Thesis

Denali Therapeutics (NASDAQ:DNLI) is a biotech company and forerunner in the field of novel treatments for neurodegenerative diseases, trying to identify novel targets in light of evolving science, and creating drug candidates that allow modulation of such targets. Additionally, the company has created a transport vehicle program that should allow payload delivery across the blood-brain-barrier.

Denali’s lead program is with DNL310 in the orphan disease MPS II. Denali regularly communicates data from a Phase 1/2 trial in that indication, is having talks with the FDA on accelerated approval, and should report topline data on its Phase 2/3 Compass trial later this year. That data looks promising, but this is a 2,000-patient per year indication, which I believe is not a reason to invest in Denali at the current valuation. There are some other programs in the in-house pipeline for ALS and MPS III that are interesting, but not compelling to me.

Denali has an extended portfolio including partnerships with big pharma names Biogen (BIIB), Sanofi (SNY) (OTCPK:SNYNF) and Takeda (TAK) (OTCPK:TKPHF). The Biogen collaboration is based around a LRRK2 inhibitor for Parkinson’s disease and a drug removing beta-amyloid. I find the LRRK2 inhibitor for Parkinson’s most interesting, but little data is communicated as to efficacy, and Biogen has already terminated the Phase 3 trial for monogenic LRRK Parkinson’s. The Sanofi partnership was based on RIPK1-inhibition, and may turn out a complete fail. The Takeda partnership for frontotemporal dementia with a progranulin-mutation and Alzheimer’s targeting TREM2 is interesting, but either early-stage or facing competitive threats.

At a $2.95 billion valuation and with $1.4 billion cash on hand, I believe Denali is a Hold.

Company

Introduction

Denali Therapeutics is trying to find solutions for several neurodegenerative diseases by modulating recently identified possible causes of these diseases. In so doing, it has been able to secure not less than three partnerships with big pharma, namely Biogen, Sanofi and Takeda. These partnerships have led to upfront payments, milestones and further royalties in exchange for the development by big pharma of programs for the treatment candidates they have in-licensed. Denali’s business model seems to be based in part on such early partnering possibilities.

Denali seems to want to move forward alone with its program in MPS-II or Hunter’s disease. That program is particularly promising, including reduction of NfL levels over 60% over the course of two years.

Denali also has a focus on transport vehicles to allow drug delivery across the blood-brain-barrier.

This is Denali’s five-year stock trajectory.

Five year stock trajectory (Google)

The company currently has a market cap of $2.95 billion, and has recently picked up financing of $500 million.

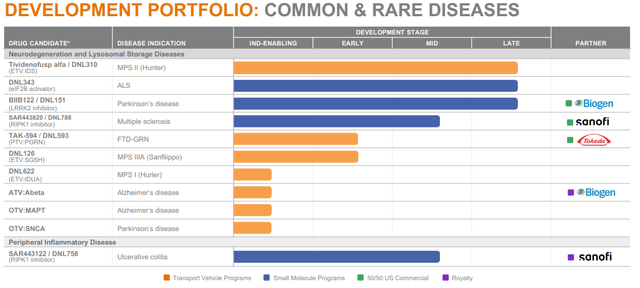

Pipeline

Denali’s has an extensive pipeline.

Pipeline (Corporate Presentation)

I will first discuss the two in-house programs for two types of MPS, then the trial I find most interesting in frontotemporal dementia with a progranulin mutation partnered with Takeda, then the Biogen partnerships and ultimately the Sanofi partnerships.

In-house programs

DNL310 for MPS II

The in-house program that gets the most attention is that for DNL310 in MPS II, so I will discuss that one first.

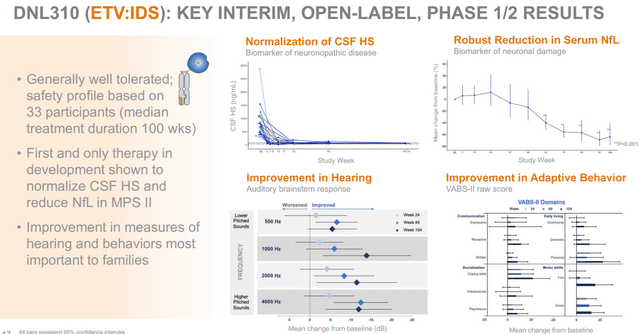

MPS comprises several subindications which are characterized by the impossibility to break down glycosaminoglycans. MPS II is caused by mutations in the IDS gene, leading to IDS enzyme deficiency, which causes the impossibility to break down glycosaminoglycans. The disease affects over 2,000 patients world-wide, with symptoms starting often at the age of 2, and current treatments do not affect cognitive capabilities due to the inability to cross the blood-brain-barrier. The current standard of care is an enzyme replacement therapy that does not cross the blood-brain-barrier, meaning the physical symptoms are addressed but not the ones related to cognition, hearing and behavior. Denali has up to two years of treatment data of patients in an open-label Phase 1/2 study, showing a drug safety profile consistent with that of standard of care. Furthermore, positive changes both on biomarker as functional levels are reported up to one year of treatment. In February 2023, Denali announced that 49 weeks of DNL310 treatment in the open-label stud led to positive changes on the VABS-II and BSID-III rating scales, respectively for adaptive behavior and cognitive capabilities, and that the drug improved hearing.

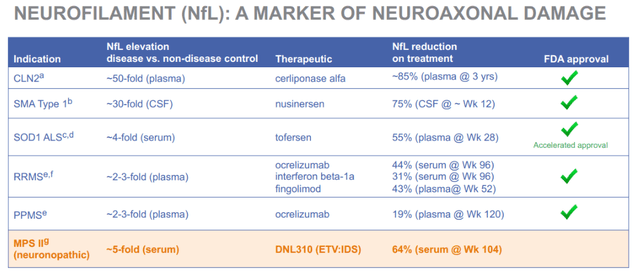

In June 2023, Denali announced a reduction of 64% from baseline in the biomarker NfL, a biomarker that is currently well accepted in the industry across neurodegenerative diseases as a biomarker of neurodegeneration. Apparently the FDA had suggested using NfL as an exploratory endpoint for diagnostic, prognostic and therapeutic assessments. This is a slide that was previously part of Denali’s corporate presentation, linking NfL reductions to approvals, and showing that DNL310 is performing well here.

NfL correlations with approval (Corporate Presentation (previous version))

The below slide sets out further biomarker reporting on DNL310, including reduction of heparan sulfate levels.

DNL310 Phase 1/2 results (Corporate presentation)

Denali is discussing with the FDA whether it could qualify for accelerated approval, possibly on the basis of the drug’s safety profile up to 85 weeks of dosing, and normalization of heparan sulfate levels. Apart from normalizing heparan sulfate levels, DNL310 also improved biomarkers of lysosomal function.

The company is completing a Phase 2/3 study called COMPASS in which it is recruiting up to 54 patients, and from which it should report topline data later this year. This Phase 2/3 trial should in any case allow the company to complete a package to apply for approval to the FDA.

DNL126 for MPS IIIA

MPS III or Sanfilippo syndrome is a lysosomal storage disease that results in the reduction of N-sulfoglucosamine sulfohydrolase, which should degrade heparan sulfate in the lysosome. There are currently no treatments for MPS III, which has a total market size of $ 1.7 billion, and several competitors are actively looking for a treatment here.

Denali has initiated dosing in its Phase 1/2 study in February 2024, and had at the same time released data showing correlations between heparan sulfate reductions in mice and cognitive improvements. This is an open-label trial in eight patients of an initial 25-week duration followed by a 78-week open label extension.

On June 3, 2024, Denali announced that this trial would be part of the FDA’s START pilot program, launched in September 2023 and intended to accelerate development of rare disease therapies.

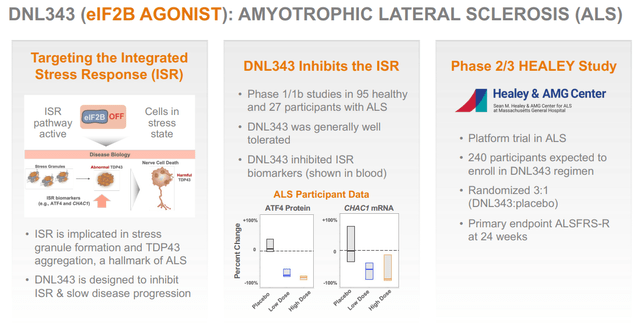

DNL343 for ALS

DNL343 is an eIF2B agonist targeting the integrated stress response, which Denali is using for the treatment of ALS. Phase 1/1b studies had shown that it was safe and well tolerated, and that there was target engagement.

Denali is currently testing DNL343 in a 24-week randomized placebo-controlled Phase 2/3 study in ALS in 240 participants, which has the ALSFRS-R as its primary endpoint.

In April 2024, the enrollment in the Phase 2/3 Healey trial was complete. That means topline data could be for the end of this year of the beginning of next year.

DNL343 slide (Corporate Presentation)

I do not see eIF2B emerging as a primary target in ALS, and hence I am expecting very little from this program. Again, there is limited data that could provide a strong confirmation that DNL343 could have efficacy in a disease as difficult to treat as ALS is.

Partnerships

DNL593/TAK-594 for FTD-GRN, partnered with Takeda

DNL593 or TAK-594 is a program that is partnered with Takeda for the treatment of frontotemporal dementia with a progranulin mutation, which drives disease progression. Using a transport vehicle, DNL593 aims to replace progranulin deficiency. If the treatment has effect, the question is, however, to what extent the progranulin deficiency accounts for the dementia.

Denali and Takeda have already shown that the drug was safe and well-tolerated, and that drug treatment led to substantial increases in progranulin levels in the central nervous system. Currently, dosing is taking place in the multiple ascending dose phase of the Phase 1/2 trial.

DNL919/TAK-920, partnered with Takeda

TREM2 is a receptor on microglia, which is believed to be involved in the pro-inflammatory and reactive phenotype that is causing neurodegeneration in Alzheimer’s. Modulating TREM2 could lead to the microglia reverting to their original nurturing function. Alector (ALEC) has a similar program addressing TREM2 in Alzheimer’s disease.

Takeda used to be running a Phase 1 single ascending dose study in healthy volunteers. In August 2023, it was announced that due to the impossibility to dose at higher doses, the program would be stopped. Alector’s program, a randomized placebo-controlled Phase 2 trial, is in any case further ahead. Alector’s partner for this program is AbbVie.

My personal view is that merely addressing this receptor on microglia may not be sufficient to reverse neurodegeneration. It is well-known that astrocytes and other innate immune cells are also involved in neurodegeneration, and that there is extensive crosstalk with peripheral immune cells such as T-cells and natural killer cells.

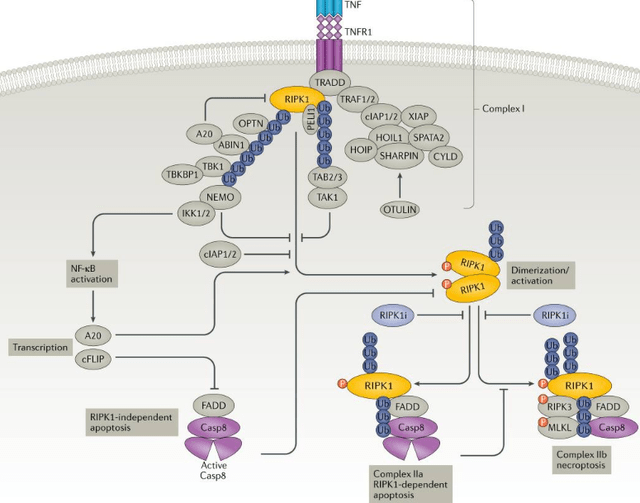

DNL747/SAR443820 for ALS and MS, partnered with Sanofi

DNL747 or SAR443820 is a RIPK1 inhibitor for the treatment of ALS and MS. It is based on the understanding that inflammation is involved in ALS and MS, just as it is in Alzheimer’s and Parkinson’s. RIPK1 is a protein that is part of the inflammatory pathway inside the cell, linked to the inflammatory TNF receptor 1. INmune Bio’s (INMB) XPro has its target more upstream, as it blocks soluble TNF outside the cell. Soluble TNF primarily signals through TNF receptor 1. In that sense, both programs were similar but not identical.

RIPK1 in the inflammatory cascade (Nat.Rev.Drug Discovery, Receptor-interacting protein kinase 1 as a therapeutic target)

In February 2024, an SEC filing reported that DNL747 had failed to reach its primary endpoint in a Phase 2 trial in ALS, failing to show functional improvement on the ALSFRS-R functional assessment scale. Sanofi will not further pursue trials with DNL747.

At the time, it is unclear whether this will also affect the other trial Sanofi is running in multiple sclerosis with DNL747, but logically the fail in ALS is not very promising for that study. In 2020, Sanofi had already paused development of DNL747 in Alzheimer’s disease.

The Sanofi partnership has been very profitable for Denali, as it was a $1 billion deal with a $125 million upfront payment to license multiple drug candidates targeting RIPK1 in multiple indications, but there have been several discontinuations. It is already clear at this point that RIPK1 inhibition will probably not be where the solution to neurodegenerative diseases should come from. Sanofi has abandoned the trial in ALS after it failed to reach and endpoint, which is obviously not a good result. It is unclear what will happen with its trial in multiple sclerosis.

DNL758/eclitasertib for ulcerative colitis, partnered with Biogen

DNL748 is another RIPK1 inhibitor that Sanofi was originally using for the treatment of ulcerative colitis and cutaneous lupus erythematosus. Sanofi had launched two Phase 2 trials for this compound, but has recently pulled out of cutaneous lupus erythematosus due to unoptimistic efficacy data, to pursue ulcerative colitis solely. The discontinuation followed a miss to meet the primary endpoint of change from baseline in the CLASI rating scale.

Denali may receive further milestone payments if development would be continued, but again I would say I am not especially optimistic about that given the recent decision related to cutaneous lupus erythematosus.

DNL151/BIIB122 – LRRK2 inhibitor for Parkinson’s disease, partnered with Biogen

LRRK2 mutations are one of the most common genetic risk factors for Parkinson’s disease, and is involved in lysosomal and mitochondrial dysfunction.

DNL151 is the furthest advanced LRRK2 inhibitor in clinical testing for Parkinson’s disease. Preclinical results had shown that reduction of LRRK2 expression could lower Parkinson’s symptoms, and Phase 1 and 1b results had shown that the drug was safe, well tolerated and lowered BMP, a biomarker of lysosomal function. Biogen and Denali originally had two studies running, one Phase 3 trial called LIGHTHOUSE which started in September 2022 in 400 patients focused on monogenic forms of Parkinson’s with a LRRK2 mutation, and one Phase 2b trial called LUMA which started in May 2022 in 640 patients with idiopathic Parkinson’s. The Phase 3 LIGHTHOUSE trial was subsequently terminated in June 2023 to allow a timely readout of LUMA, allowing patients from LIGHTHOUSE to join LUMA. LIGHTHOUSE was, in fact, only going to report data in 2031.

I believe this is a missed chance. Initiating a Phase 3 trial and then ending it within one year is a waste of money. Testing the idiopathic thesis first is probably the most important one. In comparison, Gain Therapeutics (GANX), which I have covered earlier, is focusing on Parkinson’s disease with a GBA1-mutation first, to then allow larger trials in idiopathic Parkinson’s disease. The preclinical work coming from Gain Therapeutics is apparently much further evolved than that of Denali, and scientific publications have shown links between GBA1 and LRRK2 dysfunction.

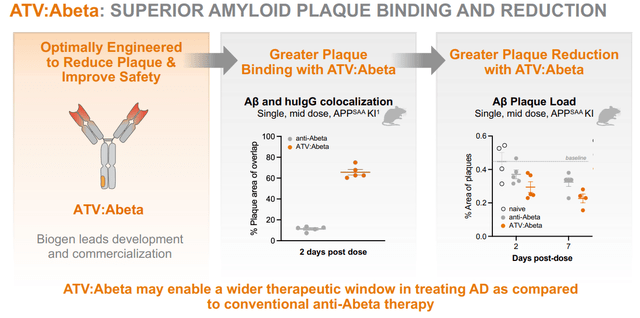

ATV:Aβ, licensed by Biogen

As mentioned above, Denali’s unique character lies in part in its transport vehicle technology, allowing delivery of drug payloads across the blood-brain-barrier. In April 2023, Biogen has exercised the option to develop and commercialize an anti-amyloid beta program with Denali’s transport vehicle, to hopefully enable improved clearance of amyloid aggregates and reduce the risk of developing ARIA – amyloid-related imaging abnormalities. In mice, the reduction of ARIA had been impressive.

ATV-Abeta program slide (Corporate Presentation)

This is an early-stage program at this time. As it is merely focused on amyloid-beta, which in my eyes, has shown all-in-all limited effects, namely at the most a 35% slowing of cognitive decline as shown by Eli Lilly’s (LLY) donanemab, I do not believe the immediate future of Alzheimer’s treatments is to be found here. Biogen will further develop and potentially commercialize this program, and apart from the option exercise payment, Denali may receive milestone payments and royalties on future net sales if certain milestones are achieved.

Financials

In February 2024, Denali picked up $500 million in financing from a private placement led by a U.S.-based healthcare-focused investor. The investors were not mentioned, but some large institutional investors are shown here and Baker Bros. is also an investor in Denali. The deal consisted of the issuance of 26 million shares of common stock at $17.07 and pre-funded warrants at $0.01 per share of common stock.

Subsequently, Denali’s latest quarterly report showed that the company had cash and cash equivalents of $1.43 billion as of March 31, 2024.

Denali’s cash burn is high, with about $90 million per quarter or $358 million over the last year. With that cash, Denali should be able to continue execution of its programs for at least two years.

Valuation considerations

Having assessed all of the programs Denali has both in-house and partnered, and its financial situation with cash at $1.4 billion, it is time to assess whether this biotech company warrants a valuation close to $3 billion. At this time, that is a net valuation of about $1.6 billion, but given the high cash burn of $358 million per year, that valuation may need to be reassessed frequently.

In short, I believe the company does not warrant a $3 billion valuation.

The partnership programs have been good cash generators for Denali so far, and there may be continued revenue from future partnerships, as partnering seems to be part of Denali’s business model. I see none of the above partnership programs at the stage where they are bringing any certainty or high potential that they will end up leading to substantial milestone payments or net royalties any time soon. In fact, given the repeated setbacks over the past few years, I expect Sanofi to discontinue its RIPK1 pipeline in the long run and end its collaboration with Denali. I could, of course, be wrong, but the current progress in any case does not look very promising, with terminations having occurred in Alzheimer’s and cutaneous lupus erythematosus, and a failure in ALS.

The Biogen partnership for Parkinson’s has seen Biogen terminate what I believed to be the most interesting part of the partnership, namely LRRK2 inhibition in Parkinson’s patients with a monogenic LRRK2 mutation. For reference, Biogen has had Qalsody approved in SOD1-ALS both in the US as the EU, and I believe doing a subgroup trial is the way forward in multifactorial neurodegenerative diseases. Doing a Phase 2 trial in idiopathic Parkinson’s patients is risky in my eyes.

The Takeda partnership seems to be intact, and both programs targeting FTD-PGN and TREM2 in Alzheimer’s are interesting, but these trials are earlier stage. I have expressed my concerns about targeting TREM2 in Alzheimer’s, however, and Alector is definitely in the lead here.

That leaves us with the programs Denali still fully owns itself. Both programs in MPS II and MPS III stand out, and the program in MPS II is late-stage and appears particularly promising. I assume Denali has a clear shot on goal here. But MPS II had a treatment market size of $358.9 million in 2018. There are treatments out there, just none that allow benefits in the brain due to their inability to cross the blood-brain-barrier. Denali will have to win over that market, which may go slow and cost efforts. At this point, I am not willing to give this program more value than the total market size of MPS II.

The program in MPS III is early-stage at this point, but shows some promise.

The program in ALS with DNL343 will report topline data either at the end of this year, or the beginning of next year. I do not see why targeting eIF2B or the integrated stress response would be particularly compelling in ALS at this stage.

Meanwhile, at $358 million per year, Denali’s cash burn is so high that it risks running out of money in three years.

Please note that Wall Street analysts on average see a 76.98% upside to the stock.

Risks

Investing in a biotech company without revenue and multiple partnerships comes with the risk that one or more of these partnerships may end at a given point. I am looking in particular at the partnership with Sanofi in this regard. The ending of such partnerships may lead to a price drop.

There is also a considerable regulatory risk. The FDA may choose not to let trials start or put them on a clinical hold.

Finally, there is the competitive risk. I have mentioned several other companies which I believe are making interesting progress in various neurodegenerative indications. The closest competitor that has similarities to Denali seems to be Alector, but competitive threats could also be coming from smaller players such as Gain Therapeutics in Parkinson’s, INmune Bio or Coya Therapeutics (COYA) in Alzheimer’s and ALS. There is also some competition in MPS, as mentioned above.

Conclusion

Denali Therapeutics is an interesting biotech company because it is one of the bigger players with several partnerships in the neurodegenerative space. Denali is flush with cash after a recent $500 million private placement which, I assume, was led or at least participated in by Baker Bros.

I am, however, not so bullish on most of the programs that have been partnered. I fear that Sanofi may further terminate its partnership with Denali. The partnership with Takeda may be the most promising one, but it is early-stage. I think Biogen’s termination of the LIGHTHOUSE trial in monogenic Parkinson’s with an LRRK2 mutation was a missed chance, and am not particularly bullish about the other programs partnered with Biogen.

The in-house programs Denali has are interesting, and most particularly its MPS II program. The market size for MPS II is however not so large in light of Denali’s market cap and enterprise value. The Phase 2/3 trial targeting eIF2B or the integrated stress response in ALS does not come across as especially compelling, but a win here at the end of this year or the beginning of next year may logically be a game-changer.

Given the high cash burn of $358 million per year, Denali has, I do not see how the company should be valued higher than it currently is. For the above reasons, I am giving Denali a Hold rating. Please note that this rating is different to that of Wall Street analysts, which on average see a 76.98% upside to the stock.

Read the full article here