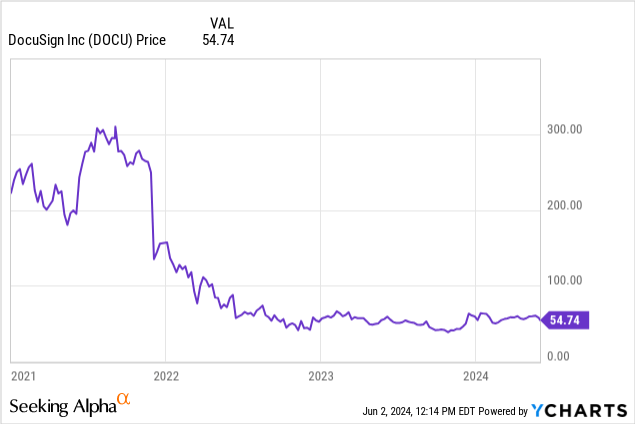

I last covered DocuSign (NASDAQ:DOCU) in February 2021 with a buy position because of the attractiveness of its electronic signature products in containing the spread of the COVID-19 virus in a world dominated by paper. It rose by about 20% to above $300 but subsequently slid to less than $55.

To shine again, it has positioned itself in the agreement management space using the AI differentiator, but the announcement on April 11 failed to instill investor confidence contrarily to other tech names that have invested in innovation.

Against such a backdrop, this thesis aims to show that this is more of a Hold until the management quantifies an AI pipeline during the forthcoming first quarter fiscal 2025 (FQ1’25) earnings call around June 6. Updates are also needed on profitability, the free cash flow margins likely to be impacted by higher capital costs, and revenue growth where product demand has declined.

Product Attractiveness Has Faded

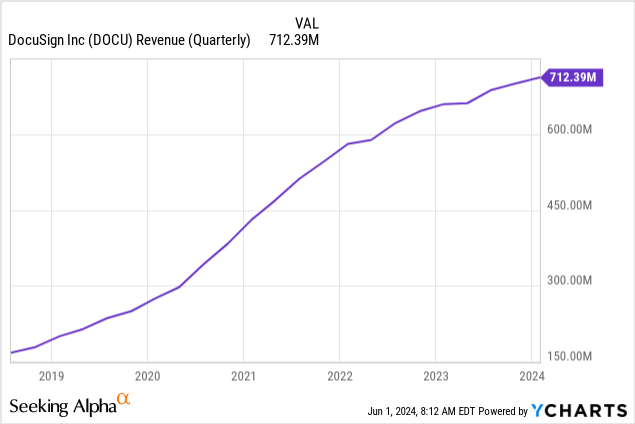

Founded in 2003 and headquartered in San Francisco, DocuSign is one of the pioneers in electronic signatures. Its products are widely used in business, for trading contracts, when signing for new employment, buying and selling real estate, etc. Moreover, 98% or $696 million out of $712 million of the company’s revenue comes from paid subscriptions in its fiscal fourth quarter of 2024 (FQ4’24), which is synonymous with stability in periods of economic distress.

Furthermore, a total of 1.5 million customers, from everyday individual users to government agencies and large businesses use the company’s technology in various industries ranging from healthcare, education, financial services, insurance, and commerce. Thus, demand for the company’s products has increased steadily as the customer base has expanded.

However, as seen in the quarterly revenue chart below, after the COVID-induced acceleration, sales have moderated as of 2022, thereby explaining the reason for the dismal price action in the introductory chart as investors instead turned towards other high-growth tech names.

Thus, after seeing peak demand for its technology during the enforcement of social distancing measures to contain the spread of the pandemic, interest eventually subsided as more workers returned to the office. Consequently, annual revenue growth plummeted from 49.2% in FY’21 to 9.8% in FY’24 resulting in an overall growth grade of C+, which is more than 200% below the IT sector median.

Increase in Billings but NRR below 100% Amid Competition

Moreover, analysts’ consensus revenue growth for FQ1’25 is 7% or a 43% drop from the 12.35% achieved one year earlier. However, looking deeper at the absolute figures, this consensus, initially $700.31 million on April 1, has been revised higher to $707.71 million on May 28.

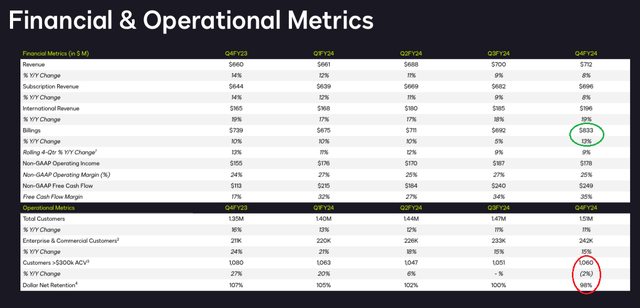

One of the reasons is billings progressed by 13% in Q4 as highlighted in green below, compared to only 5% from Q3, mainly driven by early subscription renewals which should normally have been recorded in the current fiscal year or FY’25. While early renewals augur well for FQ1’25 sales, the NRR or Net Revenue Retention (NRR) which is the percentage of sales retained from existing customers has dropped below 100% to 98% as highlighted in red below. This indicates more churn than expansion and could impact growth.

Earnings Call Presentation for FQ4’25 (s22.q4cdn.com)

Moreover, this remains a tough macro environment given that interest rates are above 5% while the Fed has not subdued inflation, which remains above 3%. Thus, potential clients have most likely scrutinized investments, before switching to the competition, resulting in net churn.

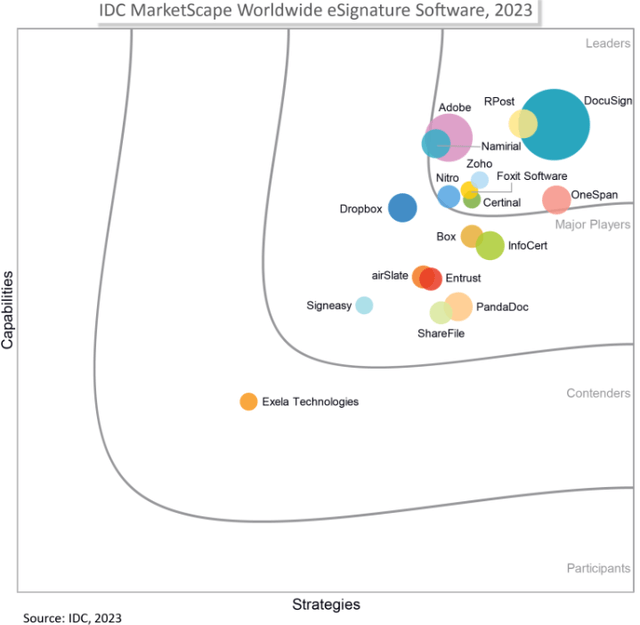

In this respect, DocuSign has a leading position in electronic Signature as pictured below, a market expected to grow at a 26.7% CAGR by 2030. However, it competes with well-known brands like Adobe (ADBE), RPost, PandaDoc, and others, as shown below. Moreover, competitors are not sitting idly and are developing new solutions in the field of electronic signatures, which implies that DocuSign has to continue spending on R&D to enhance products and marketing to drive sales. Thus, for FY’24, total operating expenses which include sales and research already consumed 78.13% of revenues, a significant percentage that also limits the amount of marketing dollars it can spend to drive product sales.

DocuSign eSignature leadership position (DocuSign)

Assessing the Profitability and FCF Margins

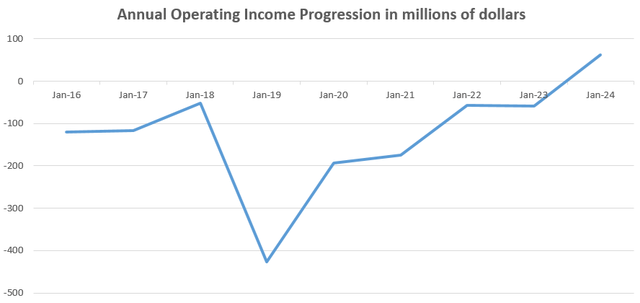

Still, significant progress was made on the profitability front with $62.7 million of operating income recorded during FY’24, which enabled it to break even as charted below. Looking ahead, analysts have upgraded its EPS expectation for FY’25 twenty-three times during the last three months versus zero downgrade, contributing to its profitability grade of A.

Chart prepared using data from (Seeking Alpha)

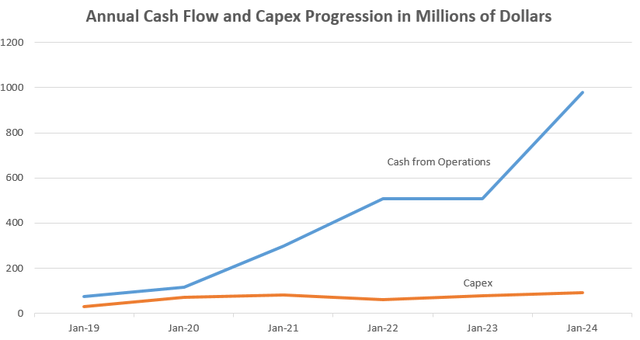

However, this grade will likely take a hit after the company acquired AI-powered contract management software vendor Lexion for $165 million on May 6 in a cash deal. This acquisition will impact free cash flow generation for a company whose capital expenses have stayed within the $72 million to $92 million range during the last four years, as shown below.

Charts were prepared using data from (Seeking Alpha)

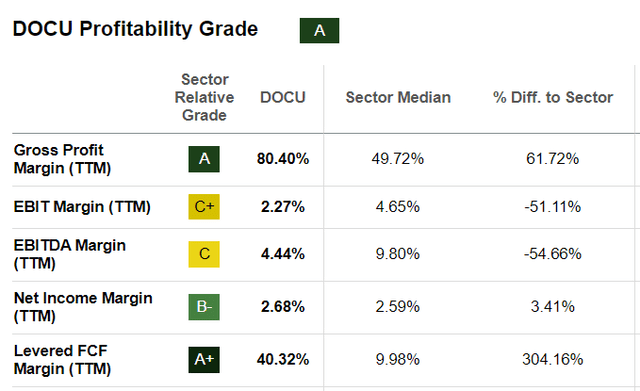

For this purpose, DocuSign’s FCF margins of 40.32% as tabled below exceed the median for the IT sector by more than 300% in sharp contrast to its EBIT margin is below the IT sector median by 51%. Thus, it is the FCF margin that weighs more in its profitability grade of A.

Seeking Alpha

Therefore, the 165 million dollar acquisition, by increasing the capex will have an impact on FCF margins, unless DocuSign can improve revenues fast enough. This will, in turn, depend on Lexion’s sales.

Also, integration of Lexion’s products into DocuSign’s platform may result in additional man-hours of software development and application migration, leading to higher costs of sales and in turn impacting its gross margins of 80%. Along the same lines, in case Lexion is loss-making, this may impact operating margins, especially for a company that has just broken even.

Clarifications are needed because of the Risks

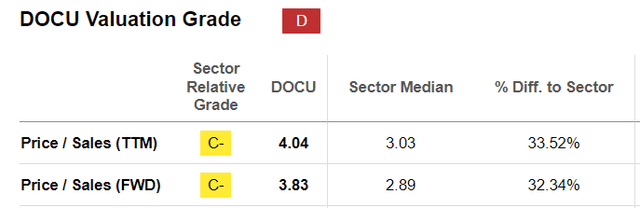

This is why, despite the margin expansion and improvement expectations, it is not the time to invest. Also, both the trailing and forward price-to-sales multiples are overpriced relative to the sector, despite sliding by more than 70% during the last three years. Its P/S still exceeds the IT median by over 30% implying this is no opportunity.

Seeking Alpha

On the contrary, the stock could fall in case there is a further deterioration in NRR from the 98% I mentioned earlier while at the same time, billings could see “less spillover” in FQ1’25 since the fourth quarter saw some advanced renewals. In this respect, since DocuSign does not have the global scale of Adobe, it is important to assess the progress made in the channel partner ecosystem which includes SAP SE (SAP), Microsoft (MSFT), and Deloitte. Noteworthily, these partners enabled the company to bag its first $1 million customer contract last fiscal year.

Second, regarding profits, it is important to follow up on the “efficiencies and improvements in G&A” expected for FY’25 together with the cost management efforts undertaken since the beginning of this calendar year. One example is how the company drives the adoption of its CLM (contract lifecycle management) products for managing complex workflows. These have seen traction from its enterprise customers, but still constitute a small share of the overall business. In this case, upselling to the existing client base numbering 1.5 million is preferable, as it would entail spending relatively few marketing dollars compared to luring new customers to buy the product.

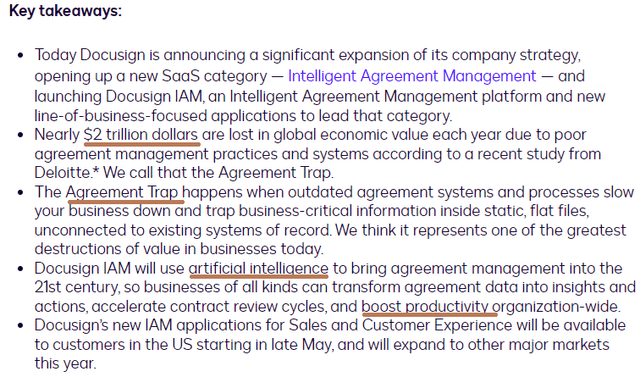

Thus, unless progress is made, analysts could revise consensus estimates lower, resulting in volatility and the stock could fall to the $50 level as in February this year. This could constitute an opportunity to buy, depending on the way it positions its new SaaS business, Intelligent Agreement Management, launched on April 11 generating sales rapidly.

Highlighting IAM Opportunities

Talking opportunities, about $2 trillion are lost in global economic value annually because of poor agreement management practices and related systems according to Deloitte as shown below, meaning there are opportunities for solution providers. Moreover, IAM forms part of the legal AI software market, expected to reach around $19.3 billion by 2033, after accelerating at a CAGR of 29.1% from 2024. It entails using innovative technologies to bring automation to tasks such as contract analysis, legal research, due diligence, document review, and enhancing various legal processes for attorneys and other legal professionals wanting to close deals faster, helping in efficiency and cost-effectiveness.

Intelligent Agreement Management (DocuSign)

However, given the hype around everything which includes the word “AI”, it is crucial for the management to come up with a dollar pipeline or at least a TAM (total addressable market). To this end, the IAM portfolio should have been available in the U.S. as of the end of last month, with expansion to other major markets planned for later this year.

In conclusion, this thesis has painted a rather mixed picture or one where growth has remained on the low side, but revisions have been upgraded. Also, profitability-wise, DocuSign managed to break even, but, it is important to ascertain whether this can be sustained. In the same vein, the FCF margins should drop unless Lexion generates operational cash flow. However, there are opportunities, and if DocuSign just manages to capture 1% of the $19.3 billion legal AI software market, this would represent $193 million of revenues and divided by $2.76 billion (or FY’24 sales) could yield a 7% increase. Added to the 7% revenue growth expected for FQ1’25, this could result in double-digit growth.

Read the full article here