As we get closer to recession during late 2023, investors have been getting nervous about the prospects for the cyclical maritime shipping industry. One of the larger players is Danaos Corporation (NYSE:DAC) operating a fleet of 68 container ships, based in Greece, with 4x the aggregate capacity in 2006 when share trading began in America.

I last wrote about the company with a bullish take in June here. Since then, the stock has delivered about +5% for investors including dividends, which has beaten the S&P 500 performance by about 10% (the S&P 500 is down -5% over the last five months).

Why does this stock jump out to me? Danaos management has decided to run the business in a completely different fashion than many in the industry, starting at the time of spiking shipping/charter rates during the COVID-19 pandemic. As of June, Danaos has stockpiled cash ($368 million) and paid off debt ($418 million left), in this usually capital-intensive, debt-heavy industry. Today, the company holds more current assets ($488 million) than debt, which is incredibly rare for a container shipping business, with total liabilities standing at just $695 million. DAC sports the most liquid balance sheet by far in shipping, and perhaps any transportation-related firm with decent size.

More good news for shareholders is the company, to a large degree, locked in the high shipping/lease rates of 2021 for years with customers using long-term pricing contracts. So, enormous cash flow is coming in the door right now, and the problem of what to do with all the money is one enviable concern for owners.

To boot, the stock price has been following industry equity trading trends downward, following stagnating to declining demand and quotes since 2021. The result of all these variables is that Danaos is now materially “undervalued” vs. net assets after all liabilities are subtracted. New share buyers can acquire a position at a whopping -53% discount to tangible book value! Honestly, it’s hard to find any stock in America with little debt, trading at a significant discount to net hard assets.

My view is both backward and forward valuation ideas point to a wonderful bargain for new investment. And, if the 10% autumn correction on Wall Street gets worse soon, lower prices in Danaos shares could open a welcome and very remarkable buying opportunity. I am talking about the kind of dirt-cheap acquisition entry that only appears once every 5-10 years in any equity (mainly during recessions).

Unique and Superb Valuation Stats

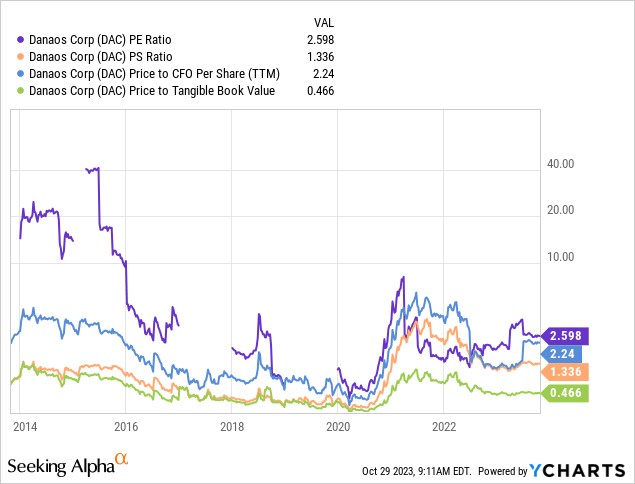

At first glance, Danaos looks somewhat inexpensive, using basic financial ratio analysis of underlying fundamentals. On price to trailing earnings, sales, cash flow, and tangible book value, shares are cheaper now than the 2014-15 and 2021 highs. Overall, however, a roaring bargain is not presented by these stats.

YCharts – Danaos, Basic Fundamental Valuation Stats, 10 Years

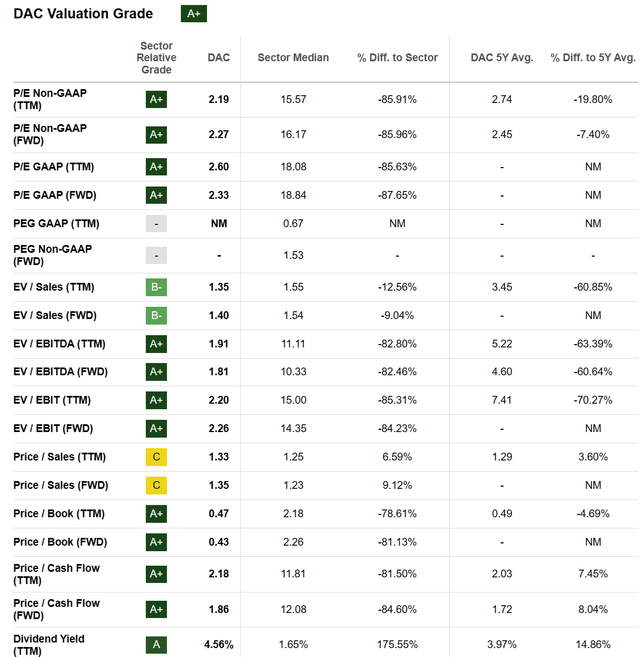

Yet, when we include the financial strength changes in debt and cash levels over the years, Danaos does stand out as an incredible value today. Seeking Alpha’s computer ranking and review of both price and “enterprise value” stats is screaming DAC is an excellent buy candidate. SA’s Valuation Grade for Danaos of “A+” is well deserved and might not even tell the whole bullish story.

Seeking Alpha Table – Danaos, Valuation Grade, October 29th, 2023

What am I and Seeking Alpha computers weighing specifically, that regular investors might be missing? Any business takeover or outright purchase by a single owner has to account not only for the share price, but also the debt acquired in any transaction. On top of this idea, if a company has plenty of cash on hand, not needed to run the business, a single private owner could pocket the cash and liquidate short-term assets for themselves. In the end, the enterprise valuation accounts for real-world worth of the whole business setup.

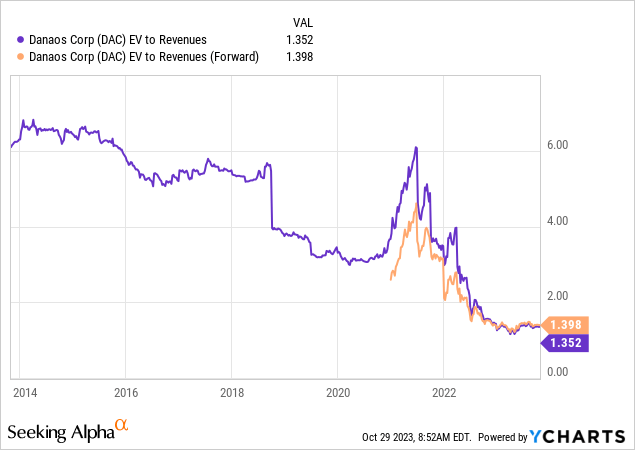

For example, the whole business value of debt and equity, net of cash, can be compared to sales generated by the business. When we look at EV to revenues over the last decade, we quickly see Danaos is currently selling at a record low. Today’s 1.3x EV multiple on sales is a better than 70% discount to its 10-year average above 4x.

YCharts – Danaos, EV to Revenues, 10 Years

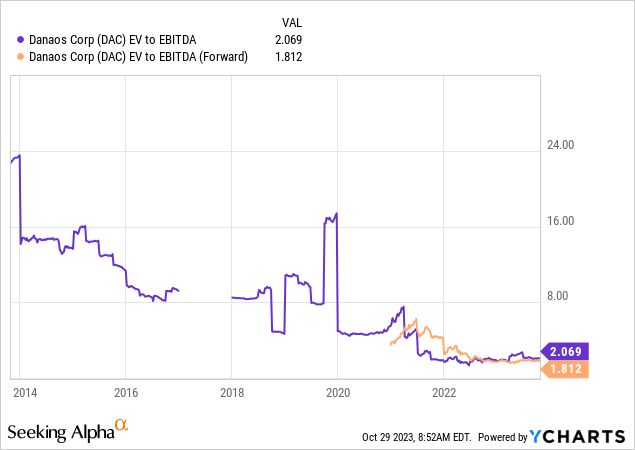

Again, EV to core cash EBITDA generation has imploded under 2x (using forward estimates) from a 10-year average over 8x. Who doesn’t want to own a business with difficult to replicate assets and customer contracts, holding almost no net debt, priced at 2x EV to EBITDA? The S&P 500 average company in comparison is sitting closer to 15x an equivalent construct.

YCharts – Danaos, EV to EBITDA, 10 Years

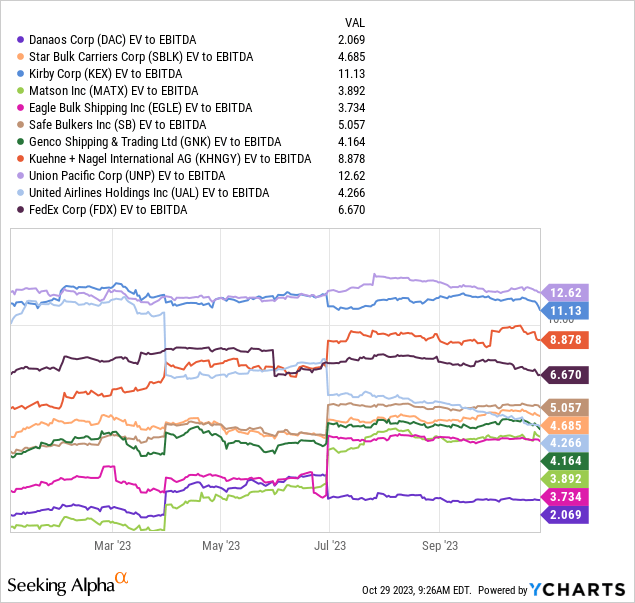

What about shipping and transportation peers? Well, Danaos is far and away the clear value pick in this sector of the economy right now. Its 2x trailing EV to EBITDA ratio is a wicked discount to everyone else operating a transportation business. Reviewing maritime shipping businesses or leading air, train, and truck goods movers in the 4x to 11x EV to EBITDA range (many with very high debt levels and rising interest costs associated with it), DAC’s valuation and balance sheet risk is sitting in a different dimension of positivity.

YCharts – Danaos vs. Transportation Peers, EV to Trailing EBITDA, Since January 2023

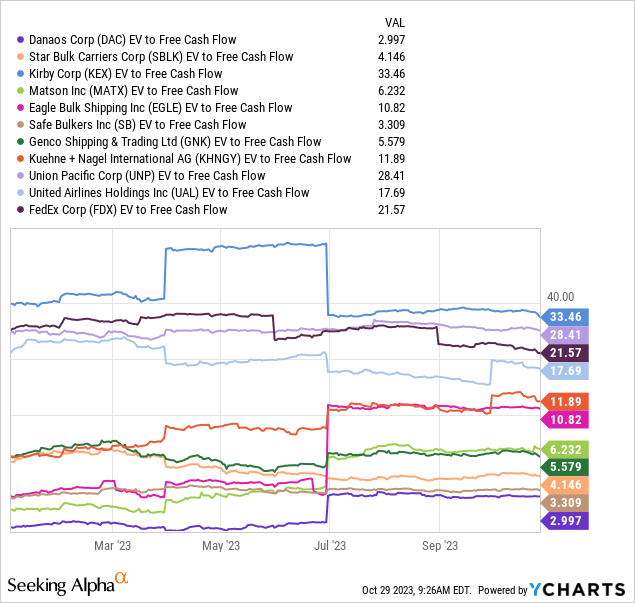

What about free cash flow? Every business owner wants cash in their pocket generated as soon as possible. Again, Danaos is the leading buy (or buyout) candidate on the metric of EV to free cash flow at ratio of 3x. What this means is any purchaser of the whole business, net of debt and cash, could theoretically pocket enough cash flow over three years to pay for the acquisition. A buyer would get repaid his/her initial investment quickly, and the remaining cash flow and earnings generated after 2026 would be gravy. You would also own/control 68 container ships, free and clear of debt. The vast majority of publicly-traded businesses in America are going for an EV to free cash flow multiple ranges of 10x to 30x today.

YCharts – Danaos vs. Transportation Peers, EV to Trailing Free Cash Flow, Since January 2023

Tangible Book Value Ideas

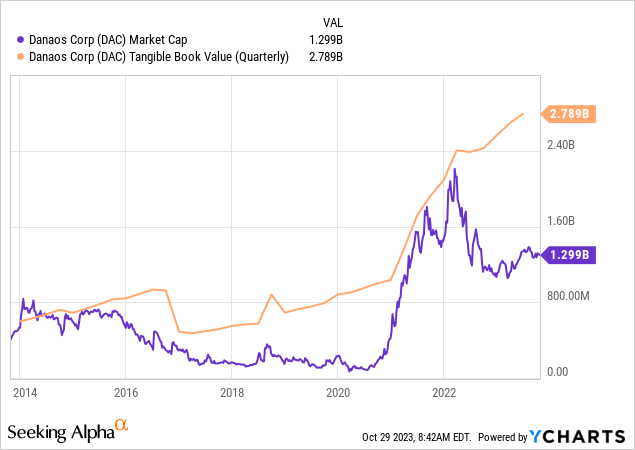

For me, the simplest valuation measure of all to understand is price to tangible book value. The original “value investor” book writers in the 1930s like Ben Graham harped on this concept, and yes, I am old school in my thinking. It’s definitely only a piece of the valuation puzzle to consider, but owning useful economic assets like ships that generally rise in worth/price with inflation (arbitraging replacement costs) is a key number to contemplate for DAC.

The greatest share price discount to tangible book value for Danaos was reached right after the pandemic started in early 2020 on economic shutdown fears. Believe it or not, we are now approaching the same level of underlying investment value at a price to tangible book value ratio of 0.47x.

YCharts – Danaos, Equity Market Capitalization to Tangible Book Value, 10 Years

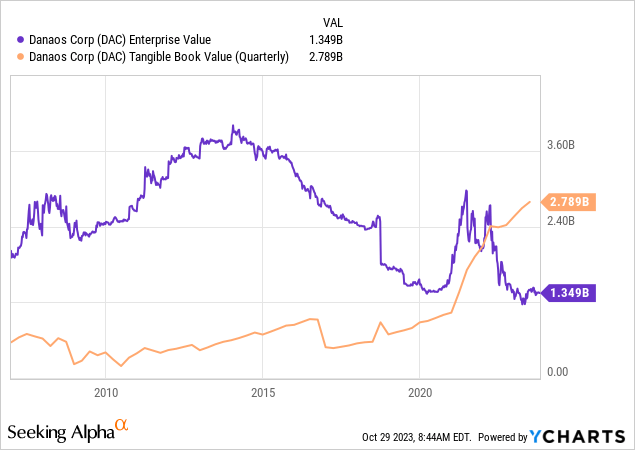

But that’s not all. The truly bullish story is found in management’s decision to slash debt and hoard cash windfalls beginning later in 2020. EV to book value has NEVER been anywhere near this type of bargain. Using the yardstick of average EV to tangible book value since 2007, a target price well north of $200 a share would be the mathematical result.

YCharts – Danaos, Total Enterprise Value vs. Tangible Book Value, Since 2007

Technical Momentum Review

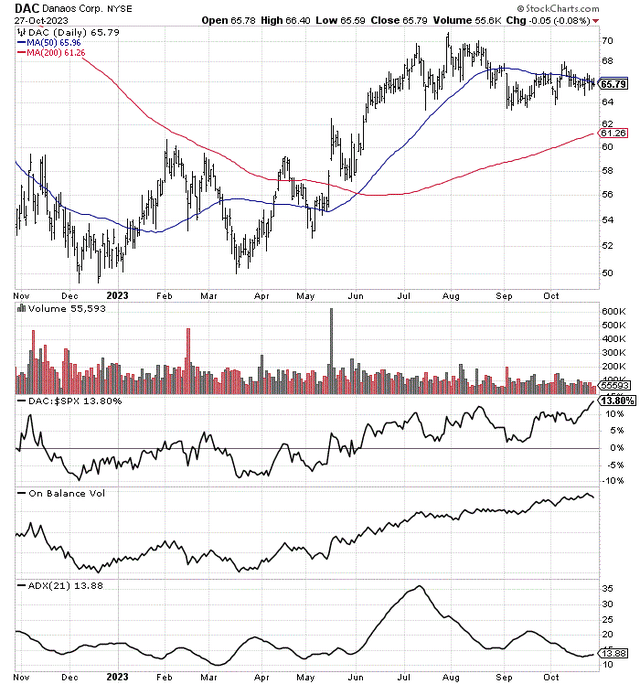

There’s also plenty of good news for owners on the trading chart. Relative strength vs. the S&P 500 has been picking up since early September. Price is above its 200-day moving average and trying to hold its 50-day moving average (less than 15% of all equities are trading above their respective 50-day after the September-October correction).

Daily trading volume has been abnormally low since August. From my experience, stocks drifting higher in price on low volume could be an indication of lack of overhead supply. If any positive news is announced by the company, price could jump appreciably.

On Balance Volume readings have been super-positive since March. Often, OBV leads price.

Reduced volatility can be a sign of balance between buying/selling interests. The 21-day Average Directional Index has been quite low again in October. Similarly low ADX scores often predate big upmoves in all types of equities. For example, ADX numbers in the 10-15 range were part of the March-May bottoming period for DAC’s quote.

StockCharts.com – Danaos, 12 Months of Daily Price & Volume Changes

Final Thoughts

What could go wrong with my bullish thesis? Two risks represent clear and present dangers. The first is management gets too aggressive with its balance sheet by entering a large dilutive acquisition that also adds substantial debt/leverage. The company was rumored to be close to buying out Eagle Bulk Shipping Inc. (EGLE) in June. While such a transaction for this smaller shipper may have been somewhat accretive long term, it would have changed the company’s future direction with added dry-bulk shipping exposure. A minor acquisition or two seems likely over the next couple of years, in my mind. It’s hard for managers to sit on lots of cash indefinitely while growing any business for size (diversification or economies of scale) is constantly a top priority.

A second risk to contemplate is a major and/or prolonged global recession could begin soon. Remember Danaos has locked in many shipping contracts/rates on its assets. So, an economic downturn is less of an immediate concern. Nevertheless, a prolonged recession could affect cash generation years down the road, while a deep one could cause some customers chartering ships to default on payments or demand reworkings of older deals. My view is both outcomes are remotely possible. Countering this risk, DAC’s low debt position means it should still perform better than other peer shippers.

On the positive side of the investment outlook, share buybacks in 2023 (probable in 2024) are incredibly accretive at currently ultra-low multiples of earnings, sales, cash flow, and book value. It’s entirely possible on management’s present course, for example, tangible book value will eclipse $200 a share in 2-3 years. So, buying around $65 may represent a discount of as much as 70% vs. what each share will actually represent in underlying ship value, over the intermediate term.

Don’t laugh too loud, but any unexpected upturn in shipping rates could send the share price back above tangible value quickly. What this means is the upside potential of owning Danaos is well above average vs. other transportation businesses and perhaps dramatically better than your average S&P 500 company today (which remains overvalued vs. rising interest rates and a weakening economy over time).

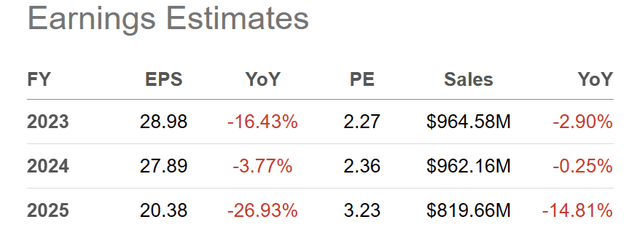

Sales and earnings are largely locked in place because of long-term contracts for 2023-25. Consequently, Wall Street analyst estimates over the next couple of years have not changed much since the summer. Charter coverage stood at 99% for 2023 and 86% for 2024 (reported on the Q2 earnings call).

Seeking Alpha Table – Danaos, Analyst Estimates for 2023-25, Made October 28th, 2023

As an investor, you are always on the hunt for a stock with at least one winning characteristic like a new product selling well with consumers, or a killer balance sheet, or above-average free cash flow generation. Sometimes, you can locate a company with two or maybe three attractive variables working in favor of shareholders. Rarely, can you find a company with a long list of reasons to buy like Danaos.

For sure, Danaos should be a part of your portfolio’s transportation exposure. I continue to rate shares a Strong Buy, especially for those looking to reduce risk in their sector weightings. DAC may offer some of the strongest risk/reward characteristics of any transportation equity available for investment.

An industry pricing/demand upturn in late 2024 into 2025 (post-recession) could support a Danaos price above its rapidly rising tangible book value. Such a move might place shares in the $200+ range by 2026, equal to an outstanding projected total return number (the company paid a 4.5% dividend rate over the past 12 months) above +200% over 36 months (approaching +60% compounded annually for three years).

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Read the full article here