Co-authored by Treading Softly

A glance through the history of humanity has shown us that one of the most frequent and common means of developing and growing wealth is to own land. For any commodity, its value is heavily dependent upon the fact that there is a limited supply of that commodity available. This is one reason a limited quantity of Bitcoin (BTC-USD) available makes it have more value. This is the same reason why gold and silver have long been units of holding value – because there is a limited supply of them available, and you’re able to value other things against them. Before we started trading in coins or digital tokens, there was something a little more tangible — land. Land has long been a means of showing wealth, as owners were able to use that land to produce food or other goods that they sold and were able to pay their employees. Owning land and, therefore, owning real estate continues to be a proven way of generating wealth. Many develop their wealth and riches through land ownership by being a landlord and renting out houses.

You don’t necessarily have to buy individual homes, rent them out, and deal with tenants, toilets, and taxes. Instead, through the financial markets, you have several options to own and have exposure to different types of real estate, all while collecting fantastic income from them. Today, I want to take a look at two options for owning real estate that I find to be fantastic deals today.

Let’s dive in!

Pick #1: GHI – Yield 10.3%

Greystone Housing Impact Investors (GHI) reported a quiet quarter, providing us with a clean look at how much its MRB (Mortgage Revenue Bond) business is producing. GHI has separated its investments into two core businesses. MRBs are mortgage bonds that are issued by state housing agencies to encourage the development of affordable housing. These bonds are exempt from federal taxes, and that benefit is passed along to investors through the partnership structure — yes, GHI issues a Schedule K-1 at tax time. GHI’s investment strategy is to be a provider of capital and take advantage of the spread between the yield it receives and the interest it pays on its own leverage. As a result, earnings from this section of the business are interest rate sensitive and reasonably predictable. GHI’s MRB business generally benefits from declining interest rates. So, the past few years haven’t been the best for it.

The second portion of GHI’s business is what we call the “Vantage” investments — although GHI has added additional partners beyond Vantage over the past year. The strategy in this segment is to provide a preferred equity investment in constructing multifamily residential buildings. The partner is responsible for the construction and management of the properties. Once construction is complete, they are leased up, and GHI gets a portion of the revenues. However, the real gains come when the leased-up property is sold.

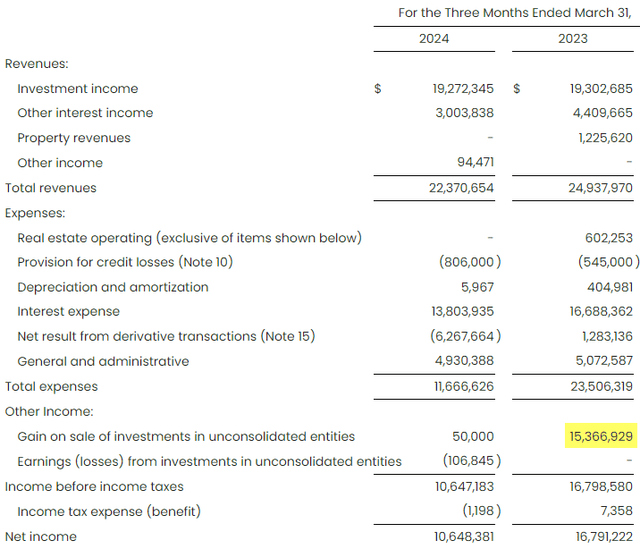

We can see this clearly comparing Q1 2024 to Q1 2023: Source

GHI Q1 2024 Earnings Release

Note the $15.366 million gain on sale. This was driven by the Vantage strategy. This filters down to CAD (Cash Available for Distribution), which we can see was approximately $13 million higher in Q1 2023 than in Q1 2024. This is primarily due to GHI recognizing a gain in 2023, but not in 2024 from the Vantage JV.

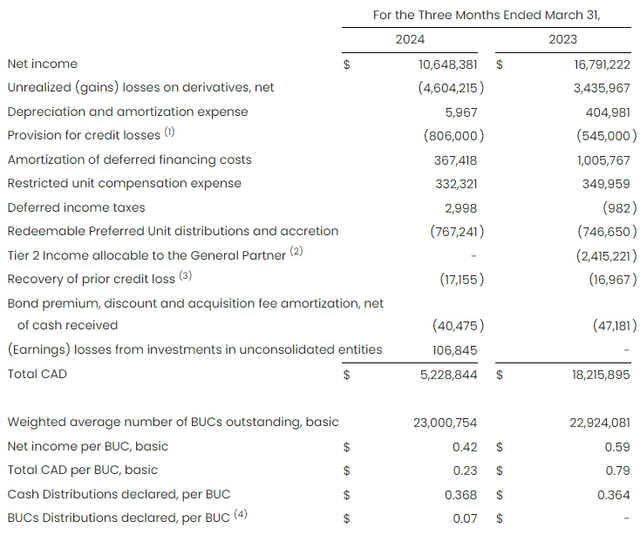

GHI Q1 2024 Earnings Release

So when we look at the headline of CAD being $0.23, and failing to cover the $0.368 distribution, some might panic. However, if we back out the gain on sale, CAD produced by the MRB investment strategy is about the same year over year. Investment income is about the same, and interest expense is lower in 2024.

GHI’s JV strategy creates lumpiness in CAD. It’s always nice to start the year off right with a large realized gain, but the process of selling properties is not one that should be rushed. To get top dollar, it takes time to market the property and negotiate with buyers, and even after a price is agreed upon, there is a period of due diligence before closing.

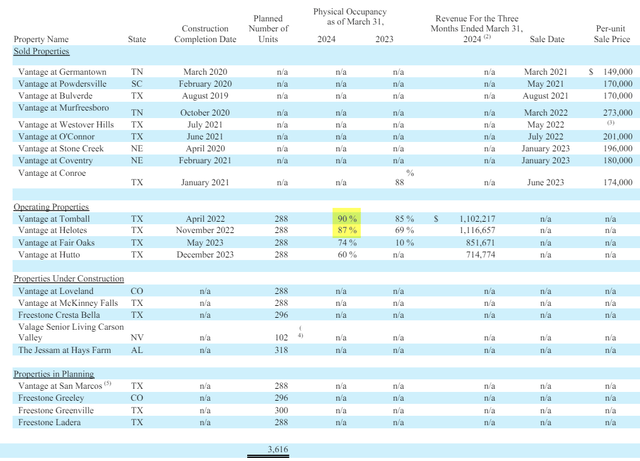

Here is a look at GHI’s current properties among their JVs that are pursuing this strategy: Source

GHI Q1 2024 10-Q

Two of them are ready to sell right now, and it is a question of when a deal can be negotiated and when the buyer is ready to close. Until they are sold, the properties are providing approximately $1.1 million in revenue each. Unless the real estate market completely collapses like it did in 2020, we can expect that these will be sold sometime this year. Two other properties are currently being leased up. These properties could be sold this year, or the JV might choose to hold on to them a bit longer, depending on market conditions.

GHI has a healthy pipeline, with 10 other properties that are under construction or in planning. From 2021 through 2023, GHI has been selling three properties per year. That has been enough to fund the current distribution and make so much in excess gains that GHI has been paying specials and supplemental distributions on top of it. We expect that we will see 2-3 properties sell this year, which should be more than sufficient to cover the current distribution with a possibility of more supplements/specials if they sell three. However, in future years, we could see the annual pace increase from 2-3 to 3-4 properties per year. This would either make supplemental distributions a lot more frequent or, if management believes the pace is stable enough, an increase in the regular distribution.

Pick #2: ONL – Yield 11.3%

Orion Office REIT Inc. (ONL) is a REIT that specializes in office space, and it isn’t a secret that office space is going through a tough period. We’ve seen numerous dividend cuts in the office sector as even well-established REITs have struggled with soft demand, declining property values, and higher interest rates. ONL has been spared the risk of a cut as it set the dividend extremely conservatively following its spin-off from Realty Income (O). At $0.10/quarter, ONL’s payout ratio in Q1 was 34% of FAD.

Q1 core FFO came in at $0.36, slightly higher than Q4’s $0.33. However, management warned us that it would decline in Q2, so don’t be shocked when there is an earnings “miss” reported across the artificially intelligent internet next quarter. Management warned that this was coming at Q4 2023 earnings. Yet many will be “surprised” that they weren’t making it up!

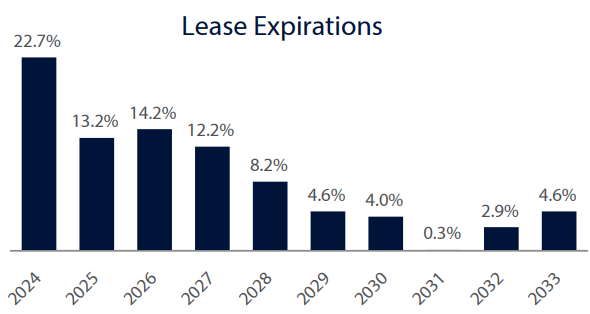

ONL has been facing headwinds from a glut of lease expirations at a time when many tenants are reassessing their need for office space. It has made significant progress but still has 22.7% of its leases maturing this year. After this year, ONL’s lease expirations will be at a much more reasonable pace. Source

ONL Q1 2024 Supplement

Q2 is expected to be a tough quarter because leases are expiring, and the tenants have informed ONL that they intend to vacate the property. In the current environment, ONL is not counting on being able to backfill quickly.

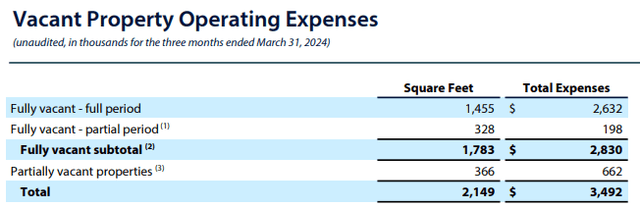

When leased, the tenant pays for various property-level costs like insurance, taxes, utilities, etc. — either paying them directly or as an expense that’s built into the rent amount. When a property is vacant, it still incurs expenses, and it falls on the landlord to ensure they get paid. In Q1, vacant properties cost ONL nearly $3.5 million.

ONL Q1 2024 Supplement

That is over $0.06/share being spent just to maintain vacant properties that are not producing any income. This is pushing down ONL’s Core FFO. The good news is that it is fixed immediately upon the sale or leasing of the property. Even if ONL were to give the properties away for free, Core FFO would go up over $0.06/share per quarter.

Fortunately, ONL isn’t giving them away for free. The REIT currently has 14 vacant properties, and 8 of those are under contract to be sold for $48.1 million. Management has guided that they don’t expect these sales to close until late in the year or even early 2025. So, for 2024, these properties will continue to be a drain on earnings both in the form of direct costs to maintain and in the form of trapped capital that is not producing any earnings.

The market for office space has been weak. While there are signs of stabilization in many markets, the fundamentals are not strong enough to support quick leasing and aggressive selling. Management is approaching the situation with patience. The dividend is well-covered, even with the expected decline in FFO, it will remain one of the best-covered dividends among publicly traded REITs.

Conclusion

With GHI and ONL, we’re able to invest in two very different types of real estate, from multifamily homes to office space, both of which continue to have valuable roles in the economy.

ONL continues to have a very conservative dividend payout ratio, while they’re managing the market-wide issues with office spaces by pursuing the sale due to the lack of interest in the current term.

GHI continues to own MRB tied to multifamily homes and collects tax-free income from it while developing multifamily properties to lease out and eventually sell.

In the long term, both of these real estate owning opportunities can provide us with strong income in the present while producing value from the land that they own in the long term.

When it comes to your retirement, I don’t want you to have to spend your time juggling tenants or dealing with complex taxes. Instead, I want you to spend every single moment enjoying your hobbies and your time with loved ones. Would you rather be figuring out your taxes or sitting back and enjoying your favorite beverage while watching the sunset at the end of another glorious day? I would always pick the second one.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here