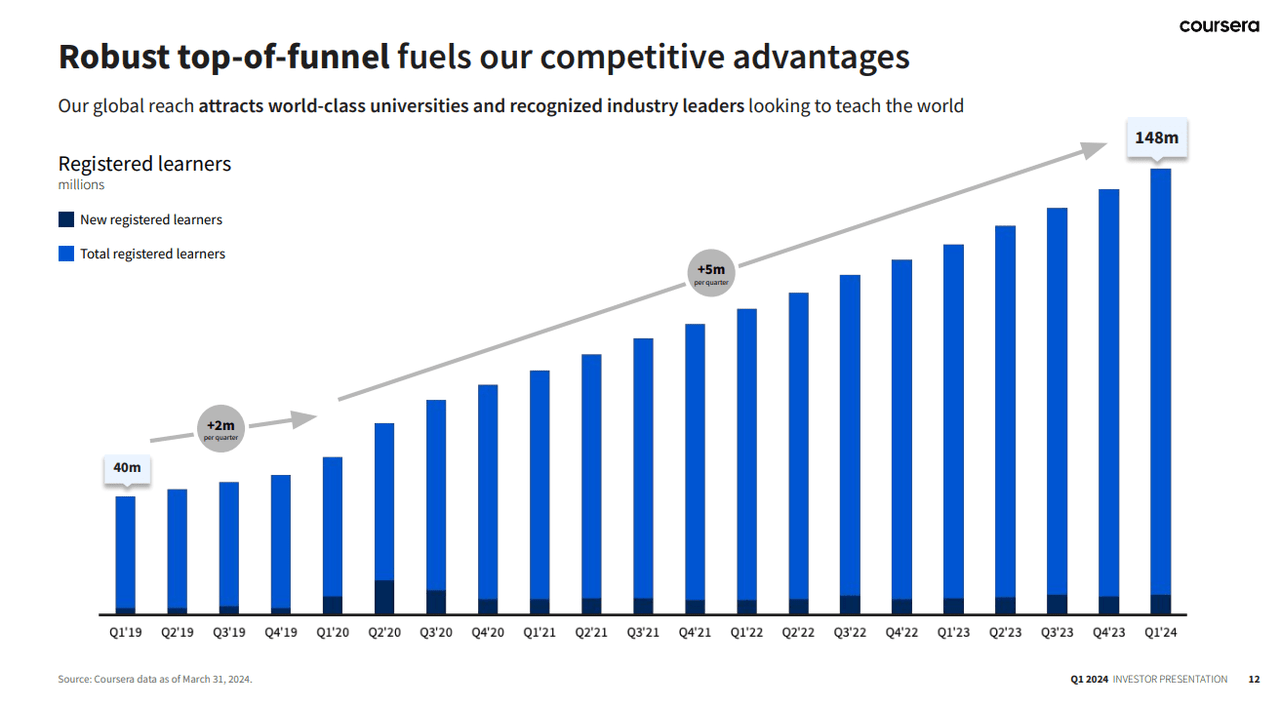

The company is also seeing strong top-of-funnel activities and the number of registered learners on the platform continues to grow. Ideally, I would have liked a better conversion of their registered users into paid subscribers. I believe over time, as recognition of online certificates and courses continues to rise, this will happen and monetization should pick up. For now, I am happy with the increasing user base as it illustrates the utility of the company’s offering and bodes well for future revenue growth.

Coursera’s registered users (COUR’s Q1 2024 Earnings Call Presentation Slide)

In the enterprise segment, while the company is seeing some pressure from business customers as corporate learning budgets are under pressure due to the tough macroeconomic environment, the government and educational institutional clients continue to see good traction. I believe the integration of Coursera’s content into the university curriculum should continue to benefit Coursera’s sales in the coming years. Also, the headwinds among corporate customers aren’t something that should continue forever. In the coming years, as the macroeconomic environment improves, I believe this market should see a recovery.

The company’s degree segment also has good growth prospects. In fact, this segment has the largest total addressable market (TAM) for the company. The company’s pathway degree programs, which allow learners to start with affordable courses that count for a degree continue to get good traction as they make higher education more accessible and affordable. As the company continues to increase its university partnerships and online degrees continue to get more acceptability, I believe this segment can continue to see good growth.

The company is also doing a good job in terms of using generative AI and other technological advances to improve the quality and efficiency of launching and delivering courses. The company has introduced tools like Coursera Coach, and AI-assisted course builders. It is also using AI-powered translations to offer courses in multiple languages, which should help it gain traction with a global audience. I believe these initiatives will greatly enhance the company’s scalability in the coming years.

Overall, I remain optimistic about the company’s growth prospects.

Coursera’s Margin Analysis and Outlook

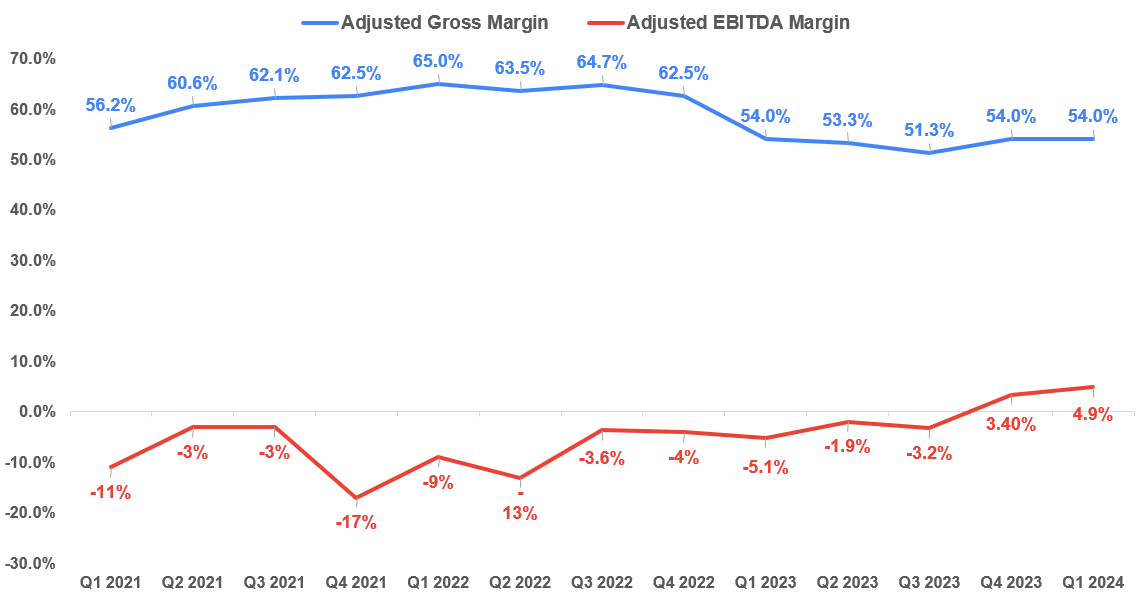

In the first quarter of fiscal 2024, the company reported a flattish adjusted gross margin of 54%. However, the adjusted EBITDA margin improved by 1000 bps to 4.9% as it benefitted from volume leverage and cost-saving initiatives which resulted in lower operating expenses as a percentage of sales compared to the previous year’s quarter.

COUR’s Historical Adjusted Gross Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking forward, I am optimistic about the company’s margin growth prospects. Coursera’s business model has a good amount of inherent leverage. With higher enrollment, the fixed cost of developing content gets spread over a larger revenue base. So, the company should see good operating leverage with an increase in revenue. Further, the company is doing a good job in terms of using AI to reduce costs. For example, the company is now using AI to translate and localize content, which is much more cost-effective compared to human translators.

I believe automating some of the content creation-related activities as well as other routine work should help the company’s margins in the coming years.

Valuation and Conclusion

Coursera is currently trading at 34.18x FY24 consensus EPS estimate of $0.19 and 23.64x FY25 consensus EPS estimate of $0.28.

Coursera’s Consensus EPS estimates, EPS Growth and Forward P/E (Seeking Alpha)

Of late, the Edtech sector has fallen out of favor among investors. A good example of it is the Indian Edtech company Byju’s which was getting ~$22 billion valuation in private markets and is now seeing its equity marked down to zero by some investors. If we look back home among U.S listed companies, Chegg (CHGG) has seen its stock price decimated to low single digits compared to $100 plus in early 2021. However, unlike Chegg, which is seeing declining revenues, Coursera’s revenue is expected to see good growth and registered users on the platform are also increasing.

While the company has seen some headwinds and its revenues have come in lower than expected in the recent quarter due to delayed launches of some courses and continued weakness in the corporate enterprise learning markets, I don’t believe it is fair to lump it with the failing Edtech startups. The company has a healthy balance sheet with over $720 mn in net cash as of the last quarter end, which should easily help it overcome any temporary weakness in the end markets. The company’s EV/Sales is now just 0.47x, which is much lower than its peer Udemy’s 1.11x EV/Sales and the sector median EV/Sales of 1.24x.

I believe a strong balance sheet, good long-term growth prospects, and reasonable valuations make Coursera a good buy, and contrarian investors who can look beyond the near-term headwinds and muted sentiment can consider buying the stock at the current levels. Hence, I rate the stock a buy.

Risks

-

Edtech is a highly competitive industry with several players aiming for market share gains. While Coursera’s size and early mover advantage should help the company, the competition remains intense.

-

While the company has made good use of AI so far, AI also presents a risk/competitive threat. Some learners have already started using AI platforms like ChatGPT to enhance their knowledge of particular topics and companies like Chegg have seen a significant negative impact. I don’t see an immediate risk to Coursera given the difference in its content offering compared to Chegg. However, AI is an evolving field and it may pose some risk in the future.

Read the full article here