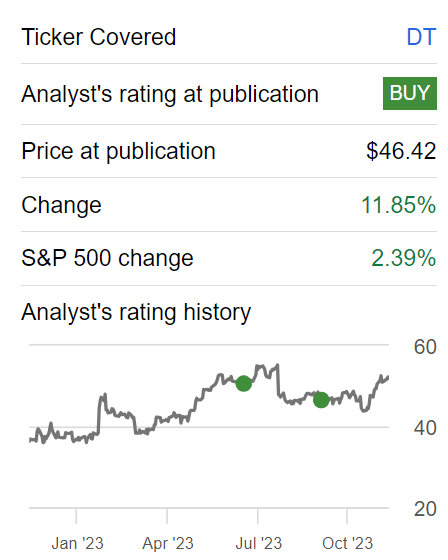

Investment Thesis

Dynatrace (NYSE:DT) is an observability platform that provides real-time insights into the performance and user experience of applications, helping organizations optimize their digital ecosystems. Dynatrace offers proactive monitoring, root cause analysis, and automation to ensure seamless and high-performing digital experiences.

Before we go further, keep in mind that Dynatrace has now reported its fiscal Q2 2024 results, not to be confused with calendar 2023. As we go through, I’ll only make reference to its fiscal year.

This is my investment thesis, Dynatrace is not a blemish-free investment. There’s the question mark hovering over whether in fiscal 2025 (starting in 2 quarters), Dynatrace will be able to improve its free cash flow margins back to the prior year.

But even with conservative estimates, you’ll soon see that the stock is now priced at less than 38x forward free cash flows, making it attractively priced.

Rapid Recap,

In my previous analysis, back in September, I said,

Here’s the pitch in a nutshell. This stock is priced at approximately 45x forward free cash flows. It would be wrong to say that this is the cheapest software stock going. But it’s hardly richly valued either. This is a stock for investors who are able to use this opportunity to buy into a stock with a small dip and remain patient, waiting for a better opportunity in the stock to present itself.

Since then, not only are we coming closer to wrapping up fiscal 2024, but also, management has raised its free cash flow line slightly.

DT Michael Wiggins De Oliveira

As such, I make the case now that Dynatrace is priced at less than 38x forward free cash flow, as we look ahead to fiscal 2025.

Dynatrace’s Near-Term Prospects

Dynatrace is currently experiencing fair success, as market dynamics indicate a rising focus on observability and application security for digital and business transformation. For example, large enterprises are increasingly seeking unified observability platforms, this is often referred to as platformization, rather than ad-hoc products.

Dynatrace is positioned as a leader in this space, providing AI-driven analytics and automation capabilities that enable proactive issue resolution and enhanced software liability and performance.

The company’s customer engagements reveal three key themes. Firstly, observability and application security are vital for digital transformation. Secondly, enterprises are moving away from fragmented monitoring tools, seeking unified platforms that leverage various data types for more efficient analytics and issue resolution.

On the other hand, there are some lingering uncertainties in the macro environment that may influence the decision-making processes of potential customers, which could impact the demand for Dynatrace’s observability and application security solutions. Case in point, Rick McConnell, Dynatrace’s CEO, highlights the cautious approach organizations are adopting due to these economic uncertainties, stating, “While we expect the current macro conditions to persist through the end of our fiscal year, we plan to increase spend levels prudently.”

Given this context, let’s delve into its financials.

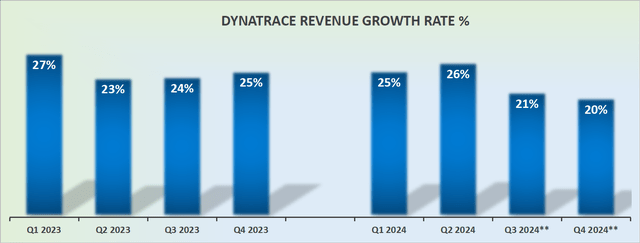

Revenue Growth Rates Are Still Alluring At Approximately 20% CAGR

DT revenue growth rates

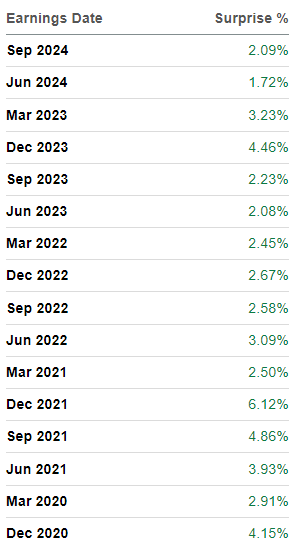

Dynatrace has a habit. A habit of delivering surprises. More specifically, a long-established habit of beating analysts’ estimates by at least 1%, see below.

SA Premium

Why do I highlight this? To demonstrate, this is not the sort of company that overpromises and under-delivers. Dynatrace’s management prudently ”manages” analysts’ expectations and financial models so that there are not a lot of negative surprises.

What’s more, this ability to avoid being left with negative surprises, boils down to its business model. This is a highly predictable business model where management can forecast and meet those forecasts. And that, I contend, is worthy of premium valuation, a factor that we’ll soon discuss. But before that, let’s talk about free cash flows.

Free Cash Flow Profile Discussed, A Negative Aspect

Dynatrace is expecting to see its free cash flow line deliver approximately $320 million in fiscal 2024, which is flat y/y. This is perhaps the most pressing consideration and detraction from the bull case.

It shows that although Dynatrace has been delivering significant growth in revenues since fiscal 2023, this isn’t translating into an uptick in free cash flows.

That being said, I don’t believe that investors will unduly punish Dynatrace on this consideration given that the business is clearly profitable and free cash flow producing, it’s just that their excess revenue growth rates haven’t translated into an uptick in free cash flows.

In fact, back in fiscal 2023, Dynatrace’s free cash flow margins stood at just shy of 29%, while this year its free cash flow margins are guided to have compressed by slightly more than 500 basis points to around 23%. In the next section, we’ll take these figures to discuss its forward valuation.

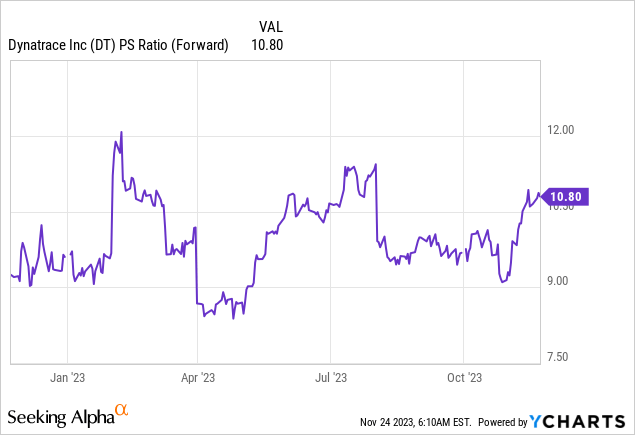

DT Valuation — Reasonably Priced at Less Than 38x Forward Free Cash Flows

Dynatrace has been in and out of favor with investors in the past 2 or 3 years. Indeed, as you can see above, in the past year its valuation has largely oscillated around 8x to 10x forward sales.

This means that investors today are not paying a large premium for a company with an attractive narrative.

Furthermore, put another way, I estimate that Dynatrace’s free cash flow could reach around $390 million in fiscal 2025. This would be a roughly 20% increase y/y from fiscal 2024 and would see its free cash flow margins expanding slightly to around 25% next year’s revenue line.

Note, that my estimate for its free cash flow is not stretched at all. In fact, as I noted earlier, back in fiscal 2023, Dynatrace had its free cash flow margins at just under 29%, and back in fiscal 2022, its free cash flow margin was also 25%.

Altogether, this reinforces that Dynatrace is very much capable of delivering around $390 to $400 million of free cash flow in fiscal 2025. Leaving this stock priced at less than 38x next year’s free cash flows, which is a very reasonable entry point.

The Bottom Line

In my investment analysis, I find Dynatrace to be a compelling opportunity.

While the consistent revenue growth rates are impressive, there are lingering uncertainties in the macroeconomic environment that may impact customer decisions, as highlighted by Dynatrace’s CEO, Rick McConnell.

Despite scrutiny on free cash flow margins, Dynatrace’s profitability and predictable business model mitigate concerns, making it an attractive investment.

The stock, currently priced at less than 38x forward free cash flows, appears reasonably valued, especially considering the company’s history of managing analysts’ expectations and delivering positive surprises.

Given its stability and predictability, I argue that investors are not paying a significant premium, and with a projected increase in free cash flows for fiscal 2025, Dynatrace presents a reasonable entry point for potential investors.

Read the full article here