When asked about homebuilders, most investors’ immediate reaction would be that it’s a low-moat, cyclical, borderline uninvestable industry.

And yet, the sector produced some of the best-performing stocks of the recent decade, one of them being none other than America’s largest homebuilder, D.R. Horton (NYSE:DHI).

Let’s dive into what made D.R. Horton an extraordinary investment, its less-understood business model, and show why it remains a very attractive growth opportunity for long-term investors.

Introduction To Homebuilders, One Of The Best-Performing Sectors In The Market

In my bio, I make the following claim:

I aim to invest in companies with perfect qualitative attributes, buy them at a reasonable price based on fundamentals, and hold them forever.

How does a homebuilder fit that criteria, you might ask? Well, in this article, I hope to prove to you that it does.

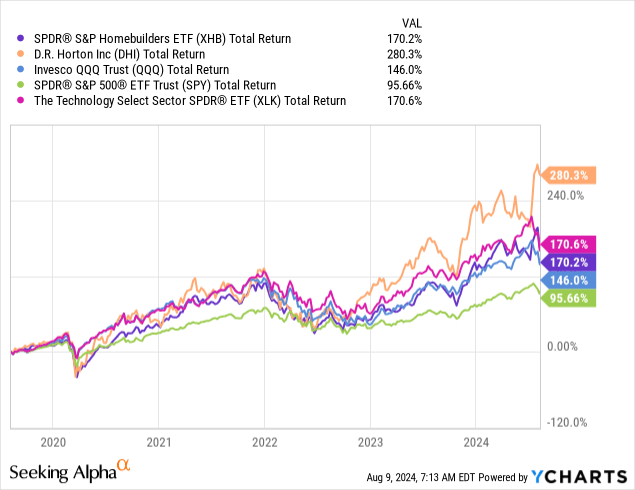

Here’s a little appetizer. As you can see, D.R. Horton outperformed both the S&P 500 (SPY) and the Nasdaq 100 (QQQ) by more than double over the past five years. It has also done so over the past decade. In addition, even the sector as a whole, represented by the Homebuilder ETF (XHB), has managed to keep up with the fast-growing Technology ETF (XLK).

I hope that has you hooked. With that, let’s dive in.

The Homebuilder Market – Supply & Demand

The homebuilder industry is predicated on three inevitable truths. One, people need to live somewhere. Two, people want to own the house that they live in. Three, the population is growing.

Combine the three of those, and you get stable and consistently growing basic demand. When I say basic demand, I’m talking about the desire to buy a house, which at this stage of the discussion, I’m separating from the actual ability to buy one.

According to estimates, the basic demand for housing in the U.S. is quantified somewhere in the 1.6 million houses per year range. This is primarily based on population forecasts, which on average expect the U.S. population to grow by 1.6 million people per year. House demolitions, which are estimated to be around 250,000 a year, and divorces, are also drivers for more basic demand.

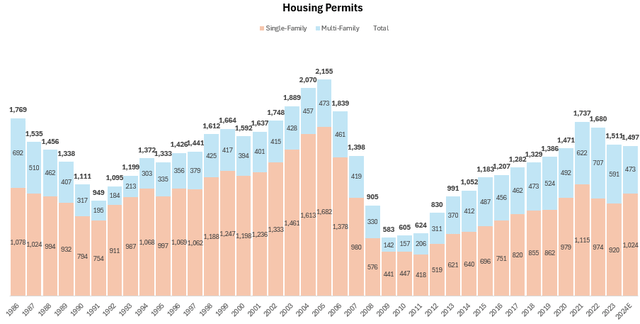

When it comes to supply, the easiest way to gauge its pace is by looking at housing permits:

Created by the author based on data from the U.S. Census

Over the last decade, we’ve had approximately 1.4 million permits per year, on average, representing a constant deficit.

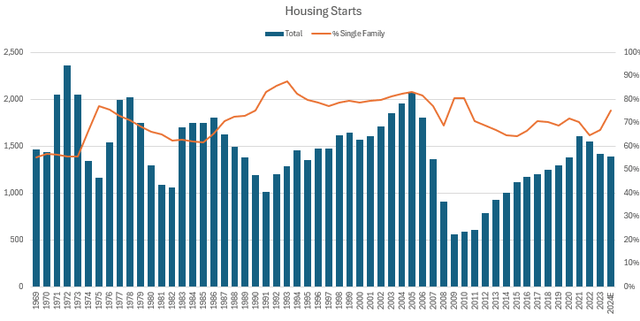

In addition, the industry’s capacity is constantly pressured by shortages of labor and building materials, leading to a deficit in housing starts as well:

Created by the author based on data from the U.S. Census

Now keep in mind, that this represents a consistent annual deficit, which makes the cumulative shortage bigger by the year. As it stands today, the cumulative shortage is estimated at around 4 million houses, with some estimates as high as 7 million and some lower, at 2 million.

So, considering there’s a basic annual demand of 1.6 million, if, somehow, the industry manages to achieve a building surplus of 100,000 houses a year (meaning it will start 1.7 million houses annually, something it hadn’t achieved since 2006), it’ll take over 20 years to bridge the gap to the lower estimate of the shortage.

The bottom line here is quite simple, homebuilders have no reason to worry about basic demand. This leads me to our next topic – affordability.

Turning Basic Demand Into Buying Demand – Affordability

Who doesn’t want a big house, with a nice pool and a place to barbecue? What prevents people from fulfilling their ‘wants’ is, obviously, being able to afford a house.

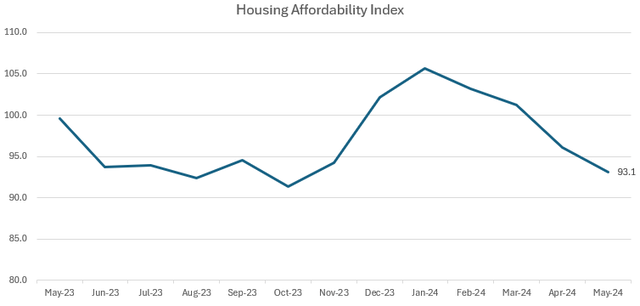

Housing affordability is the result of the median home price, median household income, and the current mortgage rate.

Created by the author based on data from FRED; Value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home.

As we can see, affordability is quite low according to the FRED index, and other indexes are showing we’re at an all-time low.

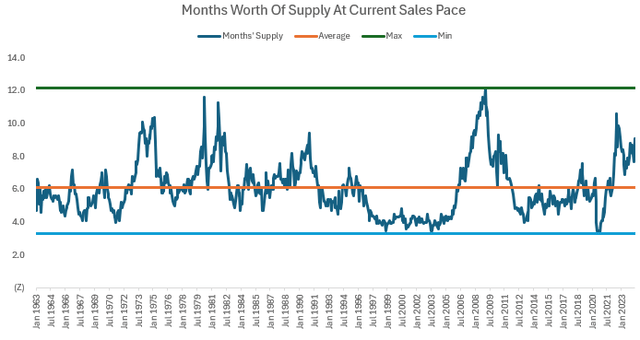

The affordability issue is the key reason the homebuilding industry is rightfully perceived as cyclical. There’s never a perfect balance between supply, demand, and affordability, which means there are periods when inventories are rising and supply is exceeding buying demand, even though the basic demand, and the shortage, still exist.

Created by the author based on data from the U.S. Census

We’re in the midst of such a period right now, as affordability and rate uncertainty are making homebuyers sit on the sidelines. This is why it’s crucial to understand the long-term forces underlying the industry, and why I think there’s no point in investing in homebuilders for the short term. That is, unless you’re trying to time the cycles, which is a tough feat.

D.R. Horton’s Unique Business Model & Scale Advantage

At this point, I hope that we established that despite being a cyclical industry, homebuilders do have long-term secular growth tailwinds, resulting from basic demand.

What’s unique about D.R. Horton, is that its business model is perfectly positioned to deal with cyclicality, and even benefit from it.

In the past, homebuilders, D.R. Horton included, used to buy land, develop it for a few years, build a model home, and then start selling houses. That business model was capital-heavy, produced little cash, and wasn’t that profitable.

Over the last 15 years or so, Horton transformed its model completely. As Greenhaven Associates’ Ed Wachenheim articulates perfectly in a Business Breakdowns Podcast:

The business has transitioned from being a real estate business to being a manufacturing business. Horton today is a high-volume manufacturer of homes.

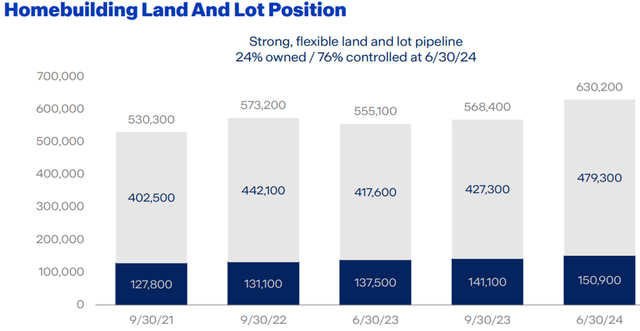

Today, Horton owns less than 25% of its land position:

D.R. Horton Q2’24 Presentation

This makes the cash cycle much more attractive and allows Horton to return capital to shareholders. Since 2018, Horton reduced its share count by nearly 14%, and it’s expected to accelerate repurchases in 2025 and beyond.

Also, the company has an exceptional balance sheet, with essentially no debt in the Homebuilding segment, as it doesn’t need to take leverage to grow.

Created by the author using data from D.R. Horton reports and U.S. Census.

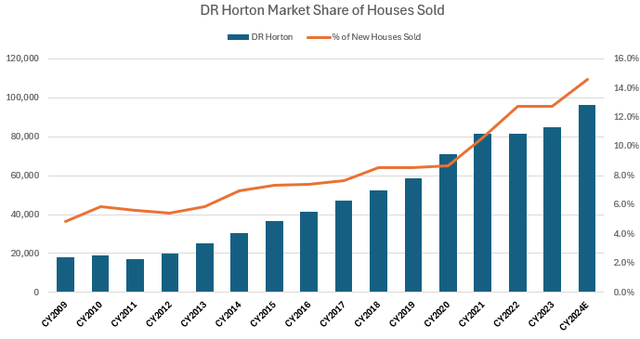

Over the years, these strengths enabled Horton to constantly acquire struggling competitors (primarily for the purpose of their cheap land), and constantly take market share. In 2024, Horton is expected to deliver nearly 15% of houses sold in the U.S., more than three times the market share it had in 2009.

This creates a virtuous cycle, as scale leads to better profitability, more cash, more growth, and more market share.

Growth Prospects & 10% Unit Count Growth Target

Usually, I research companies in a bottoms-up approach, meaning I stumble into a company I’m interested in, and then I look at the industry. In Horton’s case, it was the opposite.

After taking the time to study the homebuilder industry, heading into a rate-cut cycle, I wanted to pick my horse in the race. After screening through nearly twenty public companies, I was left with only two potential candidates, D.R. Horton, and Lennar (LEN). These two companies are number one and two in terms of market share, but Horton is bigger, has a more developed business model, and leans more toward first-time homebuyers, with selling prices in the $380,000 range.

Created by the author based on D.R. Horton reports, management guidance, and author’s projections.

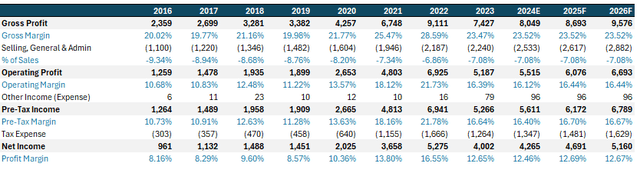

Since 2009, Horton grew its unit count at a 12% CAGR. A pace which it also maintained since 2016. That, combined with a 4% annual increase in the average selling price, resulted in a revenue growth CAGR of 15.2% from 2016-2023.

Management targets 10% unit count growth going forward, driven by consistent market share gains.

In my assumptions, I don’t take into account price increases, and for conservative purposes, I also reduce the unit count growth to 8%, although there’s nothing to suggest Horton can’t deliver its 10% target.

Created by the author based on D.R. Horton reports, management guidance, and author’s projections.

In addition, I don’t take into account margin expansion, as Horton is pretty steady at 23.5% gross margins and 16.5% operating margins. There’s no reason we won’t see operational leverage, but again, conservatively, I assume it’ll be offset by input cost fluctuations.

Created by the author based on D.R. Horton reports, management guidance, and author’s projections.

The company is already generating ample amounts of cash at the Homebuilding level, but its Rental arm, which rents single-family homes in a community and then sells them in bulk to institutional investors, was eating cash for a few years.

Now, they reached the scale that they wanted, and they expect consolidated cash flow to be much in line with the Homebuilding cash flow.

In other words, we’re approaching an inflection point in the company’s cash flow trajectory, as already reflected by their recent $4 billion buyback authorization.

Therefore, I expect buybacks to be more than 4% of the share count going forward.

The bottom line is this – D.R. Horton should grow core EPS by ~15% annually for the foreseeable future.

Valuation

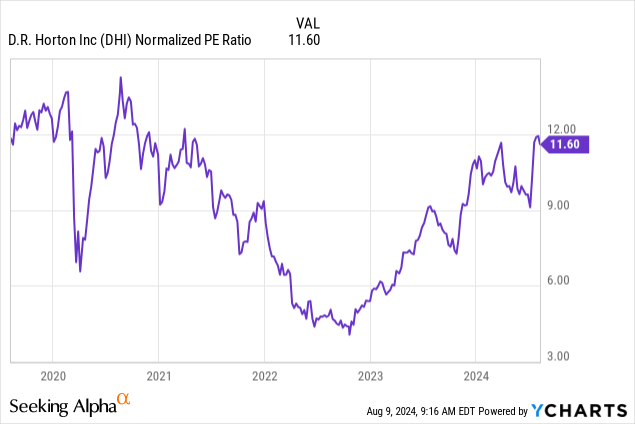

Historically, D.R. Horton trades at an 8x P/E at low times, and at 12x P/E at good times.

That is, while the most asset-light player in the industry, NVR, is trading pretty steadily in the 16x-17x range.

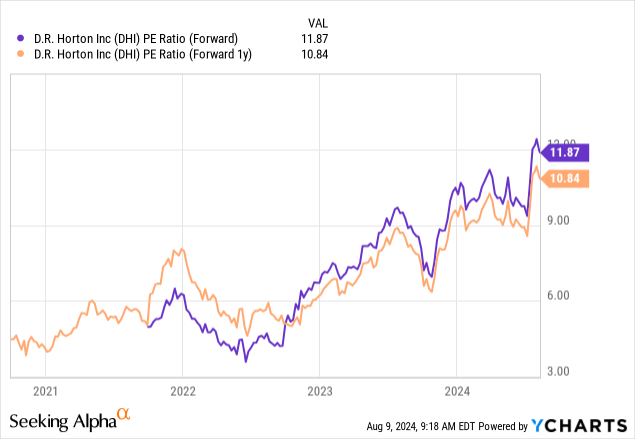

Today, D.R. Horton trades at 11.9 times forward earnings. However, the company’s fiscal calendar is one quarter ahead. For simplicity and comparability, let’s use the calendar 2025 numbers.

Currently, shares are at 10.6x, 2025 estimates, which I find a bit low. Applying a 12x multiple would put us at a fair value of $196 a share, reflecting 14% upside by early 2025.

In my view, the multiple could expand beyond 12x, as Horton’s cash conversion inflects and capital returns to shareholders accelerate. I’m not saying a 16x multiple like NVR, but 14x seems possible to me.

That would bring us to a fair value of $230 a share, reflecting 33% upside.

Risks

There are three key risks here, in my view.

Starting with the macroeconomic backdrop. This is a cyclical industry, and there are increasing concerns about a recession or a weak consumer. As I said, I think that Horton is perfectly positioned to deal with downturns, and any recession headwind will be somewhat mitigated by interest rate cuts. Still, it’s always possible that shares will respond badly to a recession.

Transitioning to execution. With any company, there’s the possibility that it won’t be able to deliver on expectations. Horton has quite an ambitious target for 10% unit count growth, and while I did take more conservative assumptions in my model, I believe that if they repeatedly fall short of the 10% mark, investors could rerate the company lower.

Lastly, competition. Horton has an impeccable track record of winning market share. It is expected to continue to do so, and nothing suggests it won’t, with all the competitive advantages we discuss. However, the moats in this industry are more about operational efficiency and economies of scale rather than differentiation. Yes, some homebuilders are building amazing homes, but the houses Horton is selling are much more basic.

Conclusion

Contrary to the common perception, homebuilders like D.R. Horton are growth companies.

Horton’s scale, unique business model, and operational excellence, position the company well to withstand the industry’s down cycles, and come out stronger.

Supported by a large housing shortage and steady basic demand, I expect D.R. Horton to continue to grow at a double-digit pace for the foreseeable future while improving the cash cycle and taking market share.

Ahead of an inflection point in cash flow, and accelerated capital returns to shareholders, I rate D.R. Horton a ‘Buy’ with a price target of $196 a share.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Growth Idea investment competition, which runs through August 9. With cash prizes, this competition — open to all analysts — is one you don’t want to miss. If you are interested in becoming an analyst and taking part in the competition, click here to find out more and submit your article today!

Read the full article here