Market Commentary

Markets moved modestly higher in Q2, delivering positive returns across most regions and countries. US stocks rose +3% (as measured by the Russell 3000 Index) — though gains were primarily thanks to large-cap stocks, which were up nearly +4%. Down the cap spectrum, returns were negative, with mid caps and small caps each down roughly -3%, as measured by their respective Russell indices. From a style perspective, growth maintained its sizeable lead over value, with large-cap growth up +8%, while large value was down -2%; mid-cap growth and value each fell roughly -3%, while small-cap growth fell -3% and small-cap value fell nearly -4% (all returns as measured by the respective Russell indices).

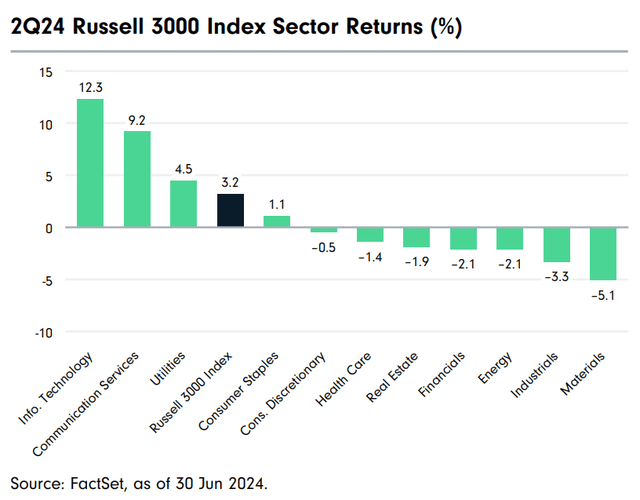

From a sector perspective, technology (+12%), communication services (+9%), utilities (+5%) and consumer staples (+1%) were in the black in Q2 — the first three tied partly to meaningful momentum around AI-related technologies and the implied energy demand, which helped boost utilities. The relative resilience of utilities and staples is also likely due somewhat to a growing preference among investors for more defensive sectors as the economic and market cycles get increasingly long in the tooth. Conversely, materials (-5%), industrials (-3%) and energy (-2%) led the way down. Financials (-2%), real estate (-2%), health care (-1%) and consumer discretionary (<-1%) were also in the red.

As has been expected for several months, monetary policy among major central banks diverged in Q2 as the European Central Bank cut rates while the Bank of England and the Federal Reserve held. Further, Fed chair Jerome Powell maintained his position that US rates are likely to remain higher for longer, signaling that there is expected to be only one rate cut before the end of the calendar year. Given the US’s economic resilience — exemplified by resilient employment numbers — and inflation’s ongoing stickiness, Powell’s commitment is not particularly surprising. What naturally remains to be seen is how durable the economic data prove to be in the coming months.

Meanwhile, in the wake of finally exiting its protracted negative interest-rate regime, the Japanese Central Bank (JCB) faces ongoing challenges maintaining the yen’s value, which has continued sliding relative to the dollar as US interest rates remain high. Though inflation in Japan has finally ticked up, which should give the JCB room to contemplate rate hikes, domestic consumer sentiment has been fragile as a weak yen has translated into high import and fuel costs. The JCB undoubtedly faces a delicate balancing act in the months and quarters ahead as it seeks to finally end decades of economic malaise.

Similarly, the ongoing global monetary policy and macroeconomic mix continues complicating the picture for a Chinese government which is seeking to boost its economy while facing growing trade tensions with Western countries — especially the US and the European Union, both of which have been ratcheting up restrictions related to electric vehicles and technology more broadly. Positively, Chinese GDP grew 5.3% year over year in Q1 — beating expectations and incrementally better than Q4’s 5.2%. However, much of the growth has been attributable to the economy’s supply side, which the government has provided ample support, while the demand side and the country’s consumers continue struggling to recover from a deep real estate crisis that has crimped wealth and led many to cut back on spending.

It’s been hard to miss the recent performance of AI-related stocks — which has contributed to an increasingly narrow market as a small number of massive technology stocks drive the majority of index returns. Against this market backdrop, it’s natural to question whether and how long the bull market can continue. However, this affords us an opportunity to add value for our clients as we avoid the temptations of swimming with the tide and maintain our disciplined adherence to our philosophy, which looks out past the latest trends to the longer term. We also believe it offers an increasingly interesting environment to deploy our time-tested, fundamental approach to identifying high-quality, underappreciated companies that may be easy to miss when they aren’t necessarily on the obvious front lines of the latest fad.

Performance Discussion

Our portfolio underperformed the Russell 3000 Index in Q2. Relative weakness was concentrated among our industrials holdings, which trailed benchmark peers, as well as our overweight to the underperforming sector. Our relative underweight to the top-performing technology sector also weighed on relative returns — though it’s worth noting our individual holdings outperformed benchmark names. Our consumer discretionary and staples holdings also posed a relative headwind in the quarter. Conversely, our energy and materials holdings provided a modest performance boost.

Among our top individual contributors in Q2 were Amazon (AMZN), Texas Instruments (TXN) and Mr. Cooper Group (COOP). Internet retail and cloud infrastructure company Amazon is benefiting from strong profitability, particularly in its Amazon Web Services (AWS) business. Shares also received a boost amid growing optimism around the demand for AWS as Amazon customers’ investments in generative AI projects continue growing.

Shares of semiconductor manufacturing company Texas Instruments rose in Q2 as demand in several of the company’s end markets show signs of recovering. Given the company’s long-term prospects, competitive positioning and scale advantages, we believe the outlook for the company from here is strong. Mortgage-servicing company Mr. Cooper Group is benefiting from a high interest-rate environment, which is supporting increased profitability in the mortgage-servicing business.

Other top individual contributors in the quarter included Coherent (COHR) and new holding International Paper Company (IP). Coherent is a global leader in materials, networking and lasers for the industrial, communications, electronics and instrumentation markets. The company is benefiting from rapid growth in AI-related transceiver sales. Investors were also seemingly encouraged by Jim Anderson’s hire as the new CEO. Anderson came from Lattice Semiconductor (LSCC), where he had an excellent track record.

International Paper is one of the US’s largest manufacturers of containerboards, which is used to make corrugated boxes and other packaging materials. We expect that as the demand environment improves and the company focuses on its commercial execution, it will be able to improve profitability and bring operating margins back to normalized levels. Given what we view as an attractive valuation for a high-quality company, we capitalized on the opportunity to initiate a position in Q2. Shares subsequently rallied after reports that Brazilian company Suzano (SUZ) is interested in acquiring the company.

Among our bottom individual Q2 contributors were Lear Corporation (LEA) and Regal Rexnord (RRX). Leading global automotive seating manufacturer Lear underperformed in Q2 as slowing electric vehicle (EV) adoption weighed on the company’s E-Systems segment in the near term. Further, rising dealer inventories are contributing to some concerns about the near-term demand outlook — though it’s worth noting dealer inventories remain below pre-COVID levels.

Shares of electric motors and power transmission components manufacturer Regal Rexnord were pressured against a backdrop of macroeconomic concerns which are seemingly making investors hesitant to own leveraged cyclical companies like RRX. However, we maintain our conviction in the outlook for RRX and believe that over the long term, it will capitalize on merger synergies to improve margins, increase organic growth and generate meaningful free cash flow, which should allow it to deleverage.

Other bottom contributors in Q2 included CarMax (KMX), Target Corporation (TGT) and Enovis (ENOV). Shares of used car dealer CarMax declined amid concerns surrounding the company’s ability to continue taking market share. While vehicle affordability continues pressuring the used car industry broadly, CarMax is focused on maintaining profitable sales and right-sizing its cost base to better position itself to capitalize on a more favorable environment. US-based mass retailer Target faces concerns about a slowing consumer discretionary spending environment, which weighed on shares in the quarter.

Shares of innovative medical technology company Enovis were pressured amid some short-term headwinds related to the integration of a recent acquisition. While some were quick to conclude the boost Enovis and the medical technology industry overall received from a COVID-era backlog of surgeries is winding down, we believe Enovis remains well-positioned to continue taking share as it cross-sells new products. Further, we believe the market is undervaluing the company’s ability to use its continuous improvement-focused business system to drive above-market organic growth, make accretive acquisitions and meaningfully expand margins over the long term.

Portfolio Activity

Still-rising valuations have made identifying attractively valued, high-quality companies increasingly challenging — though we still found a few in Q2 that we believe the market is overlooking amid its increasingly narrow focus on the mega-cap technology stocks dominating the major indices. In addition to International Paper, we initiated new positions in Starbucks and Abbott Laboratories (ABT) during the quarter.

Starbucks (SBUX) is the global leader in the coffee industry. Given its significant scale, we believe Starbucks can maintain its average ticket growth and drive decent traffic growth, which should allow for some margin expansion. While macroeconomic and competitive pressures remain intense in China, the country accounts for a minimal percentage of today’s earnings, and we believe the current valuation embeds little to no contribution from China over the long term, which we view as too cynical. As the share price declined recently amid near-term concerns surrounding store sales in North America and China, we capitalized on what we considered an attractive entry point.

Abbott is a diversified health care company with an extensive portfolio that spans medical devices, pharmaceuticals, nutritionals and diagnostics. With a substantial portion of its revenues generated internationally, emerging markets contribute about 40% of overall sales. We have always liked Abbott’s diverse mix of businesses and its fundamental growth prospects. The management team has consistently demonstrated skill in capital allocation, highlighted by strategic divestitures such as the European generic business in 2014, and significant acquisitions like St. Jude in 2016.

We exited our positions in HSA-focused bank Webster Financial and plant-based food and beverage producer SunOpta (STKL) during the quarter in favor of more compelling opportunities. We also concluded our investment in health insurance company Humana (HUM) in the wake of near-term turmoil in the Medicare Advantage market that led us to rethink the competitive landscape for Medicare Advantage plans in a normalized environment. We used the proceeds to fund higher-conviction ideas.

Market Outlook

Strong corporate earnings and economic growth continued in Q2, which helped bring the Russell 1000 Index’s year-to-date performance to +14.2%. However, the market has narrowed again, with a large portion of returns driven by a small handful of mega-cap tech stocks. Nearly two-thirds of this year’s return has been driven by six stocks: NVIDIA, Meta Platforms, Microsoft, Alphabet, Amazon and Apple. Year to date, NVIDIA (NVDA) alone has contributed nearly one-third of equity market returns with its +150% increase.

Over the past 10 years, growth stocks’ outperformance relative to value stocks has been astounding at over 8 percentage points annually. However, it is interesting to note this has not been driven by value stocks’ poor performance. On the contrary, the Russell 1000 Value Index has increased more than 8% annually over the past 10 years — in the range of long-term equity returns.

Similar to the performance disparity among growth and value stocks, small caps continue to underperform large caps. Year to date, small caps have underperformed by more than 12 percentage points, and over the past 10 years, they have underperformed by about 5.5 percentage points, annualized. By some measures, small caps are trading near a historically low valuation premium relative to large caps.

Corporate earnings are expected to grow at a double-digit rate in 2024, driven by mega-cap tech stocks, a rebound in health care sector earnings after a large decline in 2023 and growth from the financial services sector.

With the continued rally, equity market valuations remain at above-average levels. While this has been somewhat supported by the fall in interest rates since their peak in October 2023, it may still be difficult to generate returns from current levels that match historical averages over the next five years. However, we continue to seek attractive opportunities with the potential to generate above-average returns over that period.

Our primary focus is always on achieving value-added results for our existing clients, and we believe we can achieve better-than-market returns over the next five years through active portfolio management.

Read the full article here