One of the more interesting financial institutions that I have come across recently is a company called Customers Bancorp (NYSE:CUBI). Even those shares of the business plunged initially during the banking crisis that occurred earlier this year, the stock quickly recovered and the firm actually stands as the only bank that I have analyzed that has posted not only a full recovery from that downturn, but that is now trading at a premium to where the stock was on February 28. In some respects, this does strike me as a bit peculiar. But that is largely because of the bank has seen a decrease in its profitability this year. But when you dig deep into the most important data and see exactly how cheap the stock is, I can understand why a tremendous amount of optimism has built up around it.

A great prospect to consider

With a market capitalization of just under $1.10 billion, Customers Bancorp is a fairly small financial institution. Through its physical presence in key states like Pennsylvania, Massachusetts, Illinois, Texas, New Jersey, New York, Florida, New Hampshire, Rhode Island, and North Carolina, and more, Customers Bancorp provides customers with a wide variety of banking services. For instance, it offers up primary loans and deposit services for both consumers and commercial customers. The loans that it gives out come in all sorts of flavors, with examples being real estate loans, multifamily loans, residential mortgage loans, and commercial and industrial loans.

The firm claims that its specialty involves providing fund financing services, as well as financing centered on real estate, technology and venture opportunities, healthcare facilities, and financial institutions. It even provides small business funding through the SBA programs that exist. Operationally speaking, the company describes itself as a firm that’s dedicated to differentiating itself through the use of technology that works in conjunction with its ‘single point of contact’ business strategy.

Author – SEC EDGAR Data

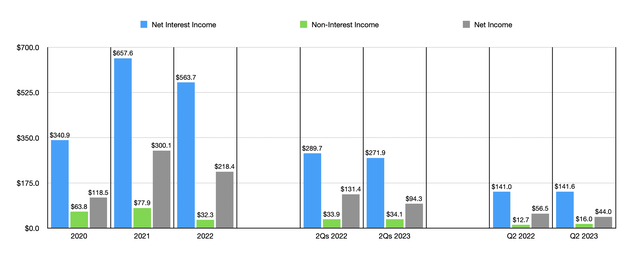

Over the past few years, the general trajectory for the company from a financial perspective has been positive. But it has also been lumpy. For instance, from 2020 to 2022, net interest income did rise, jumping from $340.9 million to $563.7 million. However, the 2021 fiscal year was actually the highest grossing for the company when it comes to this particular metric. As the chart above illustrates, non-interest income has actually decreased, and net income, while higher than it was in 2020, is lower than it was in 2021. Overall financial performance has remained mixed so far this year. As the chart above illustrates, net interest income is down for the first half of 2023 compared to the same time last year. The same is true of net profits. But the former of these two metrics actually showed some improvement when it comes to the second quarter on its own.

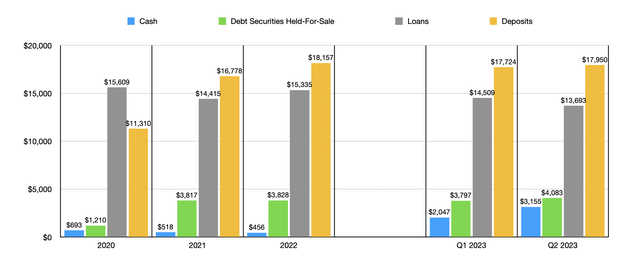

Personally, I do place a lot of value on consistent growth for a company. The absence of this does knock a few points off of my assessment for the firm. But I would also argue that there are more important metrics to be paying attention to. For instance, the most important in my mind would be the total deposits of the institution. These jumped from $11.31 billion in 2020 to $18.16 billion in 2022. We did, unfortunately, see some decline in the first quarter of the year. That brought deposits down to $17.72 billion for a sequential decline of $433.4 million. But given the tremendous amount of uncertainty in the banking sector at that time, this is not all that surprising. What’s even better is that we have seen the picture show some recovery subsequent to the end of the first quarter. By the end of the second quarter, for instance, the company had added $226.8 million to its deposit base, taking it up to $17.95 billion.

Author – SEC EDGAR Data

In looking at the banks that are out there, one thing that I have placed a high priority on is finding institutions that have relatively little uninsured deposit exposure. I typically define this as being 30% or less of all deposits. At the end of 2022, Customers Bancorp had $6.4 billion of its deposits that were classified as uninsured. By the end of the first quarter, this number had declined to $3.9 billion, or about 22% of total deposits. That number has crept up some to $4.4 billion as of the end of the second quarter, but that still works out to only 24.5% of deposits.

The picture regarding the company’s loan portfolio has been less clear. From 2020 through 2022, the company has seen some volatility in the value of loans. But they have really stayed within a fairly narrow range. At the same time, however, the company grew the value of its investment securities from $1.21 billion to $3.82 billion. This year, the business has seen a significant decline in the value of loans, dropping from $15.34 billion at the end of last year to $13.69 billion by the end of the second quarter. But this was driven in part by a surge in cash from $455.8 million to $3.16 billion and an increase in investment securities to $4.08 billion.

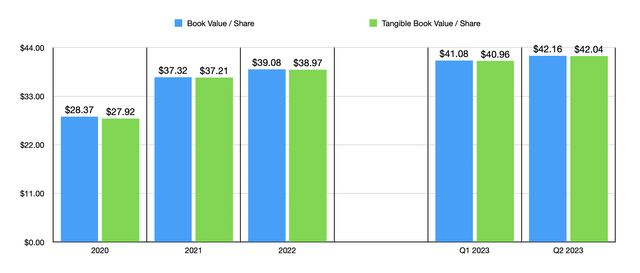

To cut through all of the changes here, I would argue that it’s actually best to just look at the company’s book value per share over time. That number grew from $28.37 to $39.08 in the three years ending in 2022. Today, it’s up to $42.16. The firm’s tangible book value per share increased at a similar rate. Of course, not all loans are the same. For instance, we know that the market is very worried right now regarding office exposure. And that is because of high vacancy rates in office properties across the nation. The great thing about this is that only $164 million, or 0.9%, of the company’s loan portfolio falls under this category. So that is essentially a non-issue.

Author – SEC EDGAR Data

The last thing that I would like to touch on is how shares of the bank are priced. At the moment, shares are going for $34.92 apiece. That is actually 16.9% lower than the tangible book value per share of the bank. Another way to value the firm is by using the price to earnings multiple. Although this might be a bit on the high side because earnings are dropping so far this year, using results for last year would result in a multiple of 5x. This is actually the lowest of any of the banks that I have analyzed so far this year.

Takeaway

Based on the data provided, I must say that I really like what I’m looking at when it comes to Customers Bancorp. No, the financial institution is not perfect. I particularly don’t like the recent downturn in profitability and the historical volatility on that front. However, the firm’s book value per share and its deposit base continue to grow nicely. Add on top of this how cheap shares are, and I have no problem rating the company a ‘buy’ at this time.

Read the full article here