By Brian Nelson, CFA

Let’s first get this out of the way: We think dividend growth investing and income investing can make a lot of sense for a lot of investors. We’re not against these strategies in any way. In fact, we produce newsletters focusing on these two strategies. However, a myopic focus on the dividend or the dividend yield could lead investors astray. A free-cash-flow backed dividend, itself, is but a symptom of a company’s ability to generate value for shareholders; it is not the driver behind value-creation and the sustainability and growth of a company’s share price. A company’s ability to continue to generate free cash flow for shareholders in excess of cash dividends paid is in part one of the key drivers behind why stocks advance over time.

One of the best videos to watch to learn about dividends is one covering the concept of the free dividends fallacy. But what is the free dividends fallacy? For one, it simply states that the dividend is not independent of the stock price. When a company pays a dividend, its share price is reduced by the amount of the dividend on the ex-dividend date. What this means is that the dividend is capital appreciation that otherwise would have been achieved had the dividend not been paid. Chicago Booth’s Samuel Hartzmark explains that if one hypothetically had a stock that was priced at $10 per share, and it paid a dividend, one now has a stock that is priced at $9 per share, while shareholders have a $1 in dividends. They don’t have a $10 stock and a $1 in dividends.

What matters most to investors and most retirees should be total return as they can sell off a portion of their investment portfolio to generate income, in somewhat of a similar way that a dividend payment reduces the capital one has in any dividend-paying position relative to the scenario if the dividend had not been paid. That said, receiving dividends is an easy way to structure income payments, but investors should not let the ‘dividend’ tail wag the ‘total return’ dog when it comes to retirement. Stock selection matters. Total return is in part a function of a company’s net cash on the balance sheet and future expectations of enterprise free cash flows (and changes in them). When a company pays a dividend, for example, the net cash on the company’s balance sheet is reduced or the net debt is increased, resulting in a reduction to the firm’s intrinsic value and therefore its stock price. The intrinsic value of a company is calculated as the sum of net cash on the balance sheet and the present value of future enterprise free cash flows.

Total return, again, is independent of the dividend payment. Many investors believe that total return is driven by the sum of capital appreciation and dividend yield. When it comes to the drivers of total return, this is not true. Total return is driven in part by the cash-based sources of intrinsic value: a company’s net cash position and changes in future expectations of enterprise free cash flows. As these expectations change over time, so does the stock price and return. The problem with believing that the dividend yield is a driver behind total return, however, is that many then start to believe that if a company increases its dividend (or has a high yield), then it will increase its total return (or lead to a better total return), too. Unfortunately, this is not the case. The total return of the stock is independent of the dividend yield, meaning investors would get the total return of the company whether the company has a dividend yield or not.

That said, let’s use a hypothetical example to explain how dividends could actually hurt investors’ wealth over time. Let’s say a company priced at $10 generates annual free cash flow of $0.50 per share and pays out $1 in annual dividends over a one-year period. Many retirees might be excited to find that this hypothetical company has a 10% dividend yield (it pays a $1 per share in dividends and is priced at $10 per share). However, as cash is accumulated from free cash flow and then distributed as a dividend from the balance sheet, over time the intrinsic value (and the share price) of this company erodes. After one year of generating free cash flow and paying dividends, for example, this hypothetical company would then be priced at $9.50 per share ($10 price + $0.50 in free cash flow – $1 in dividends). A retiree that lives off dividends might be happy about receiving the dividend, but their wealth is actually falling (as they spend that dividend on all the desires that retirement may bring).

The yield trap then begins. If the company keeps its dividend the same at $1 per share and still generates $0.50 in free cash flow the next year, the dividend yield on this company would then be ~10.5%, with its price now at $9.50 per share ($1 in dividends divided by $9.50 per share). For income-oriented investors, they may view this higher yield as even more attractive. After all, ~10.5% is better than 10%, so this company is a better-yielding idea and generates more income with any incrementally new dollar invested (should investors dollar cost average into the equity). However, if the firm keeps generating free cash flow less than the dividends it pays out, its share price would keep falling and its yield may keep moving higher as a result. Through all of this, retirees may be receiving an income stream (for some time), but their wealth would actually be eroding, as most retirees may be spending those dividends to pay for living expenses in retirement.

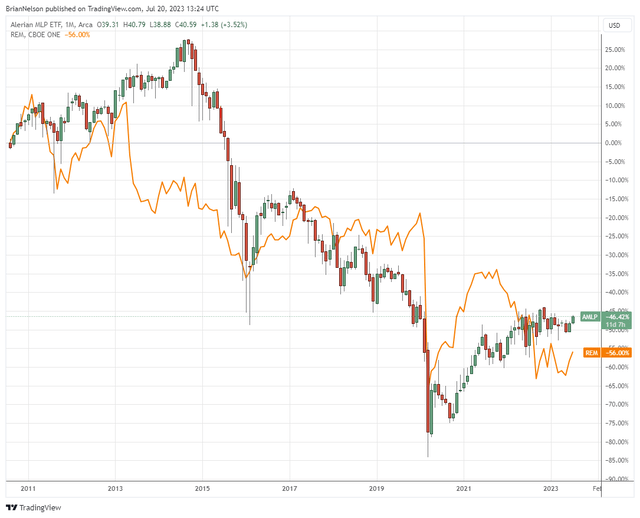

Energy master limited partnerships and mortgage REITs have destroyed the accounts of retirees, necessitating them to chase higher and higher yields as their capital positions have eroded. (Trading View)

Over a long-enough time horizon, the result then could become a heavily depressed stock price and a dividend yield that eventually doesn’t make much sense relative to other yields on the market, and one that is not supported by the free cash flow stream of the company, itself. The company then may decide to cut the dividend payout to match comparable yields on the marketplace, and retirees would then be left with a lower income stream (a lower dividend) and a lower stock price (a lower capital position). Now, with the lower dividend and lower stock price, the cycle may begin again with the company paying out more than its free cash flow again, and its stock price falling with its yield increasing–until, of course, the firm is finally able to generate free cash flow in excess of the dividends it pays such that the income stream and stock price can be supported by organic means. Though the example in this article is hypothetical and simple in nature, the reasoning behind this thinking is sound and may explain in part what we’ve witnessed across the ultra-high yield arena over the past decade.

Let’s now get into one of the primary drivers behind total return: future expectations of free cash flow (and changes in them). First, what is free cash flow? Traditional free cash flow is calculated from a company’s cash flow statement by subtracting a firm’s capital expenditures (additions to property, plant, and equipment, PP&E) from cash flow from operations (operating cash flow). Though some investors may make adjustments to this measure of traditional free cash flow, backing out sales of PP&E and perhaps ignoring the add back of stock-based comp in operating cash flow, the substance of the measure remains. It is what the company generates for shareholders after plowing capital back into the business to continue to maintain and grow operating cash flow. We like to calculate free cash flow as cash flow from operations less all capital spending (not just maintenance capital spending), as growth capital spending is used to propel future operating cash flow, which itself, is used in traditional free cash flow calculations. Balance is important, in this regard.

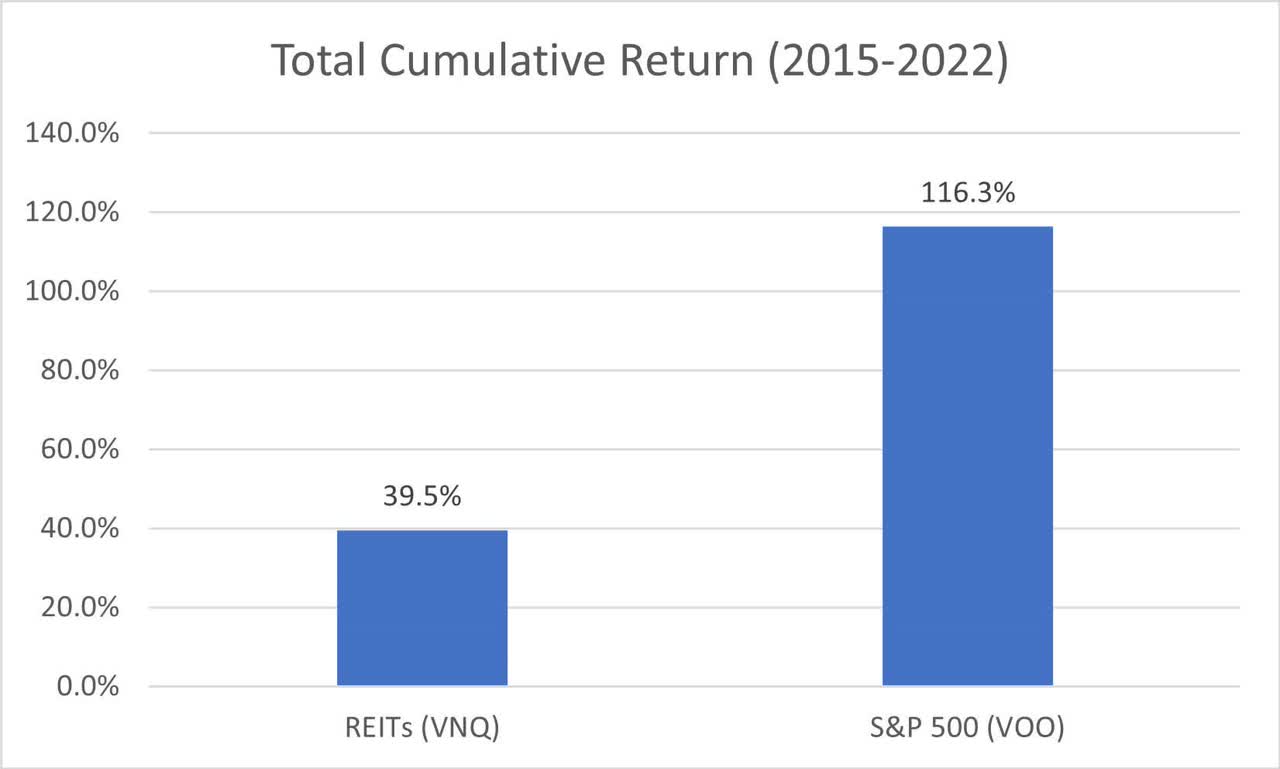

Once a measure of free cash flow is calculated, it can be compared to a firm’s cash dividends paid, which is found in the cash flow from financing section of the firm’s cash flow statement. If free cash flow is consistently less than cash dividends paid, then the company can be considered capital-market dependent, meaning it must continuously raise new capital, whether through the debt or equity markets, in order to support not only the dividend, but also indirectly its stock price (intrinsic value). Entities like these have historically been found in the master limited partnership (AMLP) arena and across many REITs (VNQ), though the former group is doing a much better job of covering cash distributions paid with free cash flow these days than they did a decade ago. With the Fed’s rate-hiking cycle continuing, the cost of capital for capital-market dependent entities continues to increase, too, and their operations continue to be squeezed. REIT returns, for example, just haven’t been great in a long time.

REITs have not performed as well as one might have thought. (Vanguard)

All else equal, if a company is not covering its dividend payments with free cash flow, and assuming of course retirees are spending those dividend checks, retirees are then destroying their wealth one dividend at a time. Many capital-market dependent entities may continue to have access to the capital markets to support the dividend and indirectly their stock price, but at some point the music eventually stops, and the firm either has to issue new debt or new equity at very expensive prices at the worst possible time, which inevitably would hurt its intrinsic value (share price)–or it may have to cut the dividend or distribution, or both. This is why high yield investing relies so much on assessing the credit health or credit rating of a company. If a capital-market dependent company can issue new debt or equity, its share price and dividend/distribution may be okay. If it can’t, well, then there might be serious trouble ahead.

We don’t think this is a game that many retirees should be playing, especially as a major financial crisis tends to happen more frequently than one otherwise would prefer. Instead, we implore retirees to do their homework, comparing a company’s free cash flow with its cash dividends paid to assess the long-term sustainability of the dividend and the risk to potential wealth destruction over time. Many retirees may already be caught in a yield trap that we described in the hypothetical example in this article, reinvesting more and more of their capital into entities that do not necessarily have sustainable and free-cash-flow supported dividend payouts. Though we have used some jargon in this article, especially with respect to references on the cash flow statement, steering clear of capital-market dependent high yield “land mines” with unsustainable dividend payouts may serve the longevity of one’s retirement portfolio well. It’s certainly not an ideal situation to have one’s retirement portfolio constantly eroding over time.

What’s the fix? Well, quite simply, a focus on the discounted cash-flow framework, or enterprise valuation, is key. Ask oneself: How much does this company have in net cash (total cash less total debt on the balance sheet)? How much does this company generate in free cash flow (cash flow from operations less all capital spending)? Does free cash flow consistently cover cash dividends paid? If it doesn’t, then the company is capital-market dependent, and retirees may be taking on credit risks that they may not be aware of in owning these types of equities. Unfortunately, almost all high-yielding equities with yields north of 8%, 10% or more suffer to some degree from the dynamic of capital-market dependence risk. Always trust your common sense, too. In a world where risk-free-rates are half of that of a high yielder, is the market really that inefficient, or is the investor just taking on significantly more risk. High yield investing is synonymous with high risk investing. Just because a company pays a dividend does not make it “safer” than a non-dividend payer. It could be far riskier.

What are some companies that we like for total return potential? Well, we’re huge fans of companies with net cash on the balance sheet and strong future expectations of free cash flow (and growth in them). These types of entities tend to have asymmetric risk/reward scenarios as they lack meaningful bankruptcy risk and capital-market dependence risk, while they have the prospect for ever-increasing expectations of future free cash flow, the latter a key driver in part behind why stock prices advance over time (accumulated net cash on the balance sheet is also another key driver). We’re huge fans of the cash-based sources of intrinsic value, and we outline three of our favorite names in this article.

Read the full article here