Even though I ascribe to the value investment philosophy, I also recognize that there are many ways to generate strong returns in the market. Growth investing is one of the most popular. It is also rather exciting. The thought of buying a company during its early stages of growth, only to see it propel higher over the years, generating stronger returns from year to year, is undeniably tantalizing. However, it also comes with certain risks. The biggest is that growth-oriented opportunities often require investors to pay rather significant premiums over what the company is worth at the moment. This can turn out well if the business in question meets the markets expectations. But if growth should falter, even if that growth is impressive, downside pain can be significant.

In my earlier days as an investor, I regretted missing out on one particular food-oriented growth play. And that was Chipotle Mexican Grill (CMG). At that time, the company was trading out earnings multiples of 50, 60, and sometimes even higher. And yet, I could not convince myself to take a bullish stance on the enterprise. One company that I have come across that has some similar characteristics to it is Dutch Bros (NYSE:BROS), a drive-thru shop owner that focuses on the sale of beverages. At first glance, shares of the company are incredibly expensive. And for those who hate the idea of paying a premium for growth, the business is definitely one that investors should stay away from. However, for anybody with a taste for growth, I would say that this is a solid prospect to consider.

A growth play with potential

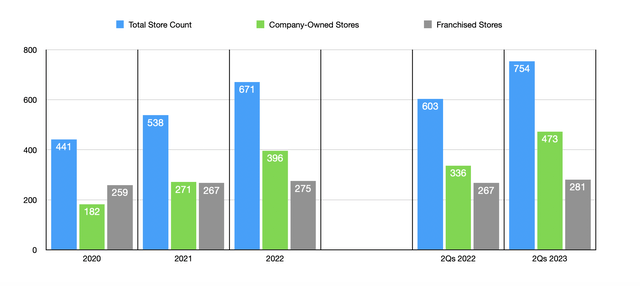

Before I get into the more financial side of the picture, it would be helpful, I believe, to discuss a little bit about Dutch Bros’ operations and where management is trying to take the firm. At present, the company has 754 drive-thru shops in its network. The majority of these, 473 in all, are company-owned, while the remaining 281 are franchised. This massive network began from a single location founded by a pair of brothers back in 1992. Those humble origins centered around a single double head espresso machine and a pushcart that the brothers operated in Grants Pass, Oregon.

Author – SEC EDGAR Data

Since its early days, Dutch Bros has truly transformed itself. Today, the company serves a wide variety of treats for its visitors. About 50% of its menu, for instance, is in the form of coffee-based beverages. Examples include its espresso based custom drinks, cold brew, and freeze blended beverages. Another 25% of its menu is based on the company’s Blue Rebel energy drink brand, which can be customized with various flavors and modifiers to fit the tastes of its consumers. And lastly, the remaining 25% of its menu involves A variety of teas, lemonades, sodas, and smoothies. Even though the company is physically oriented, it does have an app through which it provides a loyalty program for its customers. As of the end of 2022, the company had 5.2 million registered members on this app.

Management has high hopes in the company’s growth potential. They believe, for instance, that the enterprise can grow to have around 4,000 shops. And they believe that they can hit that number in the span of 10 to 15 years. More likely than not, the majority of these locations will be company owned. Management has not said as much, but that is the trend that I am seeing. Back in 2020, for instance, the business had 182 company owned locations. That stacked up against 259 that were franchised. Today, company owned locations outnumber franchised ones by nearly two to one. This has its ups and downs. The downside is that the company has more responsibilities and lower margins. But the upside is additional revenue and greater control over its brand. On top of this, if all goes well, there is always the opportunity to sell some of its locations at a rather hefty profit.

Author – SEC EDGAR Data

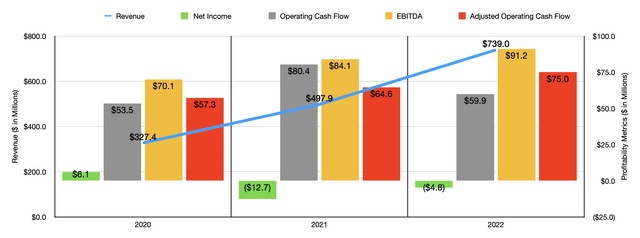

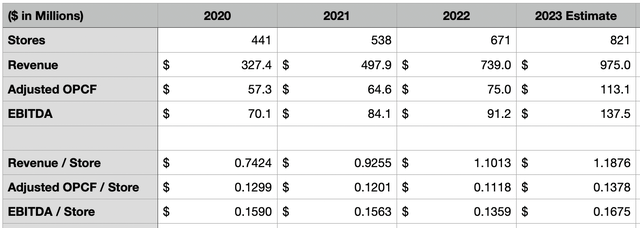

The overall growth in location count has allowed the company to significantly increase its revenue. Sales jumped from $327.4 million in 2020 to $739 million in 2022. Profitability has remained a problem for the company, with the business not really moving outside of the range of between a loss of $12.7 million and a gain of $6.1 million in any given year. At first glance, operating cash flow looks lumpy and directionless. But if we adjust for changes in working capital, we can see a consistent trend of growth. From 2020 to 2022, adjusted operating cash flow expanded from $57.3 million to $75 million. A similar trend can be seen when looking at EBITDA. From 2020 through 2022, it jumped from $70.1 million to $91.2 million.

Author – SEC EDGAR Data

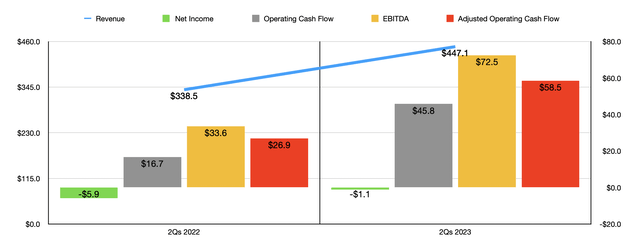

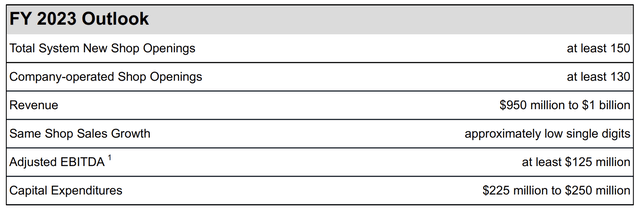

So far, the 2023 fiscal year is also looking up. A rise in location count from 603 locations to 754 caused revenue to grow from $338.5 million in the first half of 2022 to $447.1 million the same time this year. As the chart above illustrates, profitability remains an issue. However, all of the cash flow figures provided by management are demonstrating attractive growth year over year. Management expects this to continue for the entirety of 2023. Revenue should increase thanks to the addition of at least 150 locations, with at least 130 of these being company owned. Forecasts call for revenue of between $950 million and $1 billion this year. Meanwhile, EBITDA should come in at between $135 million and $140 million.

Dutch Bros

Of course, the kind of growth the company is achieving does not come cheap. In the first half of this year alone, management allocated $102.3 million toward capital expenditures. And in order to fuel growth further, on September 6th, after the market closed, management announced that they were planning to sell enough shares to generate up to $300 million of proceeds. On top of this, underwriters have been given a 30-day option that could increase this to $345 million. In response to this announcement, shares of the company plunged more than 7% after the market closed. As I write this, the market remains closed, and all calculations in what follows does not factor in this decline since we don’t know where prices might ultimately settle. However, given how pricey the stock is, I applaud the decision that management is making since it makes more sense to dilute shareholders in order to grow as opposed to taking on debt.

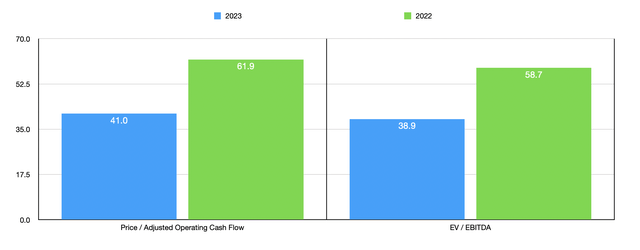

Author – SEC EDGAR Data

No estimates were given when it came to other profitability metrics. But by my calculation, adjusted operating cash flow should come in at around $113.1 million this year. Using these profitability metrics, I was able to value the company as shown in the chart above. It uses results from 2022 and estimates for 2023. Clearly, this is a very expensive firm. In the table below, meanwhile, I compared the enterprise to five similar firms. And when it came to both of the valuation metrics, even using the 2023 estimates, I found that four of the five enterprises I compared it to ended up being cheaper than it.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Dutch Bros | 41.0 | 38.9 |

| Wingstop (WING) | 48.9 | 43.3 |

| The Wendy’s Co. (WEN) | 14.2 | 12.1 |

| Shake Shack (SHAK) | 26.2 | 31.4 |

| Papa John’s International (PZZA) | 15.6 | 17.5 |

| Krispy Kreme (DNUT) | 16.8 | 23.7 |

Normally, this would cause me to be wary about buying into the firm. However, in the table below, you can see certain financial data regarding the company. I applaud it out average revenue per location, average adjusted operating cash flow per location, and average EBITDA per location for each of the past three years and, for the latter two, for the 2023 fiscal year. What is interesting is that you see revenue per store improve in each of these years, while profitability per store declines. But this should not be shocking when you consider that the company is growing its owned locations far faster than its franchised ones. Owned locations tend to have smaller margins than franchised locations do for the parent company. And they also generate far more in revenue for said parent.

Author – SEC EDGAR Data

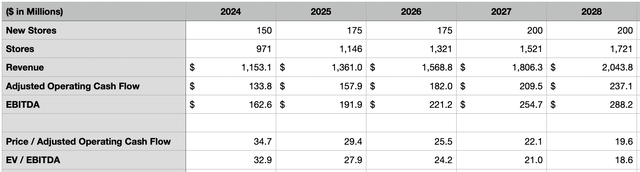

In the next table below, I decided to look at a scenario where the company continues to grow its store count over the next five fiscal years. I estimated how many locations would be added each year, so that number could ultimately change. I then took the most recent data provided by the company, including the forward estimates for profitability per location for this year. And from that point on, I forecasted revenue, adjusted operating cash flow, and EBITDA. The table also shows how shares are priced on both a price to adjusted operating cash flow basis and on an EV to EBITDA basis for each of those years. Truth be told, the firm does still look rather pricey until we get to around the 2028 fiscal year.

Author – SEC EDGAR Data

Takeaway

All things considered, I must say that I really like Dutch Bros. Even though I have never tried their beverages, the business model is attractive to me. As long as quality remains high and store placement is optimized, the picture for shareholders should be positive. I do still think the stock is very expensive and, as a value investor, I will once again sit on the sidelines. But for those who like a high quality growth prospect and don’t mind paying a premium for it, I could definitely understand the decision to buy the stock.

Read the full article here