CrowdStrike Stock’s Continued Rally

The continued outperformance from CrowdStrike Holdings (NASDAQ:CRWD) stock has been nothing short of spectacular. CrowdStrike has been leading the platformization drive in the relatively fragmented cybersecurity industry, underpinned by its “single lightweight-agent architecture.” As a result, it has been instrumental in CrowdStrike’s go-to-market strategy, broadening its land-and-expand momentum. CrowdStrike underscores the “simplicity and effectiveness” of its cloud-native approach, demonstrating the value of adopting “one centralized platform” for CrowdStrike’s customer needs. CrowdStrike has been doing this since its inception, which is attributed to CRWD’s commitment to developing and integrating security modules through its platform strategy.

I indicated my caution on CRWD stock (Hold rating) in my previous article in early March 2024. While I have been impressed with CrowdStrike’s execution and remarkable growth cadence, I was concerned with its highly expensive valuation. Notwithstanding my caution, CRWD has continued to outperform the S&P 500 (SP500) since then, underscoring the resilience of CRWD’s buying sentiment.

CrowdStrike’s fiscal first-quarter (FY2025) earnings release will be posted on June 4. I have assessed that investors are heading into its upcoming earnings report with palpable optimism, as CRWD rallied close to its March 2024 highs at the $365 level. In other words, investors are likely betting that CrowdStrike is expected to report another solid earnings scorecard, justifying its recent surge.

Analysts Optimistic About CrowdStrike’s Q1 Earnings

CRWD quarterly revenue estimates (Seeking Alpha)

Wall Street expects CrowdStrike to report revenue of $904.8M in FQ1. It’s closer to the higher end of CrowdStrike’s revenue guidance range. As a result, CrowdStrike is expected to post revenue growth of more than 30% for its fiscal first quarter, a highly remarkable growth momentum.

CrowdStrike annualized revenue estimates (Seeking Alpha)

In addition, analysts project full-year revenue growth of more than 30% for FY2025, reaching $3.98B. It’s also closer to the higher end of CrowdStrike’s outlook, suggesting less room for execution errors or mishaps. Wall Street analysts have also drummed up market sentiment for CRWD as we approach its earnings release. Morgan Stanley (MS) analysts are confident that CRWD could “exceed a $100 billion valuation within the next 12 months.”

I don’t doubt CrowdStrike’s execution capabilities. If anything, Palo Alto Networks’s (PANW) platformization push has validated CrowdStrike’s value proposition. Despite that, the relatively fragmented nature of the cybersecurity industry suggests the market is still rapidly evolving, implying relatively high execution risks.

Furthermore, Palo Alto Networks has made progress with its strategy, as indicated in PANW’s recent earnings release. Therefore, more intense competitive risks shouldn’t be ruled out, as CrowdStrike’s leading competitors undertake a more aggressive approach to potentially underprice against its premium offerings.

Given its leadership position in endpoint security, CrowdStrike isn’t expected to see its platform strategy weaken in the near term. However, CRWD’s surging optimism has reduced CrowdStrike’s margin for error. Consequently, weaker-than-anticipated execution could lead to significant pain for investors.

CRWD Stock Valuation Is Highly Expensive

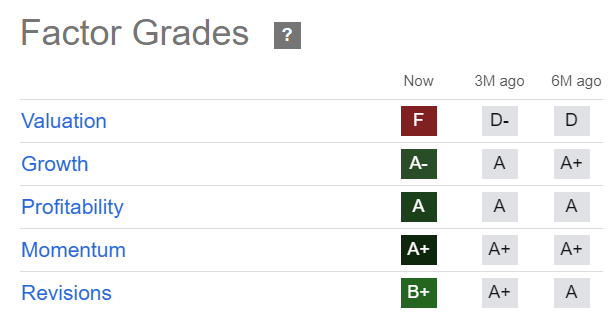

CRWD Quant Grades (Seeking Alpha)

With CRWD garnering three “A” range grades from Seeking Alpha’s Quant, it seems foolish to be bearish on CRWD. CRWD’s solid “B+” earnings revisions grade underscores CrowdStrike’s impressive execution, leading to upgraded earnings estimates.

However, CRWD’s “F” valuation grade shouldn’t be ignored. CRWD’s forward adjusted P/E of 89x is way above its tech sector median of 23.7x. Furthermore, CRWD’s forward adjusted PEG ratio of 2.2 corroborates my observation that the market’s optimism on continued rapid share gains has likely been priced into its valuation. In other words, unless you have a firm conviction that CrowdStrike management can deliver another solid beat-and-raise in its upcoming report, even a slight disappointment could lead to a potential valuation de-rating.

Is CRWD Stock A Buy, Sell, Or Hold?

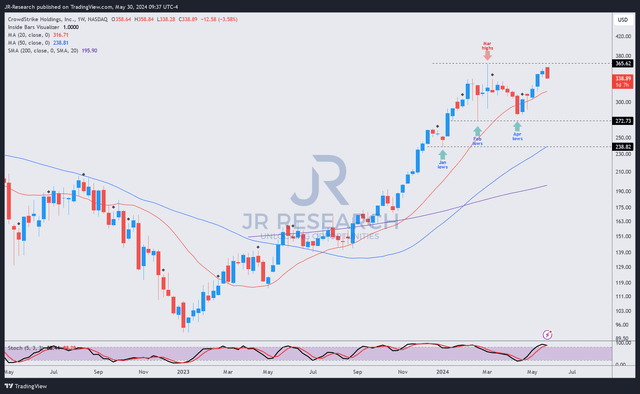

CRWD price chart (weekly, medium-term) (TradingView)

CRWD’s price chart corroborates its bullish bias, suggesting there’s no need to cut exposure significantly yet to protect earlier gains. However, CRWD’s buying momentum seems likely to fail again below the $365 level, which preceded significant downward volatility in March 2024.

As a result, investors must brace for further impact, as buyers don’t seem ready to lift CRWD stock higher from here, necessitating caution. Dip-buyers looking to add exposure at a potential pullback should find possible opportunities above the $270 levels or $240 levels (bear market decline). Given CRWD’s highly expensive valuation, we shouldn’t understate the possibility of reaching these levels if CrowdStrike management disappoints on its forward guidance.

Rating: Maintain Hold.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here