As the US economy continues to show signs of lackluster long-term growth, investors are interested in those stocks with “defensive” potential. Traditionally, these companies see greater demand during more challenging economic periods, with “discount” stores like Dollar General (NYSE:DG) being popular. During most previous recessions, most “defensive” stocks have outperformed the market as their sales and earnings rose as people shifted buying habits toward cheaper stores. However, as seen in DG’s ~32% decline this year, Dollar General and its peers may no longer offer the defense, as many investors believe. Indeed, given DG’s high valuation, a sustained decline in its sales or earnings could cause the stock to decline tremendously as it loses its significant “defense premium.”

Not Your Father’s Consumer Economy

There are numerous fundamental differences between the modern consumer economy and that which persisted from ~1980 to ~2012 (the Great Moderation period). Most investors are highly conditioned by the environment which existed during that period but does not exist today. During those decades, companies could expect most producer input prices (mainly imported goods such as those sold by DG) to inflate much slower than consumer prices. For example, average US apparel prices were constant from 1990 to 2020 despite a ~150% increase in average total consumer prices. This was due to a significant increase in offshore factory and productivity expansion (in China and India particularly) over that period, as well as improvement in trade relations and a massive gap between domestic wages and those of China and India (allowing US consumers immense buying power).

Today, the east-west wage gap is not nearly as large as it used to be, transportation fuel costs are much higher, and trade relations are weaker, so companies like Dollar General, Target (TGT), Walmart (WMT), and others can no longer expect their products to have lower import costs. Accordingly, most prices for smaller imported goods (such as those sold by DG) are now rising as fast as consumer prices and faster than wages. Further, due to commodity shortages, rapidly rising wages in “BRICS” countries, and increased transportation costs (and trade relations issues), this trend will likely continue. It may accelerate over the coming years – particularly if the US dollar loses to the dominant position.

Fundamentally, the US is not struggling with low consumer demand due to cyclical changes in the credit cycle, as did during all “Great Moderation period” recessions. Instead, the US (and its Western peers) face weakened consumer demand due to prices rising faster than wages. Unless the US rapidly expands its factory production to bring production back to the US (which would likely take decades), this trend should continue indefinitely until purchasing power among US consumers reaches parity with those in “BRICs” countries. In general, workers in those BRICs countries produce far more goods than they consume (positive trade balance), while people in the US consume far more goods than produced (negative trade balance). That situation worked well for both when BRICS countries needed international demand to drive a profit that allowed factory expansion. However, now that those countries have fully grown their physical capital base, they no longer stand to benefit from the vast trade imbalance.

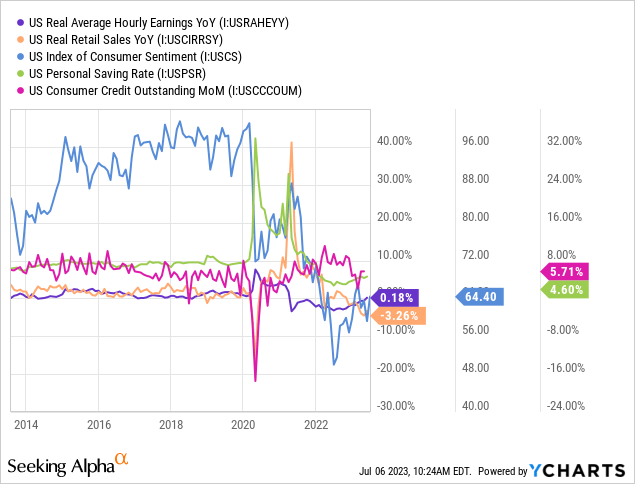

With these macroeconomic factors in mind, the US economy will likely continue to see abnormal negative trends in the retail and general consumer markets. These trends are abnormal because they are not primarily driven by a decline in bank consumer lending (i.e., higher interest rates) but a sustained and significant increase in consumer prices. As a result, real wage growth has generally been negative, savings are low, consumer sentiment is shallow, actual retail sales are falling, and consumer borrowing (credit cards) is very high. See below:

Inevitably, many people will borrow as much consumer credit as possible and need to reduce spending. This is occurring today, as evidenced by falling real retail sales and abysmal consumer sentiment. Real wages technically rose YoY; however, we must be mindful that that metric assumes the consumer price index accurately reflects price growth felt by households. The “consumer price index” has changed over time. If its calculation method were not changed since 1990, then inflation would be around 8% YoY today (and ~12% last year) (compared to 4% officially). Indeed, many people feel that prices are rising faster than 4% today. Even if that pace has slowed, it is exceptionally high by historical standards.

If inflation is actually 8%, then real retail sales and real wages would indeed be falling much faster today; further, that would mean the US economy has been in a sustained recession since 2021. While the US government’s official measures may not validate that fact, it is validated in sentiment surveys, industrial business trends, and record-high bankruptcies among small-to-midsized businesses. Many large public corporations like Dollar General have not seen as great of an impact as their smaller peers since they’ve gained business at the expense of closed “mom and pop” stores; however, in the long run, I do not believe any corporation can completely overcome the changing economic reality.

Dollar General is a “Premium” Store Today

While it may take a decade for the full effects of this change to be felt, it will continue to have huge impacts on the US (and peers’) economies and, therefore, also on financial markets. Generally, we can expect all retailers will struggle to keep retail prices up with the input prices of items, likely leading to the convergence and decline in gross margins for all retailers. In other words, Dollar General is increasingly unlikely to offer discounts to Walmart, Amazon (AMZN), and even Target for most items. Indeed, in-depth studies clearly show that Dollar General’s goods are as expensive or even more expensive than most of its peers. Dollar General does not offer discounts but typically sells smaller quantity items, making it potentially appear cheaper.

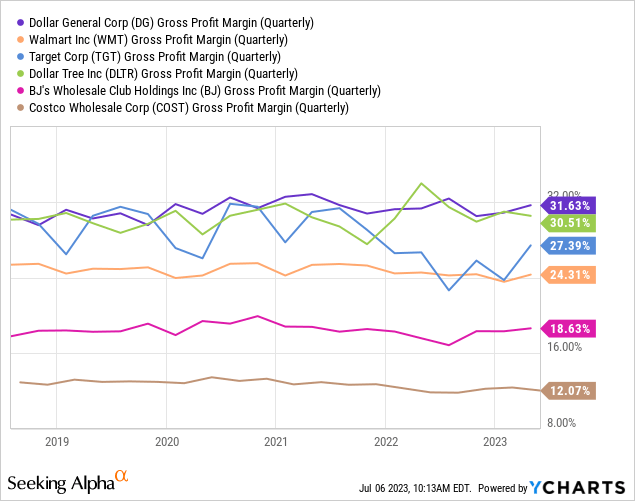

Indeed, both Dollar General and Dollar Tree (DLTR) have significantly higher gross margins than all related retailers. Further, those which sell items in bulk, like Costco (COST) and BJ’s (BJ), have much lower gross margins, implying they’re the actual “discount stores” while Dollar General is genuinely a “premium” store. See below:

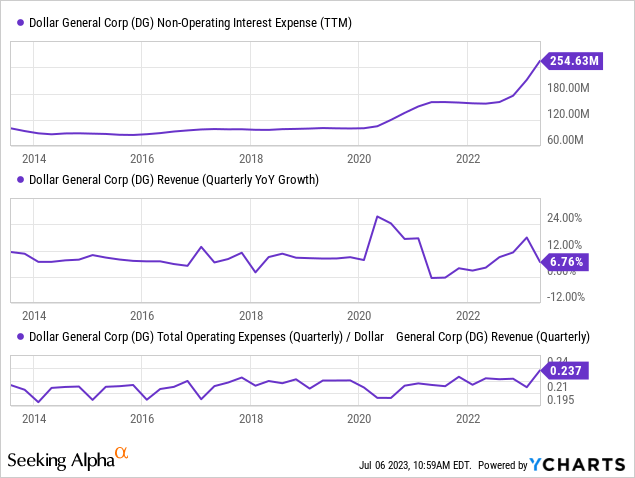

Since Dollar General and Dollar Tree have higher gross margins, they profit more per good sold than their peers. While that may seem optimistic, it is very negative in the current environment because it implies most shoppers would save by going to Walmart, a bulk goods store, or, more likely, Amazon. Even Target is technically cheaper than Dollar General on a gross profit basis. Further, due to this crucial factor, as goods import prices rise disproportionately to wages, Dollar General and Dollar Tree will likely face more significant declines in gross margins. Further, the company also sees a rapid increase in interest costs due to rising rates while its operating costs are rising faster than its sales. The company’s sales are still growing YoY but slower than inflation. Considering most retail workers’ wages are rising much faster than inflation, it is likely that DG’s OpEx will continue to grow faster than its sales, lowering its net profit margins. See below:

If we assume that DG’s OpEx-to-sales will continue to rise by ~1-2% while its gross margin declines by ~1-4% (depending on economic strength), then its net income margin may fall from ~6% today to <2% over the next year. A larger-than-expected increase in input costs or a recessionary decline in sales (considering DG is economically not a discount store) could cause its net income to fall below zero. While its interest costs remain relatively low compared to its income, the rate increase could accelerate the trend.

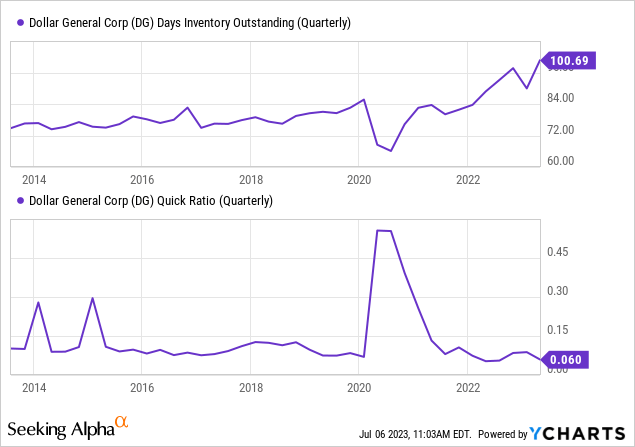

Further, DG has a relatively weak short-term balance sheet with an excessive increase in inventory levels compared to sales and a meager quick ratio. See below:

Dollar General’s quick ratio is just 0.06, meaning it has essentially no liquid assets compared to its current liabilities. That would not be a massive issue if its inventory were moving, but it is not. Instead, as Target has had to do, the company has built up a considerable inventory supply, meaning it will likely need to cut prices over the coming quarters. In my view, this situation creates a solid recipe for some financial strains as its cash flow appears likely to turn negative this year, meaning it will need to halt its dividend, raise new debt (likely at much higher interest rates), and stop buybacks. In my view, at least one of those financing avenues will likely be pursued, and if strains are large enough, all of the above may be pursued – jeopardizing the firm’s long-term potential and investor confidence in it.

The Bottom Line

To add to Dollar General’s issues, the company faces a growing crime issue. Its stores are often situated in lower-income areas with higher theft rates. Of course, since 2020, retail theft levels have risen astronomically. Since retailers generally have net margins of 0-8%, a 1-4% theft rate substantially negatively impacts their bottom line. Indeed, this is a significant reason for Dollar General’s poor Q1 report and outlook, as it faced a disproportionate rise in theft rates. The company cannot increase prices to offset theft or else lose sales, as that would make it even less competitive to Amazon and lower-theft stores.

Additionally, since more Dollar General stores are being robbed at gunpoint, the company faces many potential labor-related legal issues. That issue is a direct legal risk factor for the firm and should also increase labor shortage issues as workers demand higher wages to account for increased risk. Eventually, due to the growing theft issue (partly caused by rising import prices), the company will likely close many more of its stores.

Overall, I believe Dollar General is worse than other retailers on virtually all fronts. If the recession worsens, I expect the company will see an even more considerable increase in thefts, a more significant drop in sales (since Amazon and Walmart are cheaper), and higher interest costs. Even without a recession, the firm’s margins will likely face strain due to rising goods costs and worker wages compared to sales, particularly considering its huge inventory level. In my view, the company will likely see a complete loss of EPS this year that could be sustained for years as it reorganizes to account for the changing economic and social structure (“social” being primarily rising theft levels).

Is DG a Short Opportunity?

DG’s valuation is typical of its sector, although its dividend is much lower at 1.3% compared to the sector average of 2.5%. However, although its ~17% “P/E” ratio is near the sector average, I believe it is pretty high in light of the company’s significant potential to experience an extensive and prolonged decline in its EPS. Personally, I would not buy DG at a TTM “P/E” over 8X, considering I expect its EPS could fall by over 50% this year and likely remain near those depressed levels over the long run as it faces economic strains and closes stores. Accordingly, my price target for DG is ~$85.

Considering very few investors and analysts appear to be aware of DG’s current strains and lack of defensive potential, I believe it is a solid short opportunity. Its short interest is just ~1.5%, and it has low borrowing costs, so it is certainly not a crowded short trade as are many others today. Despite its volatility, DG’s implied volatility is much lower than last month, so put options on the stock are likely trading at a discount, making them a solid potential way to bet against DG with defined risk. On a technical basis, DG is near its new apparent resistance level of ~$175 today, giving it potentially good short timing. Overall, I am very bearish on DG and believe it will lose more value than Target and others over the coming year.

Read the full article here