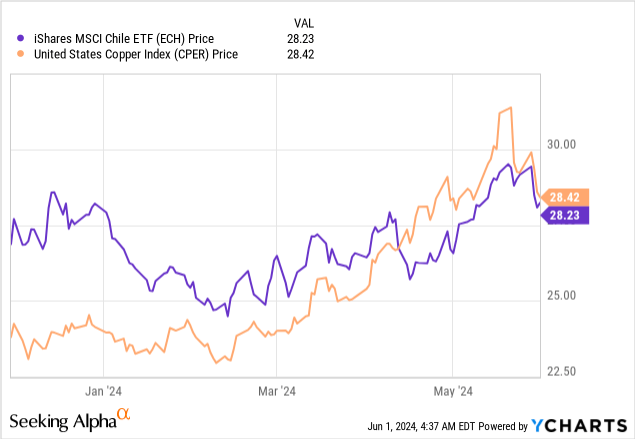

Chilean stocks went through a challenging second half of 2023, as many of the concerns I outlined in my last piece on iShares’ MSCI Chile ETF (BATS:ECH) (see ECH: Don’t Chase The 8% Yield Offered By Chilean Stocks) weighed on performance. 2024 has taken a different turn, however, and ECH is now very close to clawing back losses from recent months. It’s no coincidence that this run has coincided with a cyclical upturn in copper prices – despite the absence of copper producers in ECH’s portfolio, underlying Chilean earnings strongly correlate to copper prices by virtue of the metal’s relevance to the broader economy. This effect extends to the peso as well, so the benefit from higher copper prices has allowed investors to benefit from both legs (price and currency appreciation).

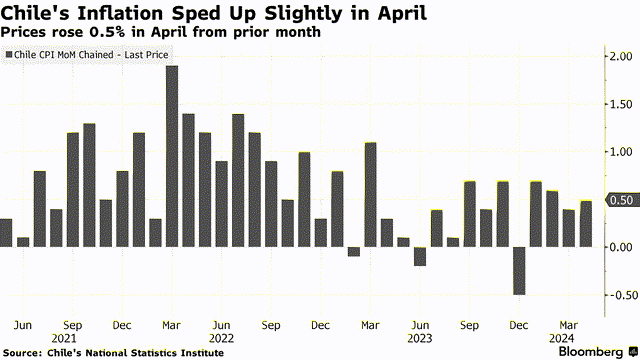

The issue for me is that, to a large extent, the positive drivers of equity performance remain cyclical, while the negative drivers are structural (think political instability, long-term economic and corporate earnings growth potential, etc). It’s also worth keeping in mind that Chile’s monetary easing tailwind is nearing an end, with ‘sticky’ inflation forcing the central bank (i.e., the ‘BCCh’) to pull back on its pace of rate cuts. This, in turn, presents a less than supportive outlook for the non-bank parts of ECH’s portfolio.

Bloomberg

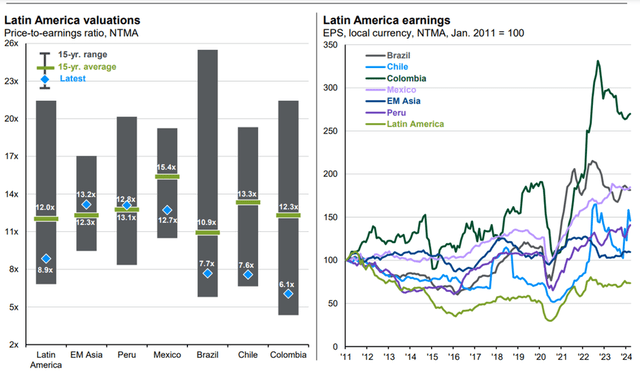

Bulls will perhaps point to the valuation, currently at a seemingly discounted ~8x forward P/E (~11x trailing), as reasons to own Chile here. The catch, however, is that the ECH earnings base is also very cyclical. Last year’s low to mid-double-digits % YoY earnings decline is a case in point, as are consensus expectations for low-single-digit % growth this year.

The implication here is twofold. Firstly, a cyclical earnings profile is harder to underwrite (and therefore warrants a bigger discount to compensate). Secondly, a cyclical portfolio looks ‘cheap’ on P/E when its constituents overearn (and vice versa). And perhaps most importantly, the compounding rate of Chilean corporate earnings through the cycles has been disappointing – a fact reflected in ECH’s poor track record. Net-net, I don’t see a particularly compelling risk/reward here and will continue to steer clear.

JPMorgan

ECH Overview – The Largest and Most Liquid Chile Tracker

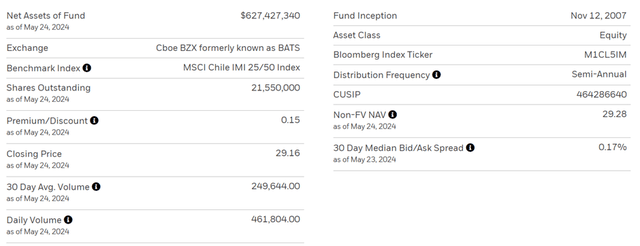

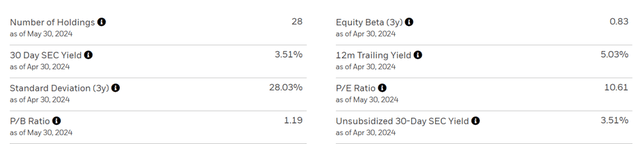

iShares MSCI Chile ETF, which tracks the country’s largest and most liquid names via the MSCI Chile IMI 25/50 Index, remains one of the few single-country plays on Chile. There is very little breadth here, as the 28-stock portfolio highlights, though the concentration limits (a 25% cap on single stocks and a 50% cumulative cap on all >5% holdings) help. But ECH is hard to beat on cost with an expense ratio of ~0.6%. Liquidity is also relatively good for an emerging market fund, though the current ~17bps median bid/ask spread is slightly wider than before – despite a bigger asset base.

iShares

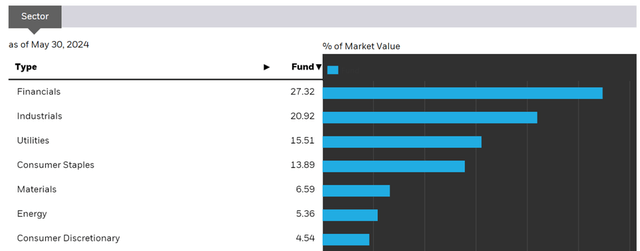

ECH Portfolio – Some Reshuffling but as Concentrated as Ever

While Chile’s economy leans heavily on copper, ECH’s sector breakdown skews a lot more toward Financials (now at an upsized 27.3%) than Materials (6.6%). The reason being that the country’s largest copper mining company, Codelco, is state-owned, while the other major miners are multinationals. Of note, other sector exposures like Industrials (down to 20.9%), Utilities (down to 15.5%), and Consumer Staples (broadly unchanged at 13.9%) also take up a larger share of the ECH portfolio.

iShares

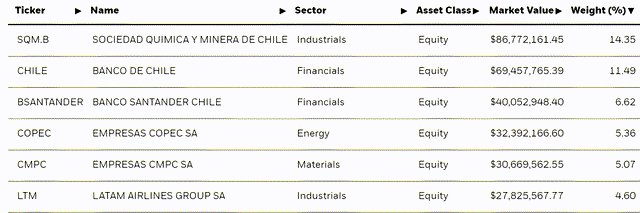

As for the single-stock breakdown, the fund keeps its portfolio relatively small at 28 holdings, which also means it’s fairly concentrated in % terms. At the top of the list remains Sociedad Quimica Y Minera de Chile SA (SQM), Chile’s staple lithium and chemicals producer, though its contribution has been downsized to 14.4% amid cyclical headwinds. In contrast, the country’s two big banks, Banco de Chile (BCH) and Banco Santander-Chile (BSAC) continue to gain share at 11.5% and 6.6%, respectively. The other notable gainers are energy company Empresas Copec (5.4%) and pulp and paper company CMPC (5.1%). Despite the reshuffling and slightly broader portfolio, ECH’s top-five concentration of ~43% still makes it a highly concentrated fund.

iShares

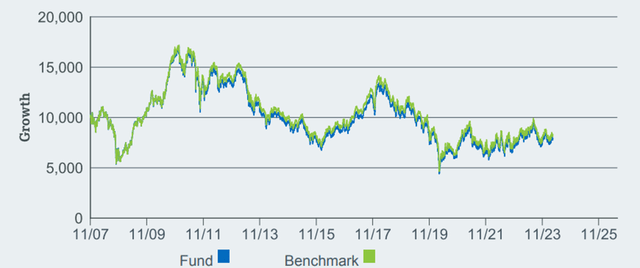

ECH Performance – Limited Shareholder Value Creation Through the Cycles

ECH may not have started the year strongly, but the recent rally in copper has reversed its fortunes and the year-to-date return has flipped slightly positive as a result. Still, it’s worth noting that the fund has delivered negative total returns across all other timelines. Over the last year, the total return stands at -1.8%, while over longer five and ten-year timelines, ECH’s annualized return stands at -5.1% and -2.5%, respectively.

iShares

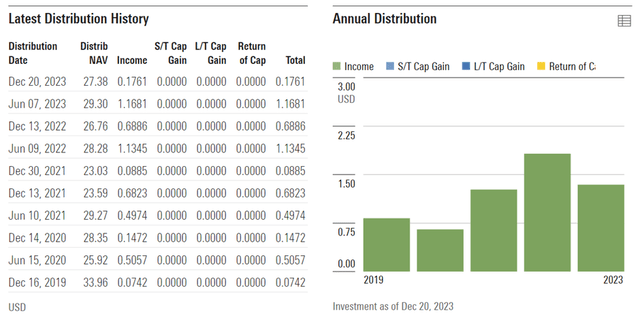

As for the distribution yield, which had run as high as ~8% when I last covered the fund, the payout has normalized a lot lower in recent quarters. As I highlighted in my prior coverage, the yield tends to fluctuate in line with cyclical swings, so it’s perhaps no surprise that ECH now offers a much lower 3.5% 30-day SEC yield (~5% trailing twelve months). If we do see a cyclical downturn, expect this yield to move even lower, though the recent uptick in dividend-paying bank holdings should also keep an income ‘floor’ in the meantime.

Morningstar

Similarly, the cyclicality here has also led to ECH’s P/E valuation more than doubling from when I last covered the fund. On a trailing basis, ECH is now priced at ~11x earnings and ~8x forward, while relative to book value, the fund trades at a ~20% premium. Given the lack of a through-cycle earnings growth track record and the rather lackluster forward projections, there isn’t a lot of value on offer here.

iShares

Fade Chile’s Copper Bounce

For all the positive news flow around copper in recent months, it’s perhaps easy to forget the many reasons not to invest in Chile. Yes, there’s a decent yield here, albeit a much smaller one than before. But at the current ~11x trailing P/E, investors aren’t getting much bang for their buck, especially when you factor in the earnings growth trajectory. Pending a meaningful reset of expectations following the latest copper rebound, I don’t see a compelling reason to own ECH here.

Read the full article here