Introduction

On February 20, 2022, I wrote an article titled Albemarle: One Of My Favorite Trades Going Forward. It was the first article I wrote on the Albemarle Corporation (NYSE:ALB).

After publication, the stock rose by more than 80%.

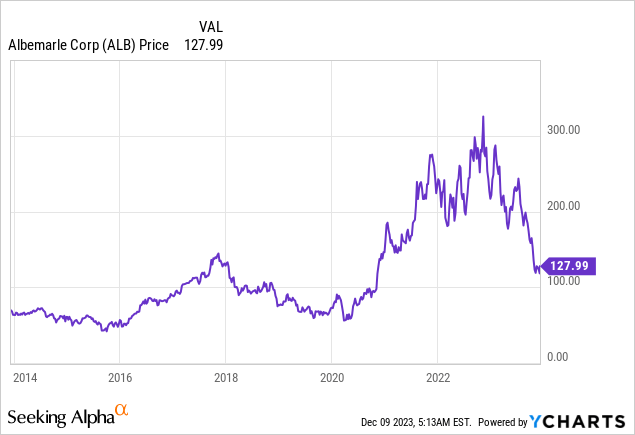

Unfortunately, the stock is now down 60% from its peak, falling 40% year-to-date. It’s now the 9th worst performer of the S&P 500.

While this may be bad for investors who were late to the party, I believe that Albemarle offers tremendous value at current prices.

Not only is ALB a dividend aristocrat with a history of more than 25 consecutive annual dividend hikes, but it seems that industry headwinds from falling lithium prices are starting to ease, providing (potential) ALB investors with an attractive risk/reward.

So, with all of this in mind, let’s take a closer look at the company!

What’s Up With ALB?

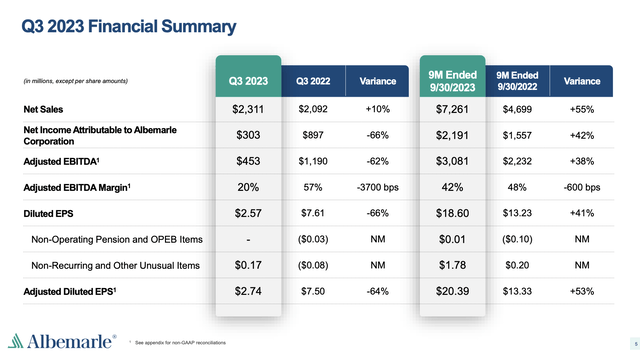

Lithium isn’t in a great spot, which is reflected in Albemarle’s most recent financial results.

For example, the third-quarter adjusted EBITDA was $453 million, down 62% year-over-year, primarily due to softer lithium market pricing and timing impacts.

Albemarle Corporation

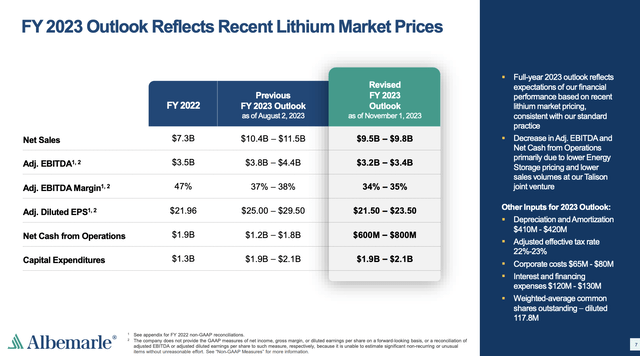

As a result, the company lowered its total outlook for 2023, with a range of $9.5 billion to $9.8 billion in net sales, and adjusted EBITDA expected to be in the range of $3.2 billion to $3.4 billion.

Adjusted EPS outlook was adjusted to $21.50 to $23.50.

Albemarle Corporation

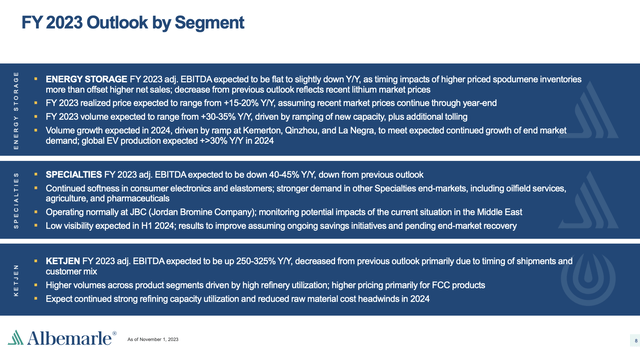

Specifically, the energy storage segment, which accounted for more than 60% of 2022 net sales, is expected to have net sales in the range of $7 billion to $7.2 billion in 2023, with adjusted EBITDA flat to slightly down.

Specialties segment net sales are projected to be approximately $1.5 billion, with adjusted EBITDA down 40% to 45% year-over-year.

Ketjen’s 2023 full-year adjusted EBITDA is expected to be up 250% to 325% year-over-year.

Albemarle Corporation

On top of that, the company stopped its pursuit to buy Liontown in October.

Albemarle CEO Kent Masters said in a statement that moving forward with the Liontown acquisition was not in his company’s best interests and was consistent with its disciplined approach to capital allocation. – Reuters

Reuters

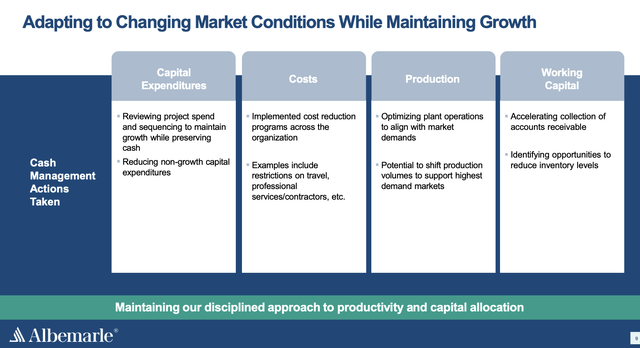

Instead of being an aggressive buyer, the company is proactively addressing cost management through a comprehensive review of actions aimed at supporting near-term profitability and cash flow.

The company is strategically managing its project spend and sequencing to preserve cash. This includes a reduction in noncritical travel and discretionary spending, demonstrating a commitment to disciplined financial practices – especially in this market environment.

Albemarle Corporation

In manufacturing, Albemarle is exceeding its goal of $170 million in productivity benefits for 2023.

This includes improvements in overall equipment effectiveness to enhance yield and utilization, expected to yield over $70 million in benefits.

The company is strategically sourcing raw materials to capture lower pricing, contributing to increased efficiency and cost-effectiveness.

Looking forward to 2024, Albemarle plans to build on these initiatives, targeting additional benefits across manufacturing, procurement, and back-office operations.

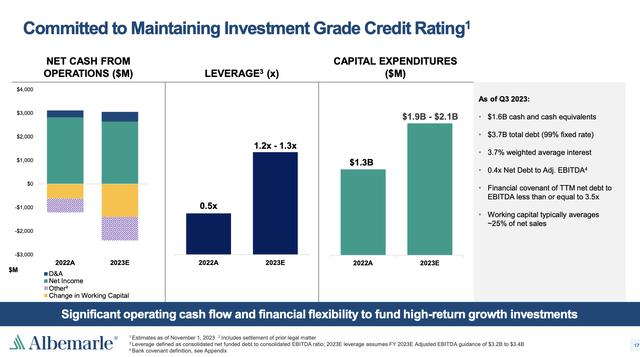

This also includes maintaining a healthy balance sheet. Despite the decline in EBITDA, the company expects to keep its net leverage ratio below 1.4x (EBITDA) this year. Almost all of its debt has a fixed rate. The weighted average interest rate on its debt is just 3.7%.

Albemarle Corporation

The company has an investment-grade credit rating of BBB.

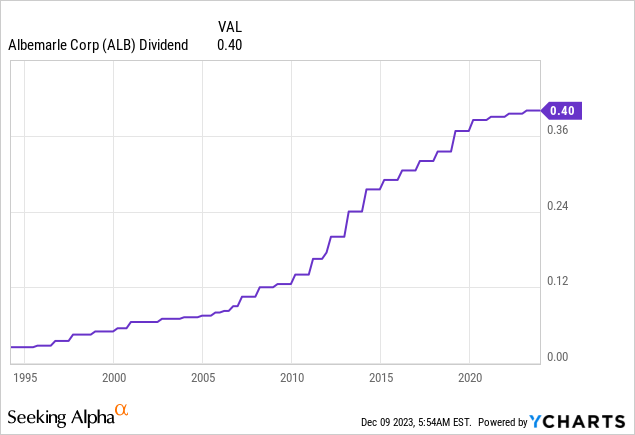

It also has a dividend that has been hiked for 28 consecutive years, although I cannot make the case that ALB needs to be bought for its dividend.

The company yields just 1.3%, and despite having a payout ratio of less than 6%, its five-year dividend CAGR is 3.8%.

What makes ALB attractive is its valuation and the opportunities in the lithium industry.

Light At The End Of The Tunnel

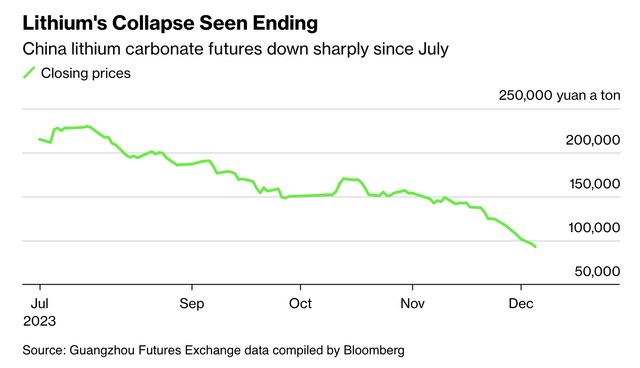

On December 6, Bloomberg wrote an article on ongoing developments in the lithium industry.

Reuters

According to the article, the lithium carbonate futures for January delivery on the Guangzhou Futures Exchange trades at roughly 92,450 yuan ($12,915) a ton, down from its peak of over 200,000 yuan in July.

Now, analysts suggest that the downward trend for lithium is nearing its end, projecting a bottom-out between 80,000 and 90,000 yuan a ton.

Bloomberg

Unfortunately, it’s a tough call to make.

Despite expectations of stabilization, challenges persist in the lithium market.

A surge in supply and a slowdown in electric vehicle sales growth have contributed to the current downturn.

The global market is not anticipated to return to a deficit until 2028, according to Bloomberg, which used Benchmark Mineral Intelligence data.

Looking ahead, the question arises whether the current cycle of lower lithium prices will lead companies to cancel or delay plans for new mines or refineries.

Also, the need for policy support from governments aiming to build their own supply chains becomes crucial. Albemarle has already observed cancellations and delays in response to market conditions.

I believe that massive economic challenges in China and the overall pressure on (often very expensive) electric vehicle sales in an environment of subdued consumer confidence are putting the brakes on a bull case that used to thrive on a lot of confidence and sky-high expectations.

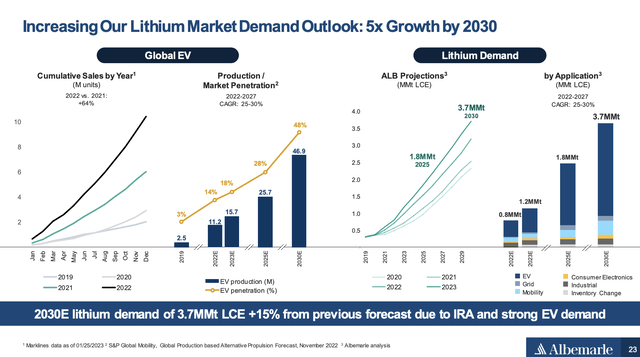

However, I do agree with Albemarle that the long-term bull case remains strong. While I’m not a fan of the EV trend (I prefer the gradual adoption of new technologies, starting with a push for hybrid vehicles), it looks like the EV market penetration will continue to rise, potentially reaching 50% in 2030.

This could push lithium demand to 3.7 million metric tons per year, as we can see in the chart below. Note that Albemarle has consistently hiked its long-term outlook.

Albemarle Corporation

Albemarle is expected to grow its lithium volumes by at least 20% per year during this period, breaching the 300-kiloton mark by 2027.

It also helps that the company is now trading at a deep discount.

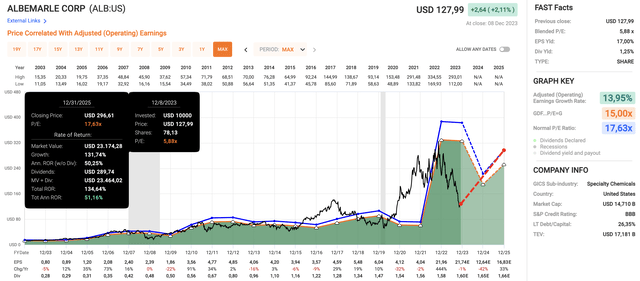

Using the data in the chart below:

- This year, ALB is expected to see a 1% EPS contraction, followed by a 42% decline in 2024. 2025 is expected to see a 33% recovery, which I expect to last.

- Currently, ALB trades at a blended P/E ratio of 5.9x. Even during the Great Financial Crisis, ALB was more expensive! In 2008, it traded at a blended P/E ratio of 8x.

- The long-term normalized P/E ratio is 17.6x.

- A return to this valuation by incorporation of expected EPS growth rates would pave the way for a fair value close to $300, which is roughly where it was trading last year before selling off.

FAST Graphs

While the attractiveness of its blended P/E ratio depends on its earnings outlook, I believe that a lot of weakness has been priced in.

At this point, it looks like cyclical risks have been massively reduced from the lithium trade, which leaves a lot of long-term secular tailwinds.

I also believe that the theoretical fair value of $300 for ALB makes sense. However, it won’t go there unless we see meaningful economic improvements.

Hence, despite my Strong Buy rating, I urge potential investors to be careful when dealing with cyclical mining companies.

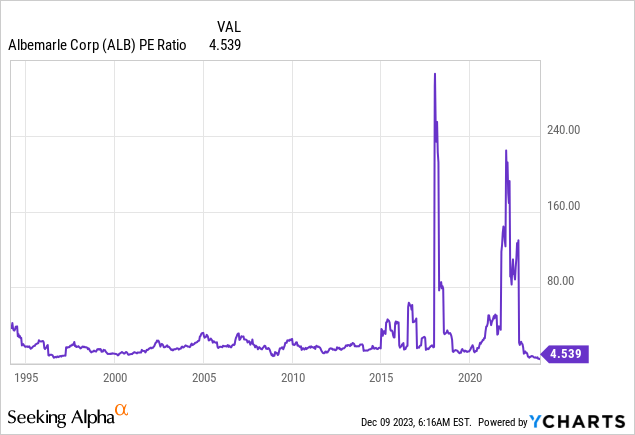

On a side note, the chart below shows the LTM P/E ratio going back to 1994. Although it does not incorporate forward-looking earnings, it does show how significant the valuation decline has been.

This brings me to the takeaway.

Takeaway

Despite recent challenges, Albemarle presents a compelling investment opportunity.

The lithium industry faces headwinds, impacting ALB’s financials.

However, the company’s proactive cost management, strategic initiatives, and strong balance sheet demonstrate resilience.

With a focus on efficiency, ALB aims to navigate the current market environment successfully.

Meanwhile, the decline in lithium prices may be nearing its end, with projections indicating stabilization.

ALB’s long-term outlook remains robust, aligning with the anticipated growth in the electric vehicle market.

Trading at a deep discount, ALB’s potential fair value of $300 suggests a significant upside.

Nonetheless, despite being a compelling long-term prospect, investors should be cautious with cyclical mining companies like ALB due to their volatile nature.

Read the full article here