Dollar Tree (NASDAQ:DLTR) and other discount retailers have been taking a massive hit lately. Dollar Tree has been the latest victim, falling around 25% after posting a bad earnings report and weakening guidance.

But before jumping on the bandwagon of bad news, let’s take an objective look at this company and try to understand if it’s really in long-term trouble and what its real value is.

Fundamentals Based On Facts

- Dollar Tree is currently trading around $63.50.

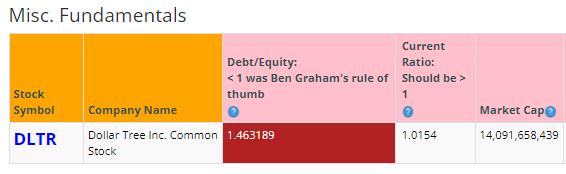

- The debt-to-equity is slightly concerning at 1.42, but nothing to seriously worry about.

- The current ratio is fine at 1.28, which means that the company has enough cash to cover short-term liabilities.

- The book value to share was $33.83 in July 2024.

- DLTR is now at a 52-week low.

- Yahoo Finance estimates that the one-year estimated target is around $132.

On the surface, it seems that Dollar Tree has a decent balance sheet and could be selling at a bargain price with a great deal of upside potential.

Why is Dollar Tree stock falling?

Believe it or not, DLTR is not only selling at a 52-week low, but it is also near a 5-year low!

A variety of reasons have been contributing to the poor performance of the recent 2nd quarter earnings report.

Here are some of the reasons:

- Customers are facing increased economic pressures.

- More customers are shopping at Dollar Tree stores, but the average sale per customer has actually decreased 0.5%.

- There is an increasingly challenging macro environment.

- Dollar Tree’s main customers tend to be in the lower-income earning category, and these are the very customers who have felt the most financial squeeze because of inflation and higher interest rates.

- The fall of Dollar Tree has also been perpetuated by the continued falling of other discount retailers, such as Big Lots (BIG) and Dollar General (DG).

On the flip side, here is some potentially positive news about DLTR:

During the past quarter, 127 new Dollar Tree stores were opened, along with 28 Family Dollar stores. Around 1,600 Dollar Tree stores that were converted to multi-price format saw sales growth of 4.6% in the second quarter.

“As part of its portfolio optimization review, Dollar Tree planned to close approx. 600 stores in the first half of 2024. By the end of Q2, the company had closed 655 stores, and it plans to close another 45 stores during the back half of the year.”

Part of the reason for Dollar Tree’s lower expected earnings can be attributed to its conversion costs of newly acquired 99 Cents Only stores.

In the long term, I feel that Dollar Tree is positioning itself well and acquiring more market share while reducing its competition. They have taken over Family Dollar stores already and have eliminated that competition. Now, they have even less competition with 99 Cents Only stores gone.

Basically, I only see Dollar General as Dollar Tree’s main competition that remains. Some will say that Walmart is also their competitor, but I feel that Dollar General is the main and direct competition. I feel that when most budget-minded consumers want to just run into a small store fast and grab a few cheap items, they will choose Dollar Tree or Dollar General. On the other hand, if they are wanting to do their main grocery shopping or have the time to do more extensive shopping for more items or higher priced items, they will likely choose Walmart.

It’s two different types of shopping, so I don’t see Walmart as the main competitor.

Dollar Tree accounts for roughly 26% or a quarter of all US Dollar & Variety Store revenue. Dollar General accounts for about 36%, but Dollar Tree continues to increase its market share. This makes me feel more confident about the long-term investment of Dollar Tree.

What’s Dollar Tree Stock Worth?

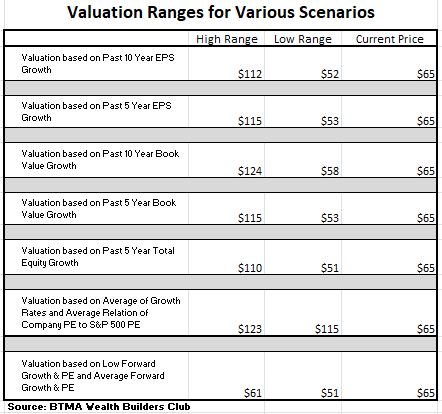

For more detailed valuation purposes, I will be using a conservative newly forecasted guidance EPS of 5.20. I’ve used various past averages of growth rates and PE Ratios to calculate different scenarios of valuation ranges from low to average values. The valuations compare growth rates of EPS, Book Value, and Total Equity.

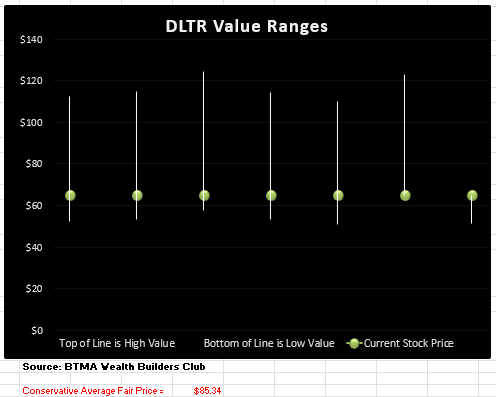

In the table below, you can see the different scenarios, and in the chart, you will see vertical valuation lines that correspond to the table valuation ranges. The dots on the lines represent the current stock price. If the dot is towards the bottom of the valuation range, this would indicate that the stock is undervalued. If the dot is near the top of the valuation line, this would show an overvalued stock.

BTMA Wealth Builders Club

BTMA Wealth Builders Club

(Source: BTMA Wealth Builders Club )

This analysis shows an average valuation of around $85 per share versus its current price of about $65, this would indicate that Dollar Tree is undervalued.

Summarizing the Fundamentals

Dollar Tree has better than average fundamentals. Its past ten years EPS has been steadily increasing overall with an outlier COVID year in 2019 when the EPS significantly dipped.

ROE (Return on Equity) has remained solid and at sufficient levels for the past 5 years (5-year average of 17.7).

ROIC (Return on Invested Capital) is less than I would like, but it has been steadily climbing over the past 5 years (5-year average of 8.3).

Gross Margin Percent is also a bit less than I want to see, but it has been steadily increasing over the past 5 years (5-year average of 30.3).

The balance sheet is in check with a reasonable amount of debt-to-equity and an excess amount of cash to cover short-term liabilities.

BTMA Stock Analyzer

Source: BTMA Stock Analyzer (Misc Fundamentals)

Dollar Tree Vs. The S&P 500

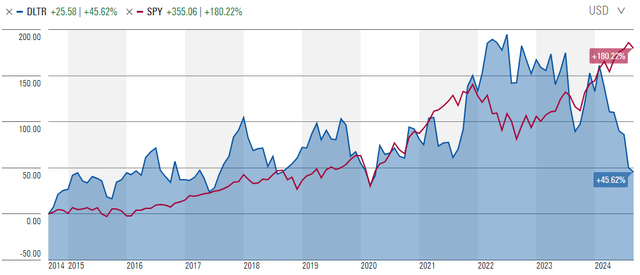

Now, let’s see how Dollar Tree compares versus the US stock market benchmark S&P 500 over the past 10 years. From the chart below, Dollar Tree has performed in a similar upward trend over the past decade. However, Dollar Tree is much more volatile. This is good and bad. For an impatient investor, it can be stressful to watch your unrealized gain swing up and down so much. But this is the nature of a single company in the more volatile discount retail store industry when compared with a much more diversified index fund like the S&P 500.

The main takeaway here is that Dollar Tree has grown overall with an upward movement and has many times outperformed the S&P 500. Whereas, it has more rarely underperformed against the S&P 500. Now is a point when the stock is temporarily priced so low, that it could be an ideal time to buy at a bargain price to experience greater gain potential.

Morningstar

Forward-Looking Conclusion

Over the next five years, the analysts that follow this company are expecting it to grow earnings at an average annual rate of 14.96%.

In addition, the average one-year price target for this stock is $132.78, which is about a 107% increase in a year.

The Expected Annual Compounding Rate of Return is 10.41%.

BTMA Stock Analyzer

Source: BTMA Stock Analyzer (Stock Value)

It is certain that Dollar Tree, along with other discount retailers, are feeling extreme pressures. Inflationary pressures mean that customers’ dollars are worth less and customers can’t afford to spend as much.

Dollar Tree has some individual issues with underperforming Family Dollar Stores and 99 Cents Only Stores that will need to go through their optimization process. But in the long run, I feel that Dollar Tree is acquiring stores and opening new stores to increase their market share and to reduce their competition. As inflationary and macroeconomic pressures ease, Dollar Tree should be able to capitalize on their solid position in the Discount & Variety Store Industry.

I just picked up more shares of Dollar Tree after its second quarter earnings fall, as I am confident in the company and that it is currently selling at a bargain price.

Read the full article here