Dow Inc. (NYSE:DOW) is a company that produces various chemicals, plastics, and synthetic fibers. The company emerged from a merger in 2019 and is a major player in the chemicals industry. Dow is dedicated to spearheading the path toward a sustainable energy future and has global reach throughout 31 different countries alongside 104 manufacturing sites. The company plays a pivotal role in curbing energy consumption because their portfolio includes products like solar and wind power technologies, building insulation applications, lightweight vehicle adhesives, and water treatment solutions.

DOW Proxy

Despite the lowered industry demand, DOW’s current price is appealing because of its cost advantage, a high dividend yield that is covered by cash flow, diverse product and service portfolio, classified as a “Dog Of The Dow” which has historically been a great investing strategy, and it is currently undervalued with big upside potential.

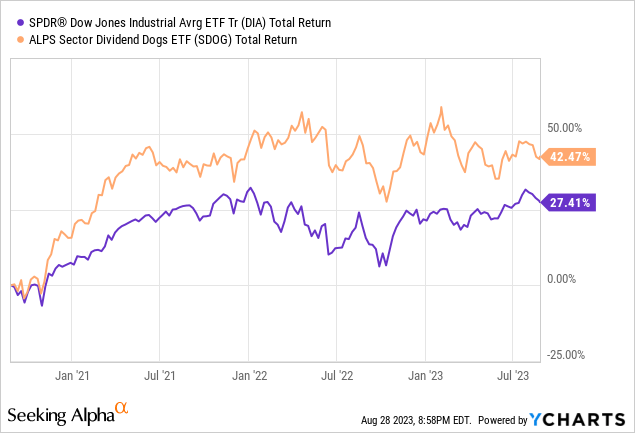

Dog Of The Dow

DOW was classified as a dog of the Dow Jones in early 2023. The Dogs Of The Dow investment strategy entails purchasing the top 10 highest-yielding stocks from the 30 stocks within the Dow Jones Industrial Average. While it might appear simplistic, the Dogs of the Dow strategy has delivered an average annual return of 8.7% since 2000 in comparison to the Dow Jones’ 7% annual average return. Although the ALPS Sector Dividend Dogs ETF (SDOG) doesn’t have history dating back to 2000, we can see an example of the Dog’s outperformance here below.

I wouldn’t solely base an investment decision on a “strategy” but I do think it’s something neat and unique to mention here. I always was quite fond of tracking these kinds of metrics.

Partnership & Sustainability

DOW Investor Presentation

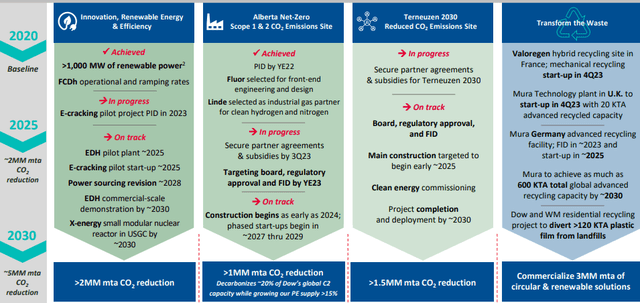

By 2025, DOW make significant progress on CO2 reduction which is planned to be accomplished through an E-cracking pilot. “Cracking” is an advanced technology that can be utilized to reduce CO2 emissions overall.

Steam cracking is a process in which saturated hydrocarbon feedstocks such as liquefied petroleum gas (LPG) or butane are broken down into smaller hydrocarbons like ethylene and propylene. These in turn are then used in the manufacture of a wide variety of products from fabricated plastics, antifreeze and alcohol, to surface coatings, and adhesives. – The Chemical Engineer

Nevertheless, this energy-intensive procedure generates a substantial volume of CO2 emissions. To stay committed to their sustainability goals, Dow is cooperating with Shell (SHEL) to introduce a new concept: replacing conventional heating methods in steam cracker furnaces with renewable electricity. DOW is making great strides towards achieving these sustainability metrics as according to their timeline, they are in progress and on track with these goals that will significantly reduce CO2 emissions. I feel that this is noteworthy because through these initiatives, DOW anticipates an earnings growth exceeding $3 billion annually, alongside a projected reduction of approximately 30% in CO2 emissions by 2030.

Strong Cash Management Despite Macro Challenges

DOW’s success is linked to its ability to produce chemicals more affordably in North America by using low-cost natural gas-based materials. This advantage could lessen if natural gas prices rise, driven by global demand and shifts to renewable energy. DOW’s CEO had the following statement at the most recent earnings call:

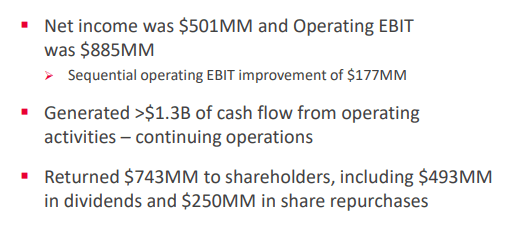

Team Dow delivered sequential earnings improvement and generated operating cash flow of more than $1.3 billion in the second quarter. We proactively navigated the challenging near-term macro environment by implementing our targeted cost savings actions while capitalizing on our advantaged feedstock position and participation in attractive end markets. – Jim Fitterling, CEO

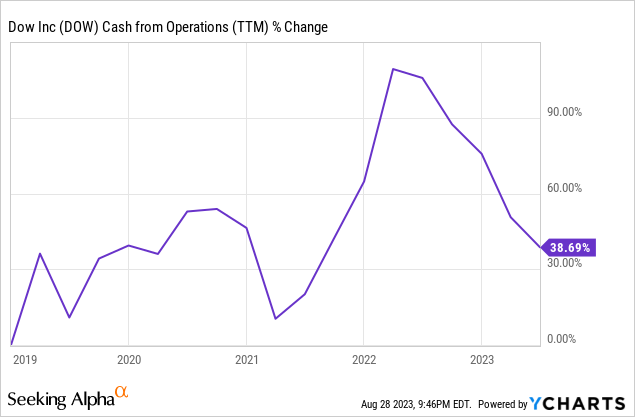

Taking a look at DOW’s cash from operations does confirm that they are treading in the right direction here. We can see that cash from operations has grown at an average of 9.5% per year. this is pretty healthy considering the macro challenges such as local price decreases and lowered global energy costs that DOW is currently experiencing. This is reassuring because it generally means that when market conditions align for DOW, we can expect a much higher level of profitability in the future. Confirmation of these conditions were stated in the latest earnings press release:

Packaging & Specialty Plastics segment net sales in the quarter were $5.9 billion, down 28% versus the year-ago period. Local price decreased 21% year-over-year due to lower ethylene and polyethylene prices across all regions driven by lower global energy and feedstock costs. Volume declined 7% year-over-year, primarily in EMEAI, driven by lower demand for olefins and aromatics. On a sequential basis, net sales decreased by 3%, as volume gains in Asia Pacific and Latin America were more than offset by lower third-party energy sales – Jim Fitterling, CEO

DOW Investor Presentation

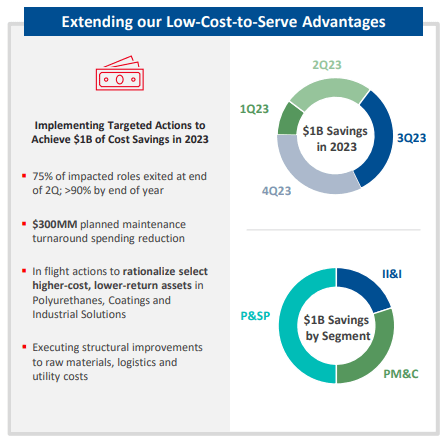

We can see that DOW’s current strategy to weather these market conditions is by prioritizing cost-saving measures throughout their business. They are targeting a savings total of $1B. This includes confronting maintenance turnaround spending and to reassess higher-cost but lower-return polyurethanes, coatings, and industry solutions.

DOW Investor Presentation

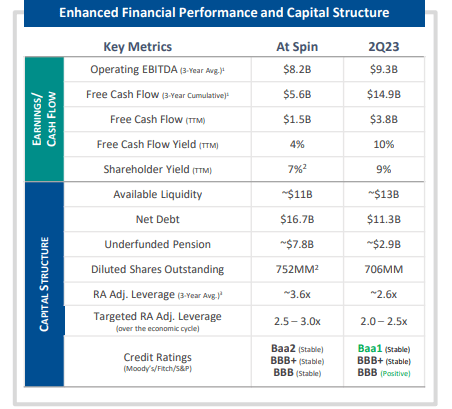

Lastly, we can see that since the spinoff, DOW has seen healthy growth in operating EBITDA, FCF, available liquidity, and a substantial decrease in net debt from $16.7B down to $11.3B. The reduction of debt allows buybacks as well as the potential to increase the dividend distribution. The decrease in debt will also result in DOW paying less in interest payments which is likely to result in an increase of free cash flow.

Dividend Yield

DOW offers a solid dividend yield of 5.2%, one of the highest among its peers. Unfortunately, we haven’t had a chance to experience a track record of dividend raises yet because of the company currently take a cash preservation approach during unfavorable market conditions. Despite this, the company’s cash flow comfortably covers the dividend. DOW’s cash per share is $4.16 while the dividend payout is currently $2.8 per share. This represents a payout ratio of roughly 67%. I anticipate this payout ratio to shrink within the next 5-year period as margins get larger and profitability starts to rise.

We can determine from their latest Q2 results that DOW is in strong financial standing. DOW generated $1.3B of cash flow from operations while paying out about $500M to shareholders as a dividend.

DOW Investor presentation

I fully expect dividend raises in the future as signals indicate profitability likely to rise over the next decade as natural gas prices settle out and DOW is able to capitalize on better profit margins from better macro environment conditions. This includes better profit margins because of local prices on items such as polyethylene, primarily used for flexible packaging. I plan on collecting more shares below the $55 price and enjoy a steady income stream of dividends while we ride out this cycle of reduced demand.

Valuation

According to Seeking Alpha, analysts hold optimistic outlooks for DOW. While they anticipate challenges in the current year due to a global economic slowdown, they project a swift rebound and anticipate the company’s earnings to experience double-digit growth over the coming years. Analysts have forecasted earnings per share of $3.94 for 2024 and $4.80 for 2025. This is understandable in my opinion because of the likely increased profit margins from a more suitable set of macro-economic conditions.

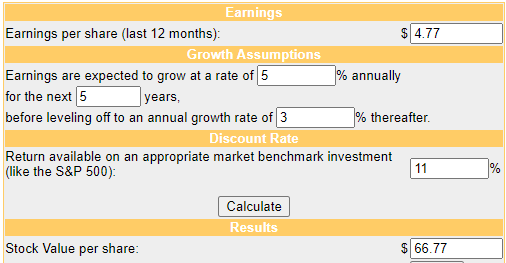

In addition, using a DCF (Discounted Cash Flow) analysis and conservative growth estimate of 5% annually, we can determine a fair value of $67/share by 2025. From the current price level, this represents an upside of 22%.

Money Chimp DCF

Risk

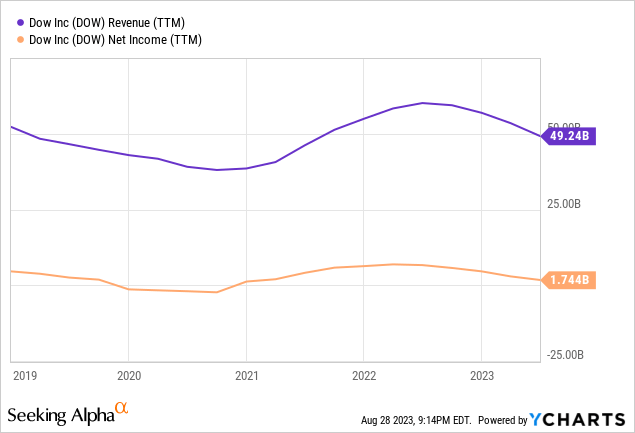

Total revenue amounted to $11.4 billion, marking a 27% decrease compared to the previous year. The drop in sales across all operational segments was due to reduced demand and prices resulting from a sluggish macroeconomic environment. In addition, sales declined by 4%, as the increase in volume was outweighed by the decline in local prices. Success here really depends on what the macro environment will shape to be.

This could be a barrier DOW faces looking forward and if they are not able to mitigate this margin somehow, I’d expect the price to stay flat or fall a bit under the $50/share mark. So far though, nothing here is concerning as DOW was able to strategically manage this current setback through targeted cost-saving measures and has the potential to continue doing so for the short term.

Conclusion

Dow Inc. (DOW) is a prominent player in the chemicals sector, emerging from a 2019 merger to offer diverse chemical, plastic, and fiber solutions. Committed to sustainable energy solutions, DOW’s global presence spans 31 countries and 104 manufacturing sites.

While revenue declined due to market challenges, DOW strategically manages costs, indicating better profitability when market conditions improve. Financially, DOW demonstrates positive cash flow growth and debt reduction, enhancing potential for buybacks and dividend growth.

Though risks persist, DOW’s adaptive strategies and growth potential position it for value creation. DOW’s capacity to innovate and seize macroeconomic opportunities will likely define its future success.

Read the full article here