A semi truck driving down a highway.

One of the beauties of capitalism is that there are thousands of publicly traded businesses in the U.S. Even filtering for quality, there may be hundreds of exceptional dividend growth stocks, with at least a handful of them being attractive buys at any given time.

This is why I believe that patience and not forcing one’s hand as an investor is so important. I have found that waiting for the opportune time to buy a great business generally produces much better results than the FOMO of rushing a purchase.

Accounting for 1% of my portfolio, Cummins (NYSE:CMI) is a dividend growth stock that I’m glad to own. When I last covered it in April, I liked the company’s earnings growth trajectory, its A-rated balance sheet, and consistent dividend growth.

However, I thought the share price had gotten too far ahead of itself. Coupled with the aforementioned principle that guides my investment strategy, that is why I downgraded it to a hold at that time.

As the markets have proven time and again, though, time and patience are all that is needed for a hold rating to go back to a buy rating. Shares of Cummins have shed 12% of their value, which I believe has swung the valuation from a premium to a slight discount.

Last month, the industrial shared its first-quarter financial results. Along with both recent and upcoming product launches, this supports underlying assumptions of healthy growth in the years to come. The company’s net debt-to-capital ratio also strengthened over the year-ago period.

Thus, I am upgrading the shares of Cummins back to a buy.

Navigating A Challenging Macroenvironment

Cummins Q1 2024 Earnings Presentation

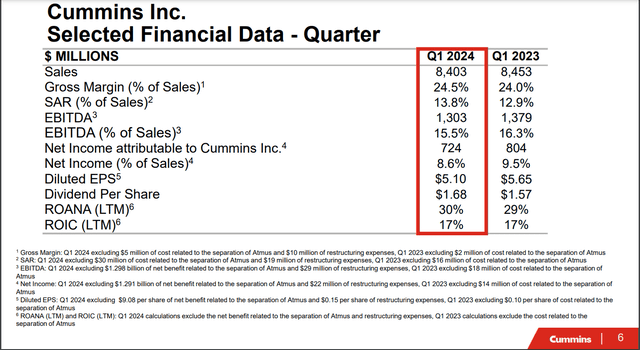

On May 2, Cummins released its financial results for the first quarter that ended March 31. The company’s sales decreased by 0.6% year-over-year to $8.4 billion during the quarter. For context, that was $50 million shy of Seeking Alpha’s analyst consensus.

At first glance, these results may seem lackluster or ho-hum. After all, essentially flat revenue doesn’t exactly evoke warm and fuzzy feelings as an investor. Overall, I would argue that the results were just fine, though.

Cummins displayed strength in its Distribution and Power Systems segments in the first quarter.

The Distribution segment’s sales grew by 5.4% over the year-ago period to $2.5 billion for the quarter. As CFO Mark Smith pointed out in his remarks during the Q1 2024 Earnings Call, distribution is more than half parts and services. This makes its sales quite reliable, which explains how the segment grew the topline during the quarter.

Cummins’ Power Systems segment posted $1.4 billion in sales in the first quarter, which was a 3.4% year-over-year growth rate. Per Smith, higher volumes and improved pricing led by power generation markets were growth catalysts for the segment.

Weakness in the Components and Engines segments weighed on otherwise respectable results for the first quarter.

Components segment sales declined by 6.3% over the year-ago period to $3.3 billion during the first quarter. On page 29 of 55 of Cummins’ Q1 2024 10-Q Filing, the company cited lower demand in heavy-duty truck markets as a headwind to the segment’s results. The completed separation of Atmus (ATMU) from Cummins also played a role in the segment’s topline drop.

Engines segment sales decreased by 1.9% year-over-year to $2.9 billion in the first quarter. That was the result of the macroeconomic environment causing weaker demand for construction engines.

Shifting gears to the bottom line, Cummins’ non-GAAP diluted EPS waned by 8.1% over the year-ago period to $5.10 for the first quarter. On the plus side, this was $0.14 better than the Seeking Alpha analyst consensus.

Due to investment in new products and lower sales volumes, EBITDA margin contracted by 80 basis points to 15.5% during the first quarter. This is why non-GAAP diluted EPS fell at a faster rate than sales in the quarter.

Cummins Analyst Day 2024 Presentation

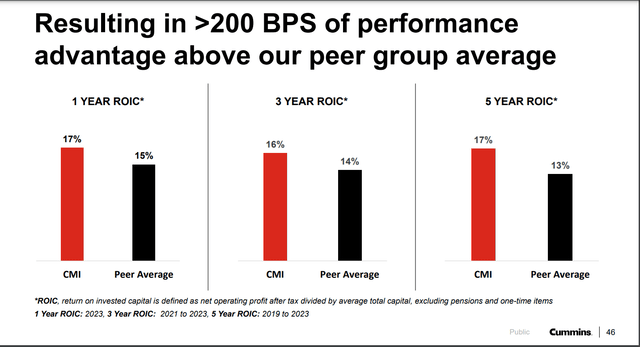

I’m also rather confident that the investments being made by Cummins today will pay off in the future. This is because the company has a proven track record of being a prudent allocator of shareholder capital.

In the past five years, Cummins has regularly generated mid-to-upper teen returns on invested capital. This is notably better than the peer average in the low-to-mid teens.

In February, Cummins added two new generator sets to the award-winning Centum Series. The power ranges of between 1750 and 2000 kW offer customers a more complete selection of products to meet their needs. The appeal to these two generator sets is that they are designed with both performance and reduced emissions in mind.

In April, Cummins launched another two models of generator sets. These have power outputs of 2750 and 3000 kW. That makes them ideal for applications like data centers and waste-water treatment plants.

These recent launches are just two of the latest examples of how the company is investing in designing, launching, and selling products of the future.

Cummins Analyst Day 2024 Presentation

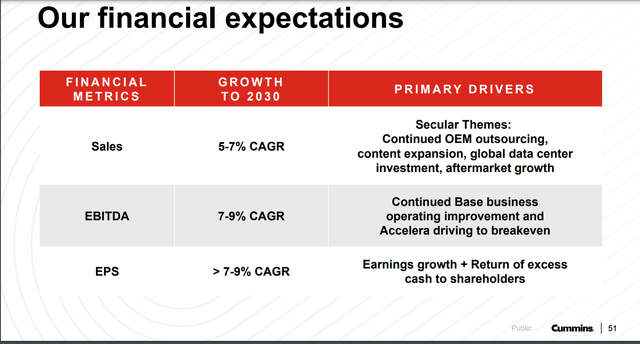

The near-term economic environment will likely continue to weigh on earnings throughout 2024. This is why analysts anticipate that non-GAAP diluted EPS will contract by 5.3% to $18.65 in 2024.

These ebbs and flows look to be baked into Cummins’ guidance of 5% to 7% compound annual growth rates for sales through 2030. Growth in aftermarkets, continued original equipment manufacturing outsourcing, and additional data center investments are all long-term trends working in Cummins’ favor.

As Accelera’s sales eventually ramp up to the EBITDA breakeven point in 2027 and the base business improves margins, this should drive incremental EBITDA margin expansion. That is driving Cummins’ expectation of an improvement in EBITDA margin from 14.9% in 2023 to a midpoint of 17.5% in 2030 (17% to 18%).

Marginal share buybacks also should push the company’s annual non-GAAP diluted EPS growth into the high single digits.

Like myself, analysts appear to have confidence in Cummins’ plans to deliver on these growth promises. The FAST Graphs analyst consensus is for non-GAAP diluted EPS to surge 14.5% higher in 2025 to $21.35 and another 14.1% higher in 2026 to $24.35.

This is based on the expectation that as time goes on, comps will be easier moving out of 2024 and recent product launches can return the company to growth.

A discussion of Cummins also wouldn’t be complete without highlighting the vigorous nature of its balance sheet. The company shored up its already strong balance sheet in the first quarter. Cummins’ net debt-to-capital ratio strengthened from 28.9% in Q1 2023 to 22.3% in Q1 2024. For more perspective, rating agencies like to see this metric below 50% per The Dividend Kings’ Zen Research Terminal.

So, Cummins is operating with quite a bit of room to spare financially. That explains how the company has an A credit rating from S&P on a stable outlook (unless otherwise sourced or hyperlinked, all details in this subhead were according to Cummins’ Q1 2024 Earnings Press Release, Cummins’ Q1 2024 Earnings Presentation, Cummins’ Q1 2024 10-Q Filing, and Cummins’ Analyst Day 2024 Presentation).

Fair Value Has Surpassed $290 A Share

FAST Graphs, FactSet

Recent weakness in industrials looks to have negatively impacted sentiment toward Cummins. In my view, this looks to have created the beginning of what I believe could be a buying opportunity in the coming months.

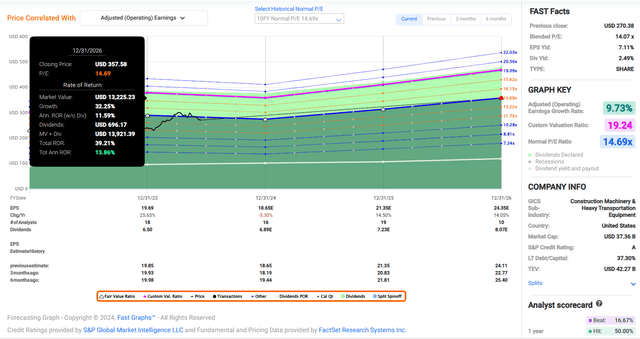

Cummins’ current-year P/E ratio of 14.1 is a bit below the 10-year normal P/E ratio of 14.7 per FAST Graphs. An examination of growth prospects shows that the company’s fundamentals are intact.

The ~10% annual earnings growth consensus for the next three years is just above the 10-year average annual earnings growth rate of 9% according to FAST Graphs. That’s what is underpinning my belief that a valuation multiple of 14.7 remains a reasonable estimate for fair value moving forward.

The calendar year 2024 will be 46% finished after this week. So, that leaves 54% of 2024 and another 46% of 2025 ahead in the coming 12 months. This is guiding how I’m weighing the earnings inputs that I discussed in the previous section of the article. That gives me a forward 12-month non-GAAP diluted EPS input of $19.90.

Plugging that in with the earnings multiple of 14.7, I arrive at a fair value of $292 a share. Compared to the current $263 share price (as of June 14, 2024), this is a 10% discount to fair value. If Cummins returns to fair value and posts growth in line with expectations, it could produce 39% cumulative total returns by the end of 2026.

The Next Dividend Raise Is Around The Corner

Cummins’ 2.5% forward dividend yield registers at nearly twice the 1.4% forward yield of the industrials sector. This generous starting income is enough to earn a B+ grade from Seeking Alpha’s Quant System for forward dividend yield.

The positives don’t end there, either. Cummins’ 18 consecutive years of dividend growth are well above the industrials sector median of 2.3 years. This is why the Quant System awards an A grade for consecutive years of dividend growth.

As if that wasn’t enough, Cummins also isn’t handing out token dividend raises to keep its streak alive. The five-year annual dividend growth rate is 8.1%, which is better than the sector median of 6.8%. That’s adequate for a B- grade for the five-year dividend growth rate from the Quant System.

Finally, dividend growth moving forward should remain in the high-single-digits annually. That is because assuming a 7.1% raise in the quarterly dividend per share to $1.80 in July, Cummins would pay $6.96 in dividends per share in 2024. Against the $18.65 non-GAAP diluted EPS consensus, this would be a 37.3% payout ratio. That’s below the 40% payout ratio that rating agencies prefer from the industry per the Zen Research Terminal.

Risks To Consider

Cummins should be set up to continue growing in the years ahead. Yet, it isn’t without its pertinent risks.

One risk to Cummins is that as of December 31, nearly 30% of its 75,000+ employees were represented by various unions. The collective bargaining agreements with these unions expire between 2024 and 2028.

If Cummins can’t reach a resolution with these employees before their contracts expire, its operations could be disrupted. Even if it reaches an agreement with employees, unfavorable agreements could pressure profit margins.

On a similar note, many of the company’s customers and suppliers have unionized workforces. So, the problems of customers and suppliers could become the problems of Cummins if they run into work stoppages/strikes.

As a global business, the industrial also faces geopolitical risk. Any trade disputes between major global economies could negatively impact the company’s financial results.

Summary: Cummins Is Back In The Buy Zone

Cummins’ fundamentals look to be fine for the circumstances. As it faces easier comps and innovation starts to bear fruit, growth should pick back up. In the meantime, Cummins possesses an A-rated balance sheet. Shares are also back around my $260 buy target, so that’s why I’m upgrading them back to a buy rating for now.

Read the full article here