Overview

EchoStar Corporation (NASDAQ:SATS) is a renowned global provider of cutting-edge satellite communication solutions. As a premier satellite owner/operator, EchoStar Satellite Services boasts a fleet of 10 satellites, delivering satellite communications infrastructure and solutions to media and broadcast organizations, enterprise customers, and U.S. government and military service providers.

However, EchoStar’s stock performance has not been favorable. Over the past five years, the company’s share price has dropped by 65%. In the last three months alone, the share price has declined by 20%. One of the key reasons for this decline is the decrease in revenue. According to the company’s financial reports, there has been a decrease in consolidated net income attributable to EchoStar common stock. This decrease in revenue can be attributed to various factors such as intense competition in the satellite and broadband industry leading to significant pricing pressures. Additionally, EchoStar has also witnessed a decline in broadband subscribers, which has impacted its financial performance in recent years.

Earnings Snapshot

EchoStar Corporation recently announced its financial results for the second quarter and first half of 2023. The company reported a decrease in revenue, with consolidated revenue of $453.1 million for the three months ended June 30, 2023, and $892.7 million for the six months ended June 30, 2023. Net income for the same periods was $9.1 million and $36.9 million, respectively. The decline in revenue can be attributed to lower service revenues and an impairment of a certain equity investment, among other factors.

Additionally, the company experienced a decline in broadband subscribers, with Hughes broadband subscribers totaling approximately 1,122,000, declining 106,000 from December 31, 2022. EchoStar is set to report earnings on November 1st when investors will closely watch the growth in broadband subscribers.

Compressed Valuation

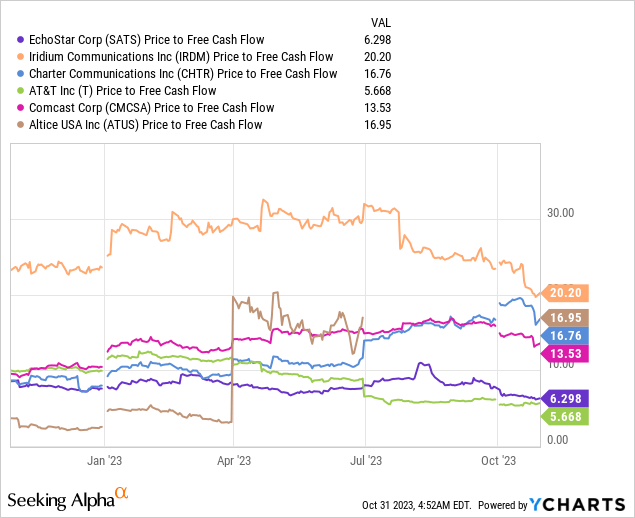

EchoStar’s margin pressures due to heightened competition are well reflected in its compressed valuation. In this regard, EchoStar trades at a significant discount compared to satellite-and-communication peers such as Iridium Communications (IRDM), Charter Communications (CHTR), or Comcast (CMCSA). However, it is important to point out that given the smaller scale of EchoStar, its free cash flow and earnings are more susceptive to downside fluctuations, which is partially reflected in the significantly lower valuation. Thus, EchoStar currently trades at 14 times forward P/E ratio, compared to AT&T (T), which trades at just 6 times forward earnings. Nevertheless, EchoStar’s debt load is more manageable, with just $1.6 billion in debt against $1.9 billion in cash, compared to AT&T, which currently has over $155 billion in outstanding debt.

Overall, EchoStar’s current valuation reflects negative sentiment concerning its ability to grow earnings over the next few years, due to intense competition from larger broadband players, which could lead to significant margin pressures for EchoStar.

Takeaways

While EchoStar currently trades at a seemingly favorable valuation, it faces formidable challenges. Notably, the company grapples with fierce competition from established industry players. Furthermore, significant risks are associated with EchoStar’s contractual obligations for satellite capacity. Should existing customer contracts be prematurely terminated before their scheduled expiration, there’s a looming threat that EchoStar might not rake in enough revenue to offset the costs associated with satellite capacity.

However, if EchoStar is able to overcome some of these challenges, shares could jump due to its substantially compressed valuation.

Read the full article here