The DoubleLine Income Solutions Fund (NYSE:DSL) is a closed-end fund, or CEF, that provides a way for income-seeking investors to achieve their goals of receiving a high level of current income from their assets. In addition, the fund could be a worthwhile addition to a portfolio for someone who is still in the process of building their wealth. This is because the very attractive 10.21% yield and monthly distribution provide fairly rapid compounding when reinvesting the distributions.

Unfortunately, as with most DoubleLine funds, this one primarily invests in bonds, so investors using purchasing this fund will want to hold their shares in a tax-advantaged account if they would rather not be surprised with a large tax bill at the end of the year. In addition, the fact that this fund primarily invests in bonds means that it will not be as good at protecting the purchasing power of your wealth against inflation. The high yield should somewhat make up for this, though, as long as inflation remains in the 2% to 3% range over the long term. I am not convinced that this will be the case, though, so it is still a good idea to be holding assets that will do a better job of preserving their purchasing power.

As just mentioned, the DoubleLine Income Solutions Fund boasts a very attractive 10.21% yield at the current price. This yield is slightly lower than many of the fund’s peers:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

DoubleLine Income Solutions Fund |

Fixed Income-Taxable-Global Income |

10.21% |

|

BrandywineGLOBAL – Global Income Opportunities Fund (BWG) |

Fixed Income-Taxable-Global Income |

11.02% |

|

First Trust/abrdn Global Opportunity Income Fund (FAM) |

Fixed Income-Taxable-Global Income |

11.16% |

|

MFS Multimarket Income Trust (MMT) |

Fixed Income-Taxable-Global Income |

8.55% |

|

Nuveen Global High Income Fund (JGH) |

Fixed Income-Taxable-Global Income |

9.61% |

|

abrdn Global Income Fund (FCO) |

Fixed Income-Taxable-Global Income |

14.30% |

As we can immediately see, the yield of the DoubleLine Income Solutions Fund is slightly below the median 10.62% yield of this peer group. This is not unusual for a DoubleLine fund, as the relative popularity of closed-end bond funds sponsored by this particular fund house has resulted in them having somewhat lower yields than the offerings from other managers. While this may cause some investors who are seeking to maximize their incomes to turn away, it is not necessarily a bad thing. After all, yields that are substantially above the sector peers are generally a sign that the market expects a distribution cut in the near future. That does not appear to be the case here.

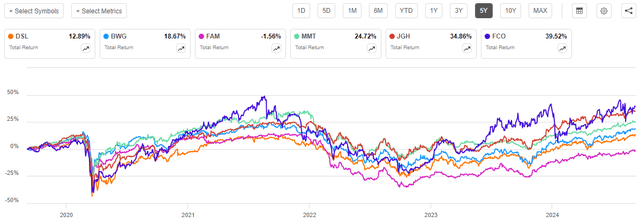

Unfortunately, however, the DoubleLine Income Solutions Fund has been one of the worst-performing funds in this peer group. As we can see here, investors in this fund have realized a 12.89% total return over the past five years. Only the First Trust/abrdn Global Opportunity Income Fund (FAM) did worse over the period:

Seeking Alpha

This is certainly not the type of thing that we really want to see, especially when we consider that funds such as the Nuveen Global High Income Fund (JGH) and the abrdn Global Income Fund have more than doubled this fund’s total returns over the past half-decade. This suggests that some hype surrounding the DoubleLine Income Solutions Fund may be misplaced.

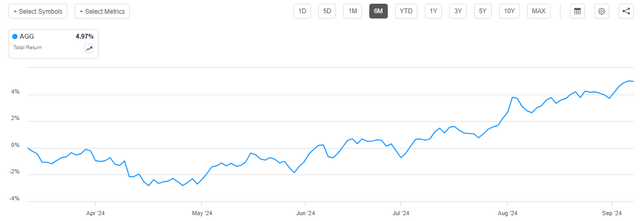

As regular readers can likely remember, we previously discussed the DoubleLine Income Solutions Fund in late April of this year. The bond market since that time has been rather choppy. During much of May and June, investors were uncertain about the direction of monetary policy in the United States, despite a few foreign central banks already beginning their monetary easing cycle. This changed in July, though, as investors suddenly became very optimistic that interest rates would be cut at the September meeting of the Federal Open Market Committee. Investors began bidding up bond prices and yields fell. This market action is quite obvious when we look at the chart of the Bloomberg U.S. Aggregate Bond Index (AGG) over the past six months:

Seeking Alpha

Note how the chart shows declines from March through early July, although it was very slightly positive during parts of June. It was not until July that bond prices went above their starting point on a sustained basis.

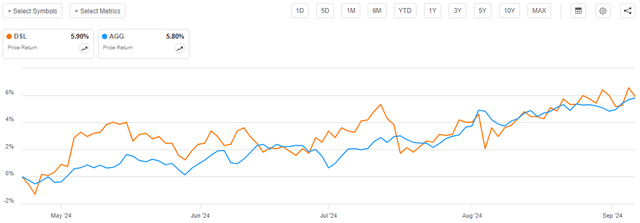

This leads us to make the assumption that the DoubleLine Income Solutions Fund has delivered a positive since our prior discussion, although the gains are likely to be back loaded and come primarily in the later months. That is indeed exactly what we see, as the fund’s share price largely tracked the domestic investment-grade bond index over the period:

Seeking Alpha

We do see though that the share price of the DoubleLine Income Solutions Fund was much more volatile than the bond index. The fund tended to decline more during downswings and appreciate more during periods in which the investment-grade bond index was appreciating. This overall resulted in the fund outperforming the index over the period. This volatility may have made it more difficult for holders of this fund to sleep at night, but it is what we would expect from a leveraged bond fund. The fact that this fund outperformed domestic bonds is also something that will likely be quite attractive.

It is important to note though that investors in this fund actually did much better than the share price performance chart suggests. As I explained in my previous article on this fund:

It is best to evaluate closed-end funds in terms of total return, not simply price return. This is because these entities pay out nearly all of their investment profits in the form of distributions. This tends to give them very high yields, and in some cases, these yields can be sufficient to offset declines in the share price. Exchange-traded funds that track indices do not do this because they do not tend to realize capital gains.

When we include the distributions that both the DoubleLine Income Solutions Fund and the Bloomberg U.S. Aggregate Bond Index paid out since our previous discussion, we get this alternative performance chart:

Seeking Alpha

This actually stabilizes the fund’s performance somewhat, as the large distributions served to offset some share price partially declines seen in the previous chart. Anyone who is reinvesting the fund’s distributions will certainly appreciate this, as the total value of the position has not seen nearly as steep peaks and valleys. We still also see that the DoubleLine Income Solutions Fund outperformed the investment-grade bond index over the period. We can all appreciate this. After all, any investor likes to beat the market indices.

As just over four months have passed since our last discussion about this fund, it is logical to assume that some things have changed. In particular, it now seems almost certain that the Federal Reserve will cut the federal funds rate by 25 basis points later this month. The DoubleLine Income Solutions Fund also released its semi-annual report that provides us with much-desired information about the fund’s ability to cover its distribution. Therefore, let us revisit the fund using this new information and see what changes, if any, we need to make to our thesis.

About The Fund

According to the fund’s website, the DoubleLine Income Solutions Fund has the primary objective of providing its investors with a very high level of current income. This makes a lot of sense for a bond fund, and the fund’s website emphasizes that this is a bond fund. Here is the strategy description that the website provides:

The Fund will seek to achieve its investment objectives by investing in a portfolio of investments selected for their potential to provide high current income, growth of capital, or both. The Fund may invest in debt securities and other income-producing investments anywhere in the world, including emerging markets.

The strategy description clarifies that this fund is investing in debt securities, but that makes it very difficult to understand how this fund expects to invest in assets that provide growth of capital. As I explained in a previous article:

Bonds by their very nature are income securities, as they do not deliver any net capital gains over their lifetimes. This makes sense, as an investor will purchase a bond at face value and receive face value back when the bond matures. The only investment return for a bond held over its entire lifetime is the coupon payments made to the bond’s owner. Thus, bonds do not deliver capital gains over their lifetimes.

Basically, bonds do not provide growth of capital over the long term. The same concept also applies to senior loans, preferred stocks, and any other types of fixed-income securities. If the fund wants an income-producing investment that provides growth of capital, then it has to invest in dividend-paying common equities. This fund does not do that, as the fund’s most recent N-PORT filing makes clear. According to this document, the DoubleLine Income Solutions Fund had the following asset allocation on June 30, 2024:

|

Asset Type |

% of Net Assets |

|

Asset-Backed Obligations |

1.2% |

|

Bank Loans |

21.9% |

|

Collateralized Loan Obligations |

12.2% |

|

Foreign Corporate Bonds |

40.2% |

|

Foreign Government Bonds, Foreign Agencies, and Foreign Government-Sponsored Corporations |

12.7% |

|

Non-Agency Commercial Mortgage-Backed Obligations |

13.0% |

|

U.S. Corporate Bonds |

22.0% |

|

U.S. Government and Agency Mortgage-Backed Obligations |

3.5% |

|

Common Stocks |

0.3% |

|

Escrow Notes |

0.0% |

|

Rights |

0.0% |

|

Warrants |

0.0% |

|

Money Market Funds |

2.7% |

We can immediately see that the fund only has 0.3% of its net assets invested in common stocks at all. Of these, the majority are not dividend-paying common stocks. Here are the common stocks currently held by the DoubleLine Income Solutions Fund:

Fund Q3 2024 Holdings Report

And here are the dividend yields of these companies:

|

Company Name |

Current Yield |

|

CFG Investment SAC |

0.00% |

|

GTT Communications |

0.00% |

|

JOANN Inc. (OTC:JOANQ) |

0.00% |

|

Longview Equity |

0.00% |

|

Revenir Energy |

0.00% |

|

Riverbed – Class B (RVBD) |

0.00% |

These all appear to be financially distressed or companies that are in the process of being dissolved. For example, JOANN Inc. filed for bankruptcy back in March, and GTT Communications filed for bankruptcy back in 2021. Securities in bankrupt companies do not provide income, although they can sometimes generate capital gains. These securities are highly unlikely to have been selected by the fund’s managers as opportunistic investments to provide growth of capital, however. Rather, the fund almost certainly obtained them as a result of the issuing company defaulting on bonds that were held by the fund, and now the fund finds it very difficult or impossible to get rid of these equities. Thus, it does not appear that the fund is really investing in anything that can provide long-term capital gains.

With that said, bonds can provide trading profits in response to interest rate movements. If the fund consistently bought bonds at a time when interest rates were high and then sold them when interest rates were low, then this would result in the fund’s net assets getting larger. However, the fund does not appear to be doing that to any great extent either. Its annual turnover rate is consistently fairly low for a bond fund:

|

FY 2023 |

FY 2022 |

FY 2021 |

FY 2020 |

FY 2019 |

|

|

Portfolio Turnover |

20% |

24% |

41% |

43% |

40% |

The fund’s semi-annual report states that the fund had a 20% non-annualized turnover rate for the six-month period that ended on March 31, 2024. That works out to 40% annualized, which is in line with what the fund had during the 2019 to 2021 fiscal years. It is significantly higher than the fund’s turnover during the 2022 and 2023 fiscal years, though.

It makes sense that this fund had higher turnover during the 2019 to 2021 fiscal years. That was a period in which interest rates were incredibly low in most countries. Nearly all developed markets reduced interest rates to the zero-bound during the COVID-19 pandemic and left them there until inflation became a worldwide problem in 2022. A “buy-and-hold” bond strategy does not really work well during periods of ultra-low interest rates, so the fund was forced to resort to trading bonds if it were to have any returns that would be acceptable to its investors. That is no longer the case today, so the fund was able to reduce its trading activity and simply revert to a coupon-collecting strategy. Once again, this has started to change as some developed-market central banks (and a handful of emerging markets) have cut their benchmark interest rates year-to-date. In addition, there was some opportunity to realize capital gains back in late November and December 2023 as the market became overly enthusiastic about interest rate cuts. The higher turnover that we have seen in the fiscal year to date may have been caused by the fund taking advantage of this opportunity to realize profits.

This fund’s turnover is historically below some of its peers, however. Please consider the following comparison chart:

|

Fund Name |

Annual Turnover |

|

DoubleLine Income Solutions Fund |

20% |

|

BrandywineGLOBAL – Global Income Opportunities Fund |

26% |

|

First Trust/abrdn Global Opportunity Income Fund |

28% |

|

MFS Multimarket Income Trust |

39% |

|

Nuveen Global High Income Fund |

35% |

|

abrdn Global Income Fund |

35% |

(All figures are from the most recent annual report filed by each respective fund.)

As we can immediately see, the DoubleLine Income Solutions Fund has a lower annual turnover than any of its peers. This confirms that this fund has been mostly using a buy-and-hold strategy recently, whereas its peers have been more aggressively trying to realize capital gains by trading bonds. There are certainly advantages and disadvantages to each strategy, so investors can make up their minds about which strategy they prefer.

The fact that the fund’s non-annualized portfolio turnover for the first six months of the current fiscal year came in at the same level as its full-year fiscal-year 2023 portfolio turnover strongly suggests that the fund is more actively trading bonds and depending on capital gains today than it did a few months ago. The fund is therefore varying its strategy with market conditions, and this is something that any investor can appreciate.

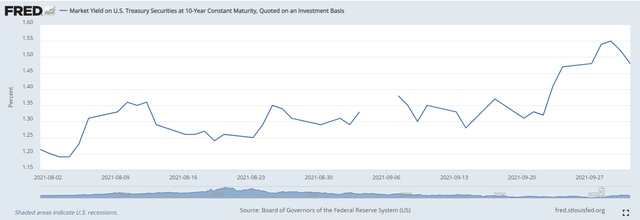

In a previous article, I pointed out that PIMCO’s “bond king” Bill Gross basically described all bonds as “trash” back in 2021. An article in the Financial Times quoted him:

Cash has been trash for a long time but there are new contenders for the investment garbage can. Intermediate to long-term bond funds are in that trash receptable for sure.

In September 2021, the yield of U.S. Treasury securities at ten-year constant maturity was sitting in the 1.30% range:

Federal Reserve Bank of St. Louis

It is unclear whether Mr. Gross would make the same comments today, with the ten-year constant maturity yield at 3.73%. However, there are some indications that he might, especially if the Federal Reserve cuts interest rates by more than the market expects. As of today, the ten-year U.S. Treasury yields 3.715%. That is a 2.34% after-tax yield for an investor in the top income tax bracket. The most recent year-over-year inflation rate based on the (flawed) consumer price index is 2.9%. Thus, the ten-year U.S. Treasury currently has a negative after-tax real yield.

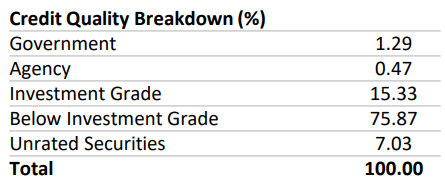

The DoubleLine Income Solutions Fund is not investing in ten-year U.S. Treasuries. The fund’s fact sheet states that the majority of its holdings consist of below investment-grade credit:

Fund Fact Sheet

As we can see, 75.87% of the fund’s assets are invested in securities that have junk credit ratings. As such, the majority of the fund’s holdings will have substantially higher coupon yields than the ten-year U.S. Treasury. However, most U.S. dollar-denominated bonds are priced based on a spread above the ten-year U.S. Treasury that supposedly accounts for the risk that any issuer apart from the United States government might default. Thus, the fact that the ten-year U.S. Treasury currently has a negative after-tax real yield suggests that the yield on every other type of bond is too low for the risks involved in holding it to maturity. Thus, this analysis suggests that bonds are overpriced. In addition, when we consider that any further bond price upside from today’s levels requires that the Federal Reserve cut interest rates by more than the market expects (the Federal Open Market Committee projects that this will not be the case), it becomes very difficult to make a case for buying bonds right now. This would therefore extend to a leveraged bond fund such as the DoubleLine Income Solutions Fund. There are equity closed-end funds that have similar yields to this one and a better risk-reward trade-off when we consider that equities are better at protecting against inflation (and U.S. Federal income taxes on dividends are lower).

Leverage

As is the case with most closed-end funds, the DoubleLine Income Solutions Fund employs leverage as a method of increasing the effective yield and total return that it earns from the assets in its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund’s leverage exceed a third as a percentage of assets for this reason.

As of the time of writing, the DoubleLine Income Solutions Fund has leveraged assets comprising 22.36% of its total portfolio. This represents a respectable decrease from the 23.21% leverage that the fund had the last time that we discussed it. As we saw in the introduction, the fund’s share price has increased fairly significantly since the last time that we discussed it, so we would expect that the fund’s leverage would have come down somewhat.

Typically, an increase in the share price correlates to an increase in a fund’s net assets per share. This makes sense because investors are willing to pay more for more assets. However, as we have seen in several articles over the past few months, the market has been bidding up the share price of numerous closed-end funds by more than is justified by their performance. As such, the share price gains have been outpacing the net asset value gains. This was the case for the DoubleLine Income Solutions Fund as the fund’s net asset value is only up 4.07% since our last discussion:

Barchart

This is less than the 5.90% gain of the share price, which suggests that the fund has gotten much pricier since the last time that we discussed it. We will discuss this later in this article. For now, the important thing is that the fund’s net asset value has increased over the period so we would expect its leverage as a proportion of the overall portfolio to have decreased over the same period. That is indeed what we see here.

The current leverage ratio of the DoubleLine Income Solutions Fund is substantially below the one-third of assets levels that we would ordinarily deem to be acceptable. However, that level is just a generalization and may not apply to every fund given the wide disparity in investment strategies. We should, therefore, compare the fund’s leverage ratio to that of its peers to attempt to determine whether its current level of leverage is appropriate for its strategy. This data is summarized here:

|

Fund Name |

Leverage Ratio |

|

DoubleLine Income Solutions Fund |

22.36% |

|

BrandywineGLOBAL – Global Income Opportunities Fund |

42.07% |

|

First Trust/abrdn Global Opportunity Income Fund |

20.12% |

|

MFS Multimarket Income Fund |

25.00% |

|

Nuveen Global High Income Fund |

27.45% |

|

abrdn Global Income Fund |

30.74% |

(All figures from CEF Data.)

As we can clearly see, the DoubleLine Income Solutions Fund is currently employing a lower level of leverage than most of its peers. In fact, there is only one fund that is less leveraged than this one. As such, it does not appear that this fund is borrowing too much money. Investors should not need to lose any sleep here.

Distribution Analysis

The primary objective of the DoubleLine Income Solutions Fund is to provide its investors with a very high level of current income. In pursuit of this objective, the fund pays a regular monthly distribution of $0.11 per share ($1.32 per share annually). This gives the fund an attractive 10.21% yield at the current share price. While this yield is lower than many peer funds are offering, it is still among the highest yields currently available in the market.

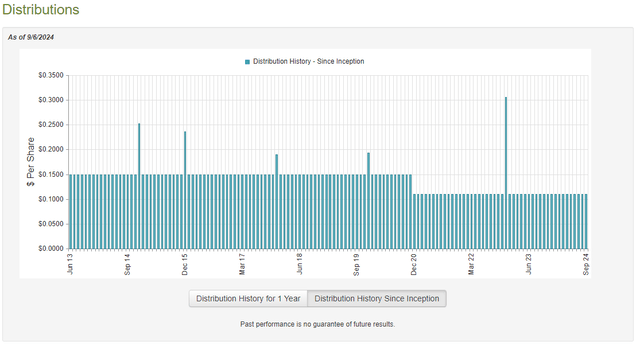

The fund has been consistent regarding its distributions over the years, but it did reduce the payout a few years ago:

CEF Connect

As I stated in my previous article on this fund:

As we can see here, in late 2020 the DoubleLine Income Solutions Fund cut its distribution by 26.67%, which reduced it from $0.15 per share monthly to the current level of $0.11 per share monthly. This is something that might prove disappointing and unattractive for those investors who are seeking to receive a safe and consistent level of income from the assets in their portfolios. However, this fund still exhibits much more stability than most debt-focused closed-end funds that change their distribution every year or two due to interest rate fluctuations. The biggest disappointment here is that we would ideally want our incomes to increase over time in order to keep up with the rising cost of living in an inflationary environment. There are very few closed-end funds that actually manage to deliver consistent distribution growth over time and at any rate, it is easy enough to achieve a rising income by reinvesting a portion of the distribution that is received.

The DoubleLine Income Solutions Fund kept its distribution steady since our last discussion, so there is no need to discuss any changes there. However, the fund did release an updated financial report that will give us better insight into how well the fund is covering its distributions. After all, as we saw in the previous article, the DoubleLine Income Solutions Fund failed to cover the distributions that it paid out for the full-year period that ended on September 30, 2024, so it really needs to improve in this area.

As of the time of writing, the most recent financial report that is available for the DoubleLine Income Solutions Line is the semi-annual report for the six-month period that ended on March 31, 2024. A link to this report was provided earlier in this article. As just mentioned, this is a newer report than the one that we had available at the time of our previous discussion, so it will work well to provide an update.

For the six-month period that ended on March 31, 2024, the DoubleLine Income Solutions Fund received $66,960,609 in interest and $197,463 in dividends from the assets in its portfolio. This gives the fund a total investment income of $67,158,072 for the period. The fund paid its expenses out of this amount, which left it with $46,948,893 available for the shareholders. That was not sufficient to cover the $68,437,996 that the fund paid out in distributions during the period.

Fortunately, this fund was able to make up the difference through capital gains. For the six-month period that ended on March 31, 2024, the DoubleLine Income Solutions Fund reported net realized losses of $43,165,584, but this was more than offset by $168,616,263 in net unrealized gains. Overall, the fund’s net assets increased by $141,574,463 after accounting for all inflows and outflows during the period.

We can immediately see that the fund did manage to fully cover all of its distributions during the six-month period. It is worth noting that its net assets were bolstered by the issuance of new shares that brought in $37,612,987, but even without this new money the fund’s net unrealized gains would have been sufficient to ensure full distribution coverage. The only real concern here is that the fund had to rely on unrealized gains to cover the distribution, which may not be problematic if the market corrects before the fund realizes the gains. However, that seems unlikely to occur unless the Federal Reserve suddenly increases interest rates, and it will not do that given current economic data. Thus, for now, it appears that the fund’s distribution should be reasonably safe.

Valuation

Shares of the DoubleLine Income Solutions Fund are currently trading at a 1.64% premium to net asset value. That is reasonably in line with the 1.57% premium that the shares have been trading at on average over the past month. This is too high of a price to pay for this fund, especially given the limited upside potential of bonds right now. The DoubleLine Income Solutions Fund appears to be a reasonably good bond fund, but there is no good reason for it to trade at a premium when some of its peers have delivered a better performance over the past five years and trade at discounts.

Conclusion

In conclusion, the DoubleLine Income Solutions Fund appears to be a decent bond fund, but that is all it is. It is very difficult to make a good case for buying any bonds right now because yields on an after-tax real basis appear to be too low and there is very little upside potential unless the Federal Reserve cuts by more than the market expects. That would almost certainly require a very severe recession that wipes out an enormous amount of the fiat wealth created since the pandemic. There are no financial analysts or economists that expect such a severe recession and as such, bond upside is probably pretty limited right now.

I am torn between maintaining a hold rating on this fund or downgrading it to a sell. On the one hand, there are equity closed-end funds that can match the fund’s yield and offer significantly more upside. It may make sense to sell this fund and purchase one of them. On the other hand, the DoubleLine Income Solutions Fund can probably maintain its distribution, so it is a decent income play if held in a tax-advantaged account. For now, I will maintain the hold rating, but investors for whom long-term wealth building remains a priority may want to consider taking their gains here and moving into equities.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here