Investment Thesis

Dutch Bros (NYSE:BROS) has a competitive edge in the US coffee chain industry due to better restaurant-level margins and lower operating costs than its competitors. The management has set a conservative goal at the time of the IPO. The market has also set a similar tone for it. However, I see the company’s potential to be substantial and the pandemic and inflation pressures should act as a tailwind, accelerating the company’s growth. I expected the stock to be repriced shortly.

Company Background

Dane and Travis Boersma launched Dutch Bros in Oregon in 1992. Over the years, it has expanded to operate 876 stores throughout 17 states. It was invested by private equity firm TSG and went public in 2021. Despite going public, Travis retained ownership of 12 million A and B shares and TSG maintained a stake of 30 million shares, representing 34.5% of the shares outstanding.

During the IPO, the company revealed plans to open 4,000 stores in the US. During the IPO, Dutch Bros revealed plans to open 4,000 stores nationwide. This ambitious expansion strategy likely contributed to the founder’s and private equity firm’s decision to retain a significant ownership stake, viewing the IPO as the beginning of the company’s growth trajectory rather than its end.

Competitive Advantage

I believe the company holds a distinct advantage for growth within the sector due to its unique business model, featuring higher restaurant-level profit than its big competitor, Starbucks (NYSE:SBUX). A higher restaurant-level profit should give the company a competitive advantage, allowing it to succeed at the micro level.

Unit Economics

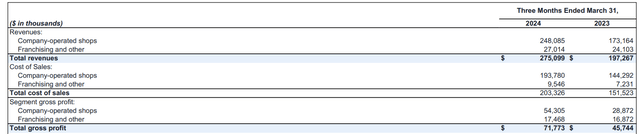

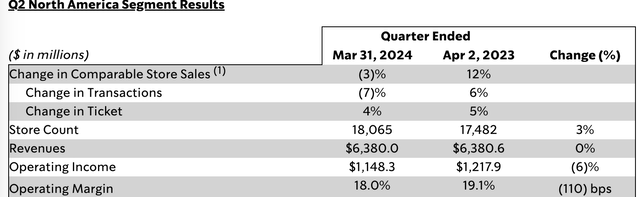

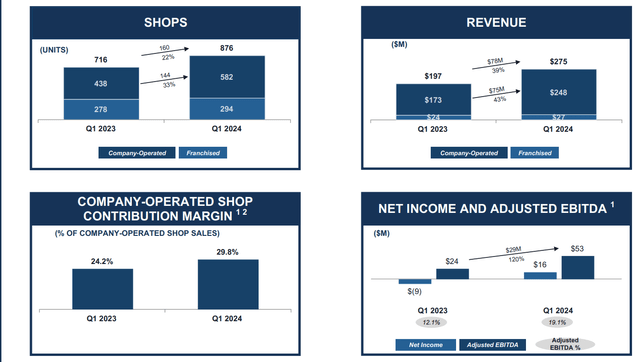

Starbucks does not reveal restaurant-level margins but discloses segment operating margins, which include license revenues in the margin calculations. However, licensing businesses typically have higher margins than company-operated stores. As a result, while including this high-margin business in its North American business calculation, Starbucks’ operating margin is only 18% as of Q1 2024, which is lower than Dutch Bros’ restaurant-level margin of 21.9%. (For comparison, we utilized a margin of 21.9% instead of a contribution margin of 29.8%.)

Margins (Dutch Bros’s presentation)

Margins (Starbuck’s presentation)

In addition, Starbucks discloses store operating expense statistics for our calculations. As a result, we can compare this metric to Dutch Bros and conclude that Dutch Bros has a significantly lower operational expenses ratio than Starbucks (44% vs 53%).

Expense ratio (Image created by the author with date from companies’ presentations)

How can the company have lower operating costs and higher margins? The answer is that the drive-thru accounts for approximately 90% of Dutch Bros business. Also, its retail lot sizes are typically smaller than Starbucks’.

Dutch Bro’s 10K

The company believes that its drive-thru business strategy prioritizes consumer convenience while achieving cost savings and preserving the personal experience.

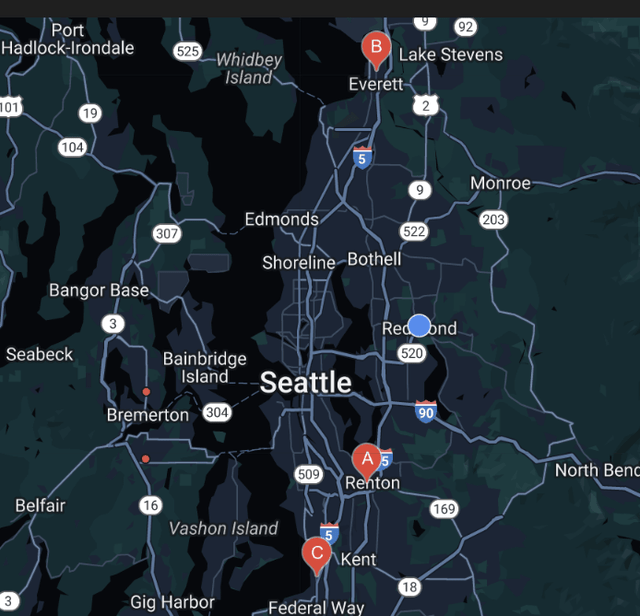

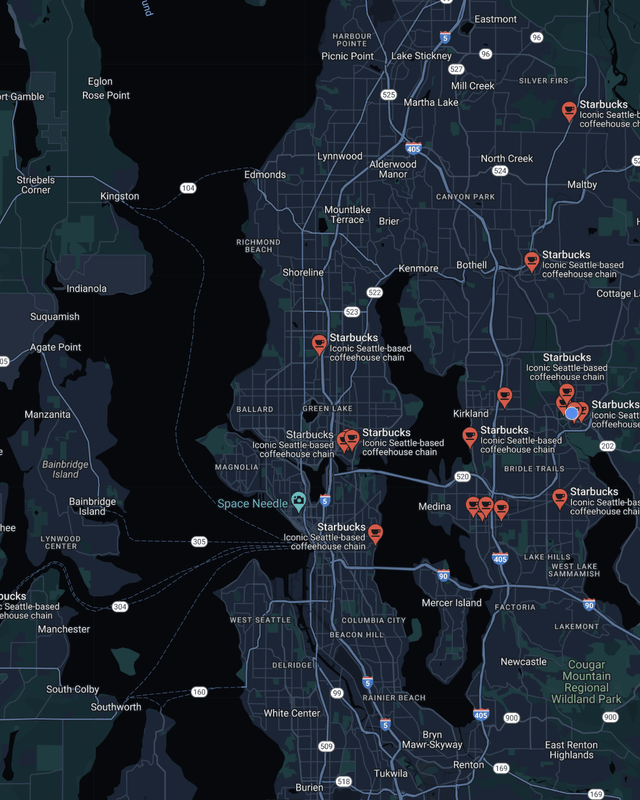

Its low occupancy costs can also be explained by its site location strategy. Using Washington State as an example, Dutch Bros opened stores in rural locations, as contrasted to Starbucks, which has more stores in metropolitan areas. This also results in decreased rent and occupancy costs for Dutch Bros.

Dutch Bros locations (Google Map) Starbucks location (Google Map)

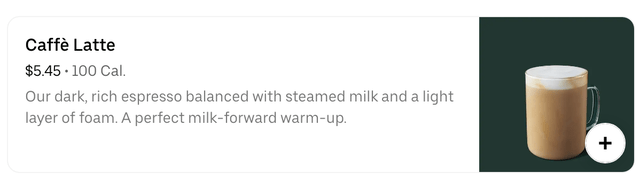

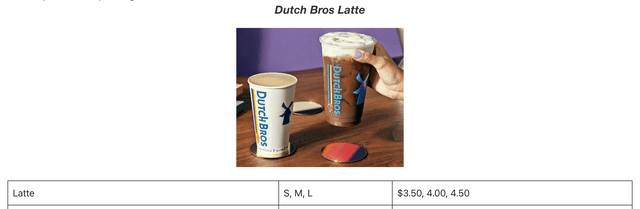

As a result, Dutch Bros can set its product prices cheaper than Starbucks. For example, in the Renton, Washington area, Dutch Bros charges $4 for a medium latte, while Starbucks charges $5.45 for a similar size, representing a 36% increase in price.

Starbuck’s website Dutch Bro’s website

Mobile App Strategy and Loyalty Program

The success of Dutch Bros can be related to the rise of mobile ordering. The company used its app as a strong customer acquisition and retention tool to drive traffic to its stores. The pandemic in 2020 also accelerated the expansion of drive-through restaurants and promoted mobile ordering. Dutch Bros seized the opportunity to start its loyalty program in 2021, and the firm estimates that as of the end of 2023, Dutch Rewards members accounted for nearly 65% of all purchases. The loyalty program helps the company to retain customers and also enhances the company’s low-cost moat.

Luckin Coffee Comparison

Dutch Bros is well-positioned for growth in the United States, capitalizing on the rise of mobile ordering, its fresh coffee, and low occupancy costs. In addition, Dutch Bros is not the only one adopting this strategy. In fact, the Chinese coffee company Luckin Coffee (OTCPK:LKNCY) has already implemented this business model in China. Luckin had a restaurant-level margin of 22% in 2023, which is similar to Dutch Bros. Luckin Coffee was founded in 2017. It went public in the US in 2019, setting a record for one of the fastest IPOs. Despite being delisted in 2020 owing to financial fraud, Lucking Coffee continued to grow fast, eventually overtaking Starbucks in China in 2023 with over 10,000 stores.

Expansion Speed Comparison

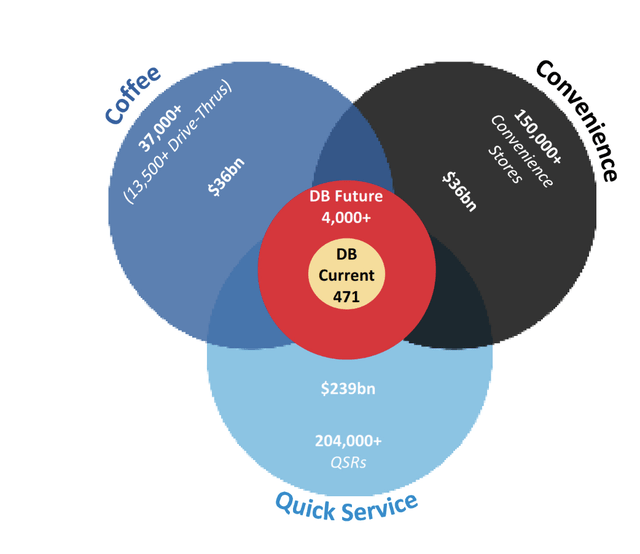

Market potential (Dutch Bro’s S-1 filing)

When Dutch Bros went public, it established a goal of opening 4000 stores in the United States. As of the conclusion of Q1 2024, Dutch Brothers had 876 stores while Starbucks had 18065 stores in North America. This presents significant upside potential for the company. However, Dutch Bros did not expand as quickly as its Chinese peer Luckin, which opened at a speed of an average of 1500 stores every year. Dutch Bros planned to open 150 in 2024 as it attempted to achieve both profitability and expansion at the same time. This is also partly owing to the difference in construction pace and regulatory requirements between the United States and China.

Expansion Opportunities

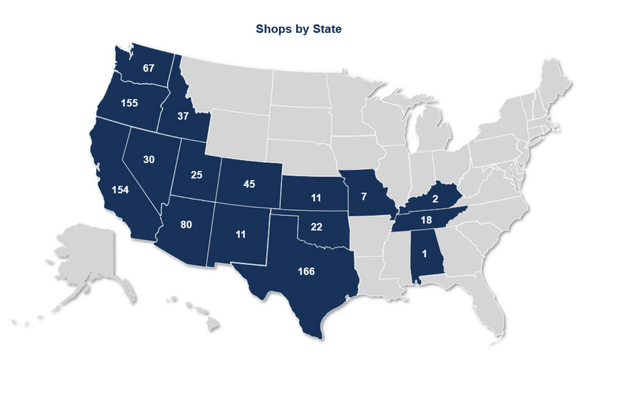

Dutch Bros is currently established in 17 states. I see that the company has plenty of opportunities for expansion in both emerging and existing markets.

Presence (Dutch Bro’s 10K)

Inflationary Pressures

Dutch Bro’s comp sales accelerated in 2023 and reached an impressive 10.9% in Q1 2024.

Comp growth (Dutch Bro’s presentation)

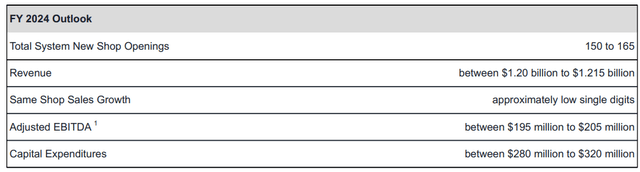

I believe the accelerated comp trend is driven by the inflationary pressures on consumers. While overall inflation has dropped, many people’s wages haven’t kept up, causing some to trade down. Retailers like Walmart (WMT) have noted this. As a result, Dutch Bros appears to be benefiting from this. Its strong Q1 performance led the company to raise annual guidance.

Outlook (Dutch Bro’s presentation)

DCF Valuation

When evaluating high-growth companies, I prefer using a discounted cash flow (DCF) valuation model. It gives you a better long-term view instead of just looking at short-term metrics. To calculate the required rate of equity of 19.1%, I utilized a 2.44x beta, a 4.5% risk-free rate, and a 6% risk premium. When combined with the 15.7% cost of debt, I arrive at a 19% WACC.

Base Scenario

My base scenario was a 10-year forecast based on management’s expectation of 4,000 stores, with an AUV of $2 million and 2% inflation. This translates to a CAGR of 23% for the following ten years. I also presume the company can maintain a 20% free cash flow margin. These assumptions are regarded as modest given that the company’s revenues expanded by 39% in Q1 2024 while its contribution margin reached 29.6% (excluding depreciation and amortization expenses).

Financials (Dutch Bro’s presentation)

With a net debt of $-29 million and a terminal growth rate of 3%, I arrived at a market capitalization of 5.5 billion, or $31.2 per share, which is 13% higher than the current price.

DCF forecast (Image created by the author with date from companies’ fiinancials)

Bull Case Scenario

Based on my analysis, I believe management’s prediction is conservative. In Q1 2024, the company’s revenues increased by 39% while its store count increased by 22%. Franchise store growth of 33% surpassed company-operated outlets. This shows that there is a possibility for additional market penetration and more franchisor interest because of the strong returns. The company is likely to raise guidance in the next couple of quarters.

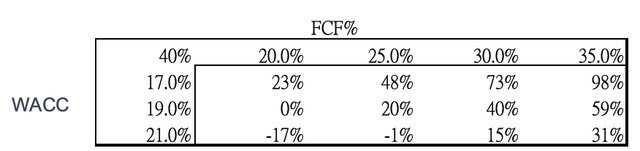

As a result, my bull case assumption is that the company will reach 6000 locations in ten years, accounting for one-third of Starbucks’ North American presence. The free cash flow margin is 30%, which is comparable to its contribution margin. This translates to a 30% sales CAGR and a valuation of $8.8 billion, or $50 per share, a 40% increase from the current level. The sensitivity analysis below shows a solid margin of safety.

Sensitivity test (Image created by the author)

If Dutch Bros can replicate Luckin’s success in China and surpass Starbucks in the US while maintaining similar margins, my current valuation would be conservative, as I assume only 3% terminal growth after 10 years.

Bear Case Scenario

My bear case is that the company did not expand as quickly as I expected, lowering the CAGR to 17% (in line with 150 stores per year at the current rate) while maintaining a 25% free cash flow margin. This translates to a $3.3 billion market capitalization, or $19 per share, with a 47% downside risk.

Competition Risk

If Starbucks or other convenience businesses, such as grocery stores at gas stations, replicate the idea of building small stores in rural areas with a similar mobile app strategy, Dutch Bros’ expansion may slow. This should not only reduce its upside potential, but may hurt its margin.

This is exactly what happened in China, as several convenience store chains recognized Luckin’s success. However, Luckin was able to defend competition and retain its customer base by introducing a loyalty program, which Dutch Bros is currently implementing. Hence, investors should monitor the competition risk while paying close attention to the growth of Dutch Bro’s loyalty program, which measures the retention of its customer base.

Catalyst

I get why the market thinks the stock is worth around $6 billion, which matches my base scenario. It’s because the management is sticking to their plan of opening 150-165 stores in 2024. Even though the company’s comp sales are accelerating, the market hasn’t fully caught on to its potential for growth in this inflationary setting. Even if the company maintains its current rate of growth, I believe it will attract more customers seeking lower-priced options due to inflation. This could lead to an increase in the number of sales, resulting in improved margins. Consequently, I anticipate that the market will recognize its growth potential within the next 6-9 months. The stock should be repriced accordingly then.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here