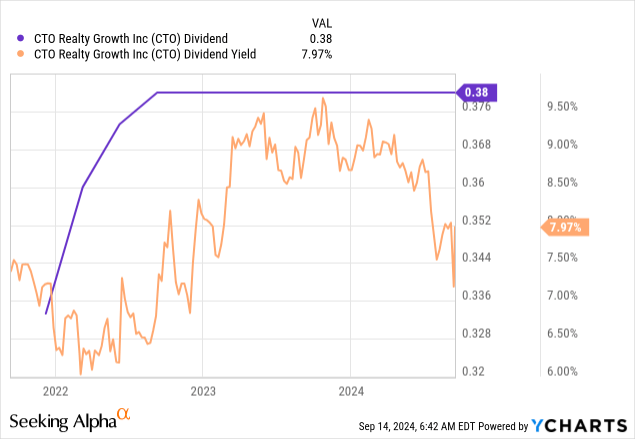

CTO Realty Growth (NYSE:CTO) has been a quiet juggernaut in the retail REIT space, up 18% on a total return basis year-to-date and last declaring a quarterly cash dividend of $0.38 per share, unchanged from the prior period and $1.52 per share for an 8% annualized dividend yield. I last covered the REIT in May, when there was still material uncertainty around when the Fed would start paring back interest rates. Market confidence around the start of rate cuts has now coalesced around the September 18th FOMC meeting, with the CME FedWatch tool also placing the probability of a 50 basis points cut at a material 50%. This is as slowed US consumer spending, rising unemployment, and low gas prices have set the conditions for the first rate cut in four years.

This bodes well for REITs with CTO set to benefit materially from this with a total debt balance of $484 million as of its last reported fiscal 2024 second quarter. This drove a monthly interest expense of $5.6 million, up $400,000 from CTO’s year-ago comp. The REIT reported second-quarter revenue of $28.85 million, up 10.8% year-over-year and beating consensus by $1.44 million. Critically, funds from operation during the quarter at $0.45 per share beat consensus estimates and was up by 2 cents from CTO’s year-ago comp of $0.43 per share. I own a significant number of CTO’s common shares, with the near 8% dividend yield on these rendered safe by a second-quarter 118% FFO coverage ratio.

Retail Property Portfolio And FFO

CTO Fiscal 2024 Second Quarter Supplemental Reporting Information

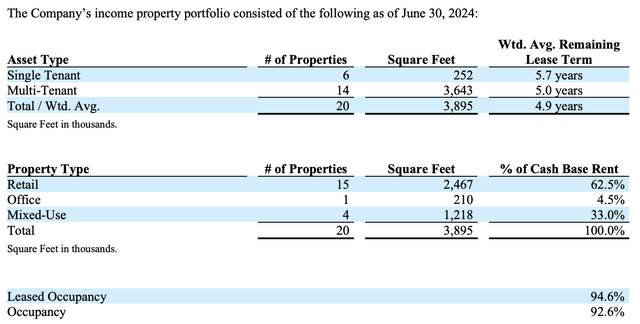

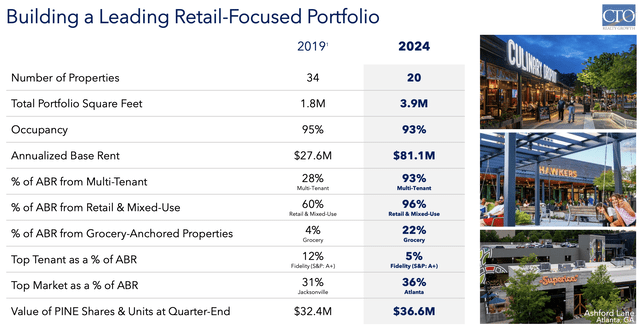

CTO’s portfolio consisted of 20 properties spread across 3.9 million square feet with an $81.1 million annualized base rent as of the end of the second quarter. Around 94% of CTO’s square feet is derived from multi-tenant properties, with the REIT’s weighted average remaining lease term at 4.9 years. Occupancy, at 92.6% at the end of the second quarter, was up from 91.4% a year ago. CTO is very active on the acquisitions and dispositions front, with the REIT recently announcing the acquisition of three open-air shopping centers in Florida and North Carolina for $137.5 million. The REIT has closed $230 million of acquisitions and $38 million of disposals year-to-date.

CTO July 2024 Investor Presentation

The REIT also has a growing structured investments business, mainly built around originating commercial loans for existing relationships. This saw a $10 million construction loan originated at a fixed interest rate of 11% for seven outparcel locations in Lake Worth, Florida. The loan is interest only ahead of its maturity on September 26, 2025. While riskier, it is a small part of CTO’s operations and commercial first mortgage loans have a senior position in the underlying collateral.

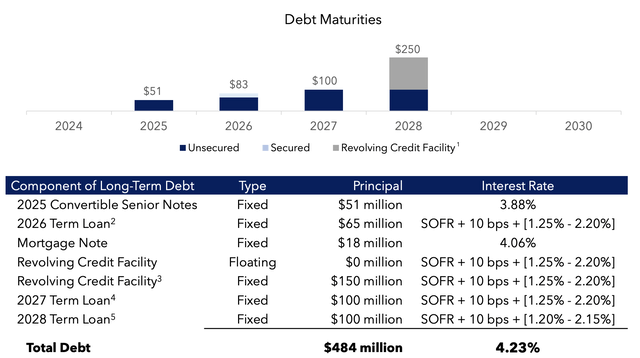

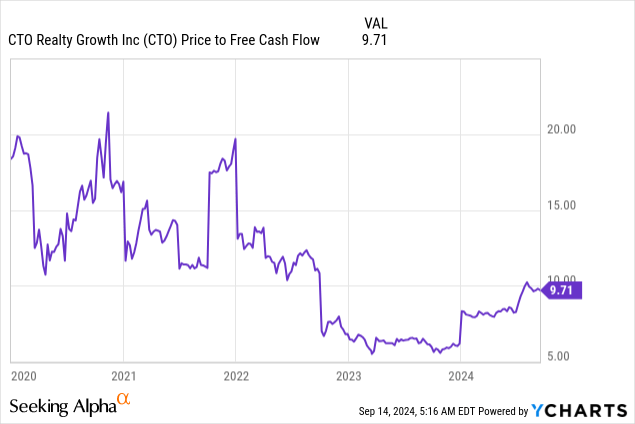

Debt Maturities, Leasing Spreads, And Valuation Multiple

CTO signed 16 leases spread across 78,593 square feet during the second quarter. On a comparable basis, the company signed 11 leases totaling 57,878 square feet at an average cash base rent of $23.34 per square foot, a positive spread of 8.8% versus its year-ago comp of $21.45 per square foot. Positive leasing spreads highlight the value proposition of the REIT’s portfolio and are set against no debt maturities for the rest of 2024. CTO faces a $51 million unsecured debt maturity next year and a further $83 million of debt maturing in 2026.

CTO July 2024 Investor Presentation

The REIT held cash and cash equivalents of $4.8 million at the end of the quarter, down from $10.2 million at the start of the year but with liquidity at $155 million. CTO tapped its preferreds (NYSE:CTO.PR.A) for liquidity during the quarter with the public offering of 1,700,000 additional shares in the Series A in April for net proceeds of $33.1 million. The REIT also has an at-the-market program which saw the sale of 250,000 common shares for net proceeds of $4.3 million comes as the 200 basis points spread between leased occupancy and physical occupancy of 94.6% is set to drive nearly $5 million of future cash rents, expected to be realized through 2025 as new tenants take possession.

CTO currently trades at 9.71x its free cash flow, up from its near-term lows but still below its historical line of best fit in the mid-teens. This implies continued capital growth with the commons as the Fed embarks on the long-awaited step to bring down interest rates, currently at a 23-year high. Bears would be right to highlight that a sudden re-acceleration of inflation would derail market exuberance over the intensity and pace of rate cuts and send the commons back down. This risk is poignant for most REITs, but the 8% dividend yield and strong coverage remain reasons to go long the commons.

Read the full article here