Introduction

You may recall that I wrote an article on Dream Industrial REIT (TSX:DIR.UN:CA) (OTC:DREUF) in March 2020 and made the following conclusion:

The REIT has realized a 24% total return over the last six months when I was more bullish on the stock, it has blown its peers out of the water in that time. I still strongly believe that double digit returns are in the REIT’s near term future. The current 5% dividend yield is accompanied by a conservative payout ratio of 78% on FFO. Furthermore, the REIT trades at a 17% discount to NAV and with greater concentration in assets with yields over 6% combined with lower cost of debt than its peers they should still see spreads of over 3% on assets which will result in further NAV growth. The current discount to NAV is among the highest in its history as it usually trades above NAV. Although the FFO should see strong growth in 2023 as a result of capturing higher leasing spreads I don’t envision increased dividend payments as the REIT would be wise to get ahead of debt repayment to keep rising interest expenses at bay.

Source: Dream Industrial: Sweet Dreams Are Made Of These

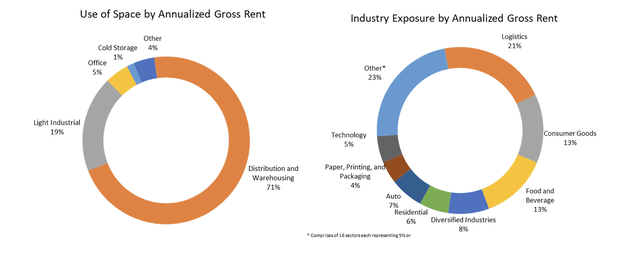

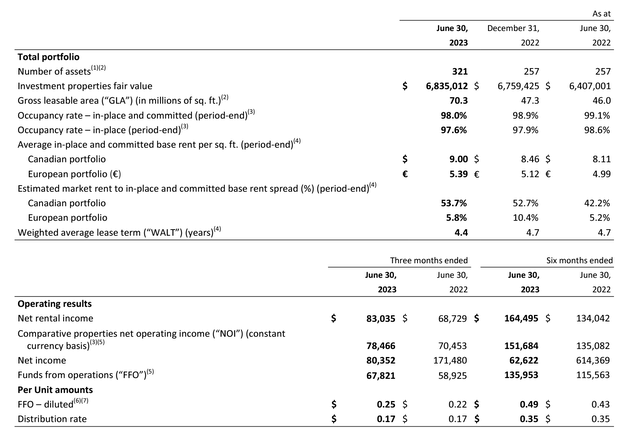

DIR owns, manages and operates 321 assets (536 industrial buildings) totalling approximately 70.3 Million square feet of GLA in key markets across Canada, Europe and the U.S. as at June 30, 2023. 71% of gross rent is in distribution and warehousing, 19% in light industrial and the remainder in urban logistics. DIR has assets mostly in Canada but has some assets in Europe and the USA.

Q2 2023 MD&A (Dream Industrial REIT)

I provide my updated investment thesis based on Q2 2023 results.

Q2 2023 Results

Q2 2023 MD&A (Dream Industrial REIT) Q2 2023 MD&A (Dream Industrial REIT)

On the plus side FFO per share was up 14% from the first 6-months of 2022. This was due in large part to the acquisition of a 10% interest in Summit Industrial Income REIT in Q1-2023 as part of a joint venture with GIC, a global wealth fund. This assisted in the increase in the GLA under management from 47 Million to 70 Million an increase of 49%. As mentioned in my previous article the acquisition was a bit pricey and the fact that NAV hasn’t budged is telling.

The other factor that played a role in the increase which I look much more favourably on is the renewal/re-leasing spreads the REIT has enjoyed over the 2023 fiscal year.

Q2 2023 MD&A (Dream Industrial REIT) Q2 2023 MD&A (Dream Industrial REIT)

From April 1, 2023 to July 14, 2023, DIR’s leasing team transacted approximately 1.4 Million square feet of leasing activity. Rental spreads were 81.1% and 91.4% in Ontario and Québec, respectively, as a result of the robust leasing market. From January 1, 2023 to July 14, 2023, the leasing team transacted approximately 2.4 Million square feet of leasing activity, with rental spreads of 83.1% and 56.0% in Ontario and Québec, respectively. Since the end of Q1 2023, DIR has transacted ~1.4 Million square feet of leases across their portfolio at an average spread of 47% over prior or expiring rents. In Canada, DIR signed 951,500 square feet of leases, achieving an average spread to expiry of 60.8% and an annual contractual rent growth of over 4%.

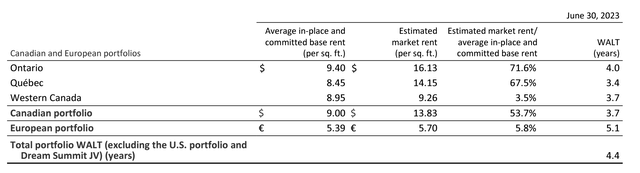

The WALT is a little below what I normally like to see for a REIT at only 4.4 year (only 3.7 years on its Canadian portfolio). I see this as a positive not a negative as it will allow them to take advantage of the hot market we are currently in for industrial space. As you can see market rents in Eastern Canada are 67-72% higher than in-place rents.

Q2 2023 MD&A (Dream Industrial REIT)

Along with capturing significant rental rate growth, DIR has added contractual annual rental rate escalators to leases that allow for consistently rising CP NOI overtime. In Western Canada, improving market conditions allowed them to embed higher contractual annual rent steps of 2–3%. Currently, the average contractual annual rental rate growth embedded in the Canadian portfolio equates to over 2.7%. In the European portfolio, approximately 87% of the leases are indexed to the CPI with the remainder of the portfolio having contractual rent steps of 2% on average.

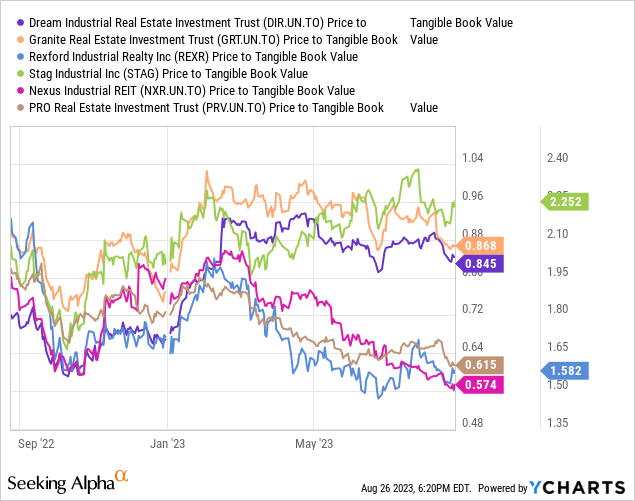

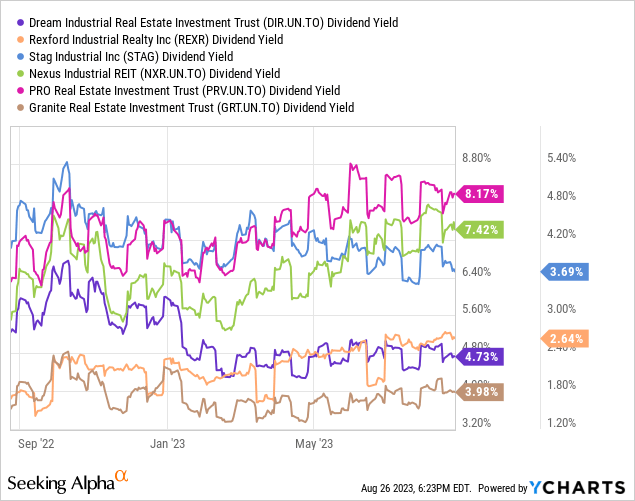

Valuation

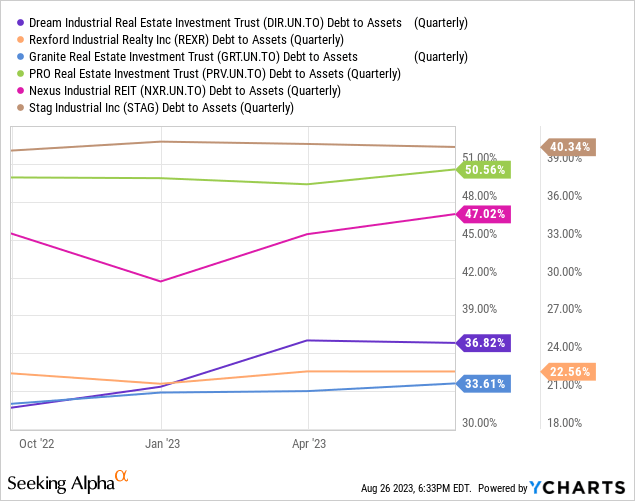

DIR is certainly not the cheapest of its peer group, especially compared to its Canadian counterparts like Pro REIT (PRV.UN:CA) and Nexus REIT (NXR.UN:CA). DIR is quite cheap relative to STAG Industrial (STAG) and Rexford Industrial (REXR). DIR’s portfolio includes more Tier 1 assets than its Canadian peers which is one reason it deserves a higher valuation but the other part is its leverage profile.

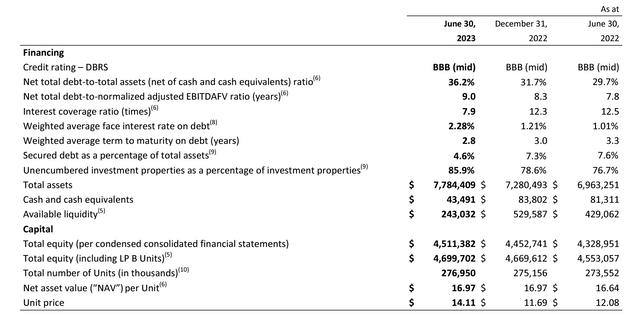

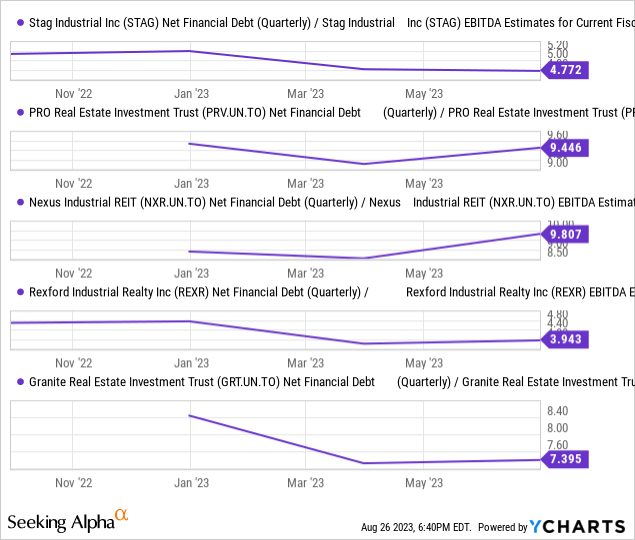

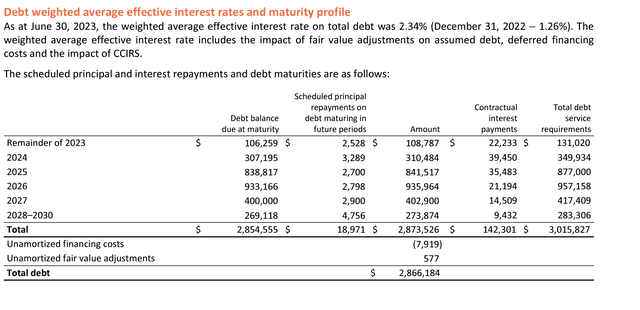

On a debt-to-gross assets basis DIR is almost as low as it gets at 37%. On a net debt to EBITDA basis that is not the case at 9.0X, which is hardly impressive even relative to its Canadian peers. This is common when the underlying assets have very low cap rates in the 4-6% range as is the case here. There is also a weighted average term-to-maturity at only 2.8 years so an increase in interest expense is inevitable over the next few quarters.

What is unique about this situation is that interest rates are extremely low for the REIT with the weighted average interest rate on debt being only 2.28% at June 30, 2023. Although this is twice the rate at December 2022 of 1.21%, the REIT is essentially paying less than the 5-year Canada bond Yield on its debt. DIR has benefited from very low interest rates as a result of having 69% of its debt structured in Europe where it had been taking advantage of lower rates than it would find in Canada. The bulk of the debt is unsecured debentures that mature in 2025 and 2026 so maturities over the next 6 quarters or so should not have a meaningful impact on interest expense and would be more than offset by rental step-ups and rent renewals/re-leases.

The $243 Million in available liquidity, combined with the $5.9 Billion in unencumbered assets (86% of investment properties), are more than sufficient to meet the 2023 and 2024 debt obligations.

Q2 2023 MD&A (Dream Industrial REIT)

The final ace the REIT has up its sleeve is the low payout ratio which sits at 68%. This is quite low when compared to PRV which has hovered around 90% the last few quarters and is in greater danger of having to cut its distribution.

Verdict

Although I still believe the risk-reward is as strong as any in the space I am more of a fan of playing this via covered calls or even cash secured puts as the price is not quite where I would call this a strong buy.

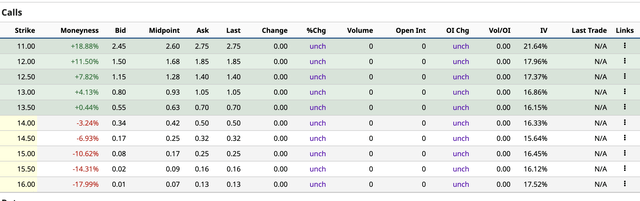

For example the calls for February 16th, 2024 offer an ATM call premium of $0.55/share. That is an ~8% annualized yield and when including the dividend the annualized yield would be ~13%. The downside to taking such a bet still looks attractive given the 25% discount to NAV, the low payout ratio, and well managed leverage. This would be a great opportunity for income investors.

Dream Industrial REIT Call Option Pricing (Barchart)

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here