Overview

My recommendation for DocuSign (NASDAQ:DOCU) is a hold rating as it is expected to remain weak over the near term, challenged by the weak macro environment. The recent key metrics also support my pessimistic view. With the weaker growth profile, DOCU should continue to trade at a discount to peers, making the stock currently fairly valued.

Business

The central focus of DocuSign’s primary offering is centered on its core electronic signature solution. The E-Signature module facilitates the streamlined transmission of documents for electronic signatures within corporate environments. DocuSign exhibits seamless integration capabilities by establishing connections with more than 350 application programming interfaces (APIs), encompassing prominent platforms such as Microsoft Word and Salesforce. When generating a document for electronic signature, users have the ability to conveniently designate the specific sections within the document that necessitate signatures. Subsequently, they can transmit the agreement to the intended recipients. The integration of E-Signature includes several e-signature extensions, such as DocuSign Click, which allows users to utilize click-wrap agreements. Additionally, it incorporates DocuSign Identity, which facilitates the verification of user identities. Furthermore, it enables users to request payments from recipients alongside their signature through the use of DocuSign Payments.

DOCU revenue is split between two streams: subscriptions and professional services. Of which, subscription is the main driver of growth, representing 97% of revenue as of FY23. DOCU is classified together with other high-growth software companies, where it has seen tremendous growth over the past few years. Total revenue grew from $381 million to $2.5 billion in just 6 years (from FY17), a staggering CAGR of 37%. However, attention should be paid to the past two years, where DOCU basically gave up a large chunk of growth potential in order to turn EBITDA profitable. Revenue growth stepped down from 45% in FY22 to 19% in FY23, while EBITDA margins turned profitable. Thankfully, management has done a good job of ensuring the business does not face liquidity issues as it is in a net cash position currently, with $1.4 billion in cash and $725 million in debt (excluding operating leases).

Recent results & updates

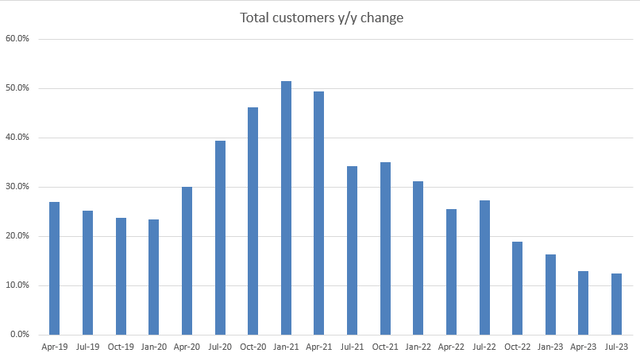

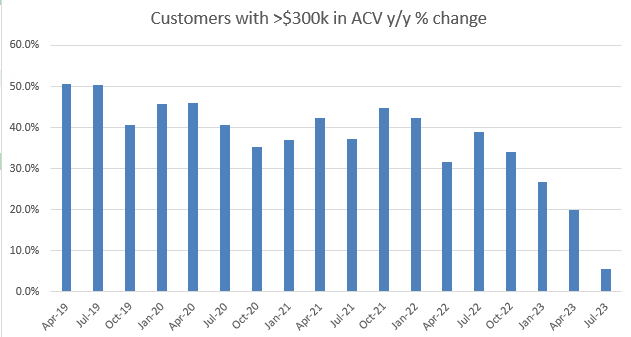

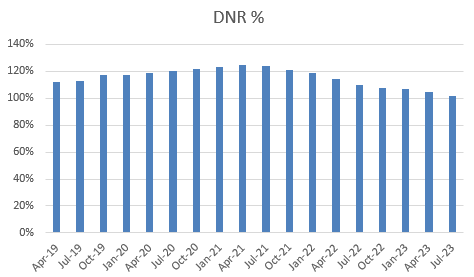

The rate of growth experienced a deceleration in the most recent quarter, as evidenced by the growth of 10.5% in revenue. Total gross margins expanded 60bps to 82.3%, and adjusted operating margin came in at 24.7%. As a result, the adjusted EPS amounted to $0.72. FCF also experienced a notable increase, rising from $78.2 million to $183.6 million. In my viewpoint, the financial results of 2Q24 serve to reinforce the notion that DOCU is unlikely to experience any notable increase in growth in the near future. In particular, important indicators like dollar net retention, total customer additions, and customer additions with an ACV of more than $300,000 all continue to show persistent sluggishness as a result of enduring macro headwinds. During the most recent call, the management also conveyed that the macro environment is exerting a restraining influence on expansion rates, as companies are carefully evaluating their investments. They also observed a certain degree of customer turnover within its customer base.

Author’s valuation model Author’s valuation model Author’s valuation model

Therefore, I hold a pessimistic outlook regarding the potential for accelerated growth in the short term. Nevertheless, it should be noted that DOCU is not entering a state of perpetual decline. DOCU is still the golden standard in terms of contract lifecycle management [CLM]. In anticipation of an economic upturn, it is anticipated that DOCU will experience enhanced business performance, particularly due to its ongoing investments in various improvements. For example, DOCU introduced a range of new product features that incorporate artificial intelligence. These include Liveness Detection for ID Verification, which has resulted in a significant reduction in signing time by approximately 60%. Additionally, the integration of Monitor Integration enables users to have up-to-date information on agreements and processes in real-time. Furthermore, the implementation of Enhanced Comments allows users to post comments instantly. Although it is difficult to measure the exact impact of each solution, the overall progress in enhancing the value proposition of the DOCU product can be seen as a positive indicator of improvement. Significantly, the management has conveyed that it is currently generating revenue from artificial intelligence through its CLM+ products, as well as indirectly through the utilization of products like search. Which means these new innovations are gaining traction (i.e., attachment rates) that should improve ARPU over time.

While I applaud management’s efforts to enhance the product, I will only put money into the company once I am confident that it can regain its previous double-digit growth rate and stabilize its most important metrics for customers.

Valuation and risk

Author’s valuation model

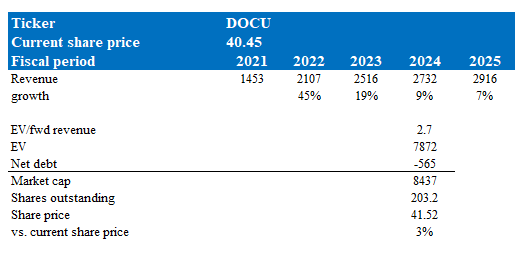

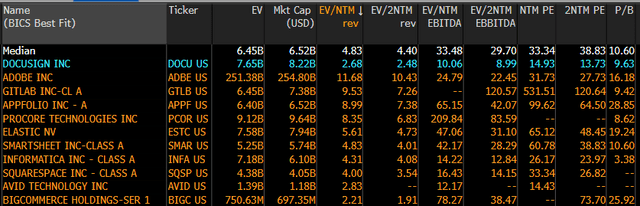

According to my model, my price target for DOCU is $41.5 in FY24. As such, I believe the stock is fairly valued in the near term. This target price is based on my forecast of growth deceleration over the near term as the macroeconomic environment remains uncertain and DOCU growth has been decelerating over the past few quarters. While growth might return in the medium term, I believe the market is focusing on the short term. Because of the weak growth profile, I expect DOCU to continue trading at a discount to other high-growth software peers that are trading at ~5x EV/fwd revenue on average, whereas DOCU is trading at 2.7x.

Bloomberg Bloomberg

Risk

One key risk to DOCU is the competition from Adobe, which is pushing out its signature module. As most documents use the PDF format, it puts Adobe in a very good position to compete against DOCU. The competitive advantage that DOCU has now – being the best standard for CLM – might be impaired if Adobe manages to gain significant traction.

Summary

DOCU currently faces a weak growth trajectory, and I recommend a hold rating in light of the challenging macroeconomic conditions. The recent financial metrics align with this view, as DOCU experienced slower growth, particularly reflected in its 10.5% revenue increase. Despite favorable indicators like margin expansion and adjusted EPS of $0.72, persistent sluggishness in key areas such as customer additions and dollar net retention suggests limited growth prospects. Management acknowledges that the macroeconomic environment is constraining expansion rates, with companies cautious about investments and some customer turnover within DOCU’s client base.

Nonetheless, it’s crucial to recognize that DOCU’s situation is not one of perpetual decline. As the economy improves, the company’s ongoing investments in product enhancements, including AI-based features and CLM+ products, offer hope for a turnaround. In conclusion, I’m cautious in the short term, waiting for signs of renewed growth and stabilization of vital customer metrics before considering investment.

Read the full article here