WisdomTree U.S. LargeCap Dividend Fund (NYSEARCA:DLN), launched on 06/16/2006 by WisdomTree Inc. and managed by Mellon Investments Corporation and WisdomTree Asset Management Inc., is an ETF that tracks the performance of the WisdomTree U.S. LargeCap Dividend Index.

With $4.09B in AUM and monthly distributions, this is an ETF that is worth some consideration by income-focused investors. Its methodology isn’t too sophisticated for the expense ratio it charges, which presents some drawbacks, but I think that a lower price level would make DLN a worthy addition to a conservative income portfolio for the long term.

Methodology

The ETF provides exposure to large-cap stocks that pay dividends in the U.S. through its replication of WisdomTree U.S. LargeCap Dividend Index’s performance before fees and expenses. The parent index is the WisdomTree U.S. Dividend Index out of which the benchmark selects the 300 largest companies based on market cap and is supposed to track the performance of all the U.S. dividend-paying stocks, subject to liquidity, dividend consistency, and other requirements. Keep in mind that the benchmark doesn’t have a methodology different from the parent’s except for this market-cap filtering.

The parent index and, consequently, the benchmark follow a dividend-weighting approach whereas each stock is weighted based on how large the sum of its cash dividends is on a dollar-value basis; the larger the dividend, the greater the weight. It’s worth noting that weighting based on yield or payout ratio may be more attractive, as such metrics would have a lower correlation with the size of the business. That’s because the calculation of the index here is the projected dividend per share multiplied by the number of common shares outstanding. This will result in a situation where stocks underlying bigger businesses are given greater weight than the ones underlying smaller ones, but which represent better value based on yield and a fatter distribution of income based on the payout ratio.

That being said, there seems to be an effort for stable dividend income here, which very conservative investors may appreciate. First, because such a dividend-weighting approach could be the expression of the reasonable hypothesis that larger enterprises operate more mature businesses and, therefore, have a higher likelihood of maintaining the current dividend policy for longer. Second, because the index uses a 12% dividend yield cap; if a constituent has a yield higher than 12%, the index won’t consider the excess dividends expressed by the spread. In other words, it will calculate its weight by multiplying its market cap by 12%, ignoring a portion of the total dividend stream.

Though I generally find more sophisticated approaches to dividend portfolio management more appealing, I appreciate the obviously cautious yet simple nature of the approach that DLN follows.

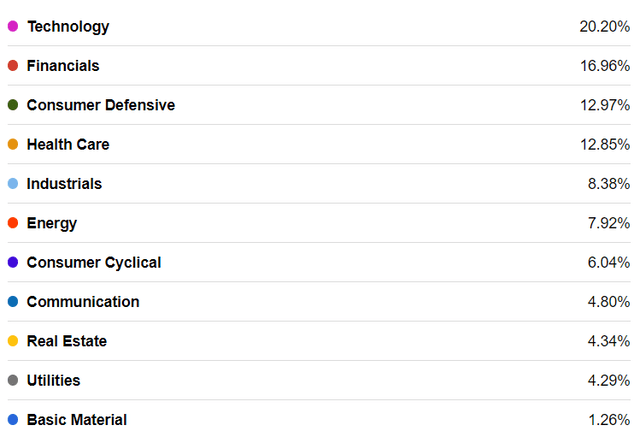

Allocations

This approach, however, results in a very high-tech concentration as tech companies provide the largest dividend streams for the portfolio because of their dominance in size. That being said, 20% is a lot better than one third of the portfolio being exposed to the industry, as is the case with SPY.

Seeking Alpha

Financials coming second is not surprising either given the fact that this is a more traditional sector out of which the more mature institutions don’t have such growth potential as to justify not paying a dividend. The downside of the weighting approach, however, is reflected in the fact that real estate takes up only 4.34% of the portfolio. As most of the sector is represented by REITs which are famous for their generally above-average yields, a more meaningful allocation would boost the currently low yield of DLN (more on that in a moment). On the bright side, it could have completely excluded the sector as many funds do because REIT dividends are not qualified, so there’s that at least.

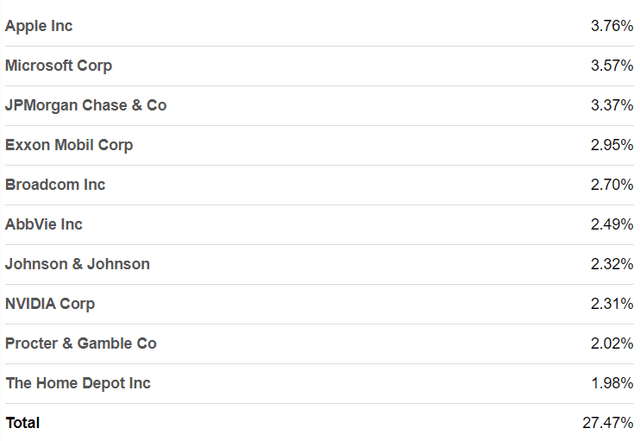

In any case, this cautious approach to weighting has resulted in Apple Inc. (AAPL) being the top constituent. Its dividend yield is currently 0.43% and the company has been paying a dividend since 2012; this represents neither a good dividend return nor an impressive payment record. Of course, total returns matter, and Apple may be a good enough allocator that makes paying any dividend a waste. However, DLN is an income-focused fund, so this doesn’t really apply as an argument here. AAPL, being the largest holding, is the perfect example of the methodology’s weakness. The rest of the top holdings have similar shortcomings.

Seeking Alpha

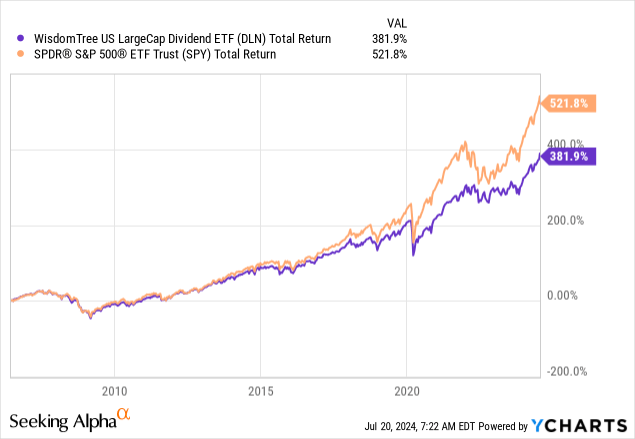

Performance & Cost

Since its inception, DLN has delivered an average annual return of 8.94%. While this is not bad on an absolute basis, it has underperformed the broad equity market in the long run:

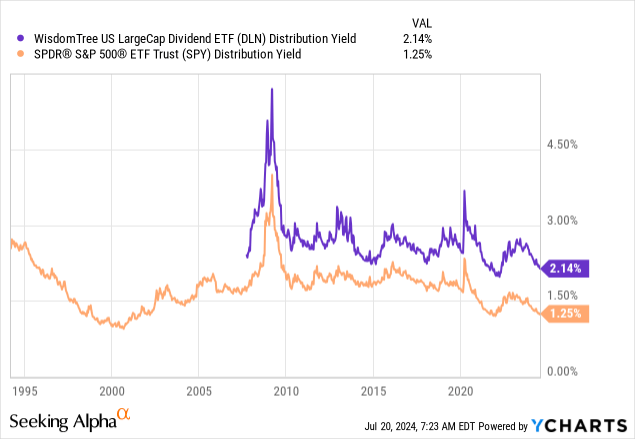

However, the performance difference here is the price investors paid for higher income and on a monthly basis. The yield spread has always been significant:

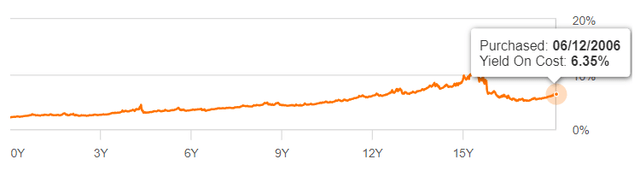

Someone who invested in the fund when it was launched would enjoy a very competitive yield on cost today because of DLN’s passive approach that probably results in a generally low turnover for the largest holdings over time.

Seeking Alpha

While that shouldn’t be understated when considering the long-term needs of passive income investors, I don’t believe this is the best time to buy DLN. Its dividend yield today is 2.29% and this accurately reflects the overall high price of the portfolio; its earnings multiple and book value premium are 21.62x and 300%, respectively.

So, I think that such a valuation results in a fundamental cost which, along with an expense ratio of 0.28%, should discourage investors from adding this ETF to their portfolios or allocating more to it right now.

Risks

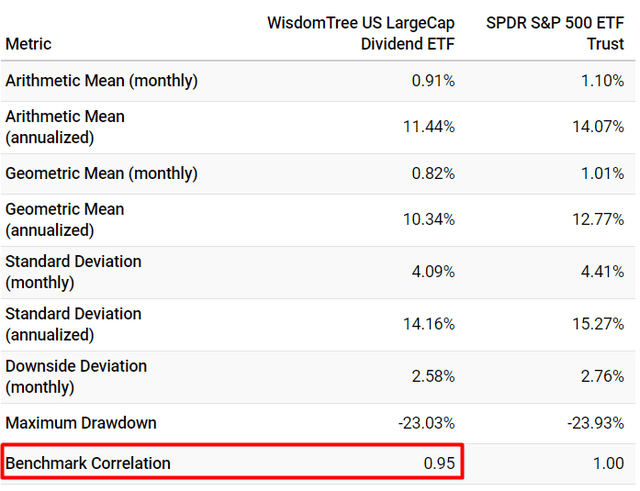

The first risk is related to the high price of DLN, as this is also a product of its high correlation to the market.

Portfolio Visualizer

The concentration in the technology sector, while less extreme here, presents the risk that comes with high volatility. Stability is one of the keys to successful passive dividend investing, so volatility can be an issue at times when the investors need to transfer funds.

The exposure level of financial stocks also makes the interest rate risk more significant here due to the sector’s high sensitivity to interest rate changes. Since there’s a good chance that we are going to start seeing lower interest rates this year, I’d say that the outlook appears positive now, however.

Verdict

This is a good dividend-focused ETF at a bad price, so while I’m rating it a hold for now, I think that adding it to a watch list and monitoring it in case of a better price level which would drive the yield to a more attractive level is worth it.

Do you own DLN? If so, what is your cost basis? Or do you prefer some other ETF for dividend income? Feel free to share below! Thank you for reading.

Read the full article here