Multifamily apartment REIT, Elme Communities (NYSE:ELME), is down nearly 18% since my last update on the stock where I rated shares as a “hold.” At the time, ELME was trading just off their Q2 results, which were generally positive minus the downward revision in full-year guidance. It was this downward revision that shaped my views on ELME’s outlook.

The outlook appears to have stabilized since my update. In their Q3 results, management reaffirmed full-year guidance and also provided positive commentary surrounding their portfolio metrics. In addition, the management team updated investors on a significant acquisition in their fast-growing Atlanta metro market.

At 13x forward funds from operations (“FFO”), shares still trade at a premium to other similar-sized multifamily peers. Centerspace (CSR), Independence Realty Trust (IRT), and NexPoint Residential (NXRT), for example, all trade in the 10x range. I’ve elaborated in past coverage why the premium is justified. But in the current market environment, I continue to believe investors would be better served by directing capital to the more discounted players in the peer group. I, therefore, remain neutral on ELME following Q3 results.

ELME Key Stock Metrics

ELME is currently forecasting 2023 core FFO to land at a midpoint of $0.98/share. Based on this estimate, shares currently command a forward multiple of FFO of just under 13x. This represents a premium to similar-sized peers, which currently trade at around 10x.

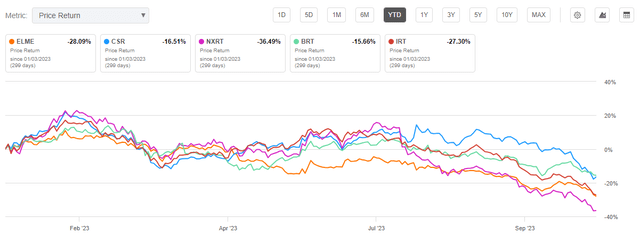

YTD, shares have lagged behind the peer set, with losses of 28%

Seeking Alpha – YTD Share Price Performance Of ELME Compared To Peers

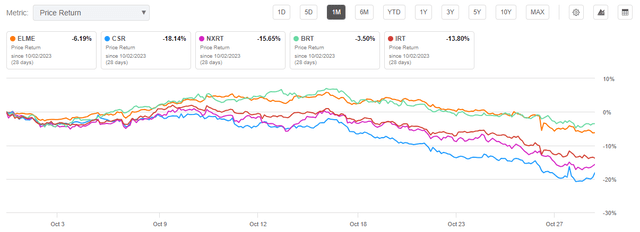

The performance is better over the past month, with much of the peer set down in the double-digits compared to ELME’s upper-single-digit percentage losses.

Seeking Alpha – 1-MTH Share Price Performance Of ELME Compared To Peers

The weakness in the share price is despite solid portfolio metrics, which include same-store average occupancy levels in the mid-90% range and high portfolio retention of approximately 60%.

ELME also continues to generate a healthy return on investment (“ROI”) of about 14% on their value-add renovations, a significant aspect of their reoccurring operations. For the year, they are projecting the completion of 300 renovations, all of which should garner similar returns in line with their yearly average.

Summary Of ELME Q3 Results

In Q3 ELME reported total core FFO of $0.24/share, up 4% YOY. Overall net operating income (“NOI”) was up a similar 5%.

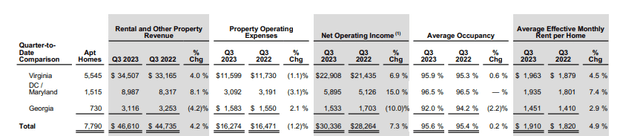

In the same-store population, NOI grew 7.3%, led higher by rental revenues, which grew 4.2%. This was supplemented by a more favorable operating environment, with expenses down 1.2% YOY. Sequentially, expenses were down an even greater 2.9%.

ELME Q3FY23 Investor Supplement – Summary Of Same-Store Operating Performance

Growth in rental revenues was supported by a 4.9% increase in average effective monthly rents per home. Additionally, ELME realized rental spreads of 5.1% on renewals and 0.1% on new leases. And despite the continued rental rate growth, retention and occupancy both held up firmly.

Same-store retention was 61%, while average occupancy remained in the mid-90% range, at 95.6%, up 20 basis points compared to the same period last year.

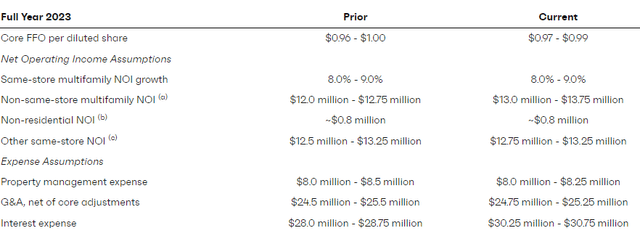

Looking ahead, the management team firmed up their full-year guidance by narrowing their expectations for full-year FFO. Elsewhere, guidance for non-same-store NOI was revised higher by +$1.0M due primarily to the contributions from their newly acquired portfolio of properties in their Atlanta market. At the same time, the increased NOI expectations were also paired with higher expectations for both G&A and interest expense.

ELME Q3FY23 Earnings Release – Summary Of Full-Year Guidance

The Druid Hills Acquisition

Just prior to the quarter end, ELME closed on the acquisition of a 500-home apartment complex in their Atlanta market. The total cost of the acquisition was +$108M.

Following the acquisition, ELME’s net debt multiple ticked up to 5.7x from 4.8x at the end of Q2, while available liquidity declined to +$560M from +$680M prior to the acquisition. Despite the uptick in leverage, total debt levels remain within targeted levels. And the company’s debt profile remains favorable, with no secured debt and no debt maturities until 2025.

Offsetting the additional leverage is the expected benefits of the transaction, which include further exposure to the fast-growing Atlanta market. The homes also fit ELME’s Class-B value-add strategy, thereby providing ELME the opportunity to renovate all 500 homes in the portfolio.

At present, the Class-A alternatives in the surrounding area are priced at a 21% premium to ELME’s current in-place rents, according to commentary from ELME CEO, Paul McDermott. Provided the ROI on renovations remains around the 15% mark, ELME should, therefore, have an attractive opportunity to drive rents in future periods on these properties.

Finally, the Druid properties also are situated in a supply-restricted location. Since 2021, for example, there has only been one new delivery into the market. And there is minimal construction within a 3-mile radius as well. This should provide an additional anchor on the market’s rate growth potential.

Is ELME Stock A Buy, Sell, Or Hold?

The Druid Hill acquisition provides ELME with an additional growth lever in a top-performing market. While the acquisition did come at the expense of higher leverage, ELME’s debt profile remains more flexible than its peer set.

ELME should also benefit through natural rent growth with the properties, as current rent levels are significantly discounted to the market median. The homes also possess a value-add opportunity, in line with the company’s strategy.

ELME’s quarterly results elsewhere were largely in line with expectations, with stable occupancy and retention levels and positive leasing spreads on renewals. For prospective renters, ELME’s properties remain attractive in relation to their Class-A counterparts. A constrained supply outlook in ELME’s operating regions also provides the company with the ability to continue driving rents. And their tenants appear adequately positioned to absorb the increases, given their properties sport a current average rent-to-income ratio of approximately 24%.

For investors seeking new or additional positioning, ELME provides a well-covered dividend payout that is currently yielding over 5%. Consensus Wall Street estimates also peg shares fairly valued at about $20/share, representing material upside potential from current trading levels.

A rally to those levels in the current market environment, however, appears unrealistic. In my view, the stock will likely continue to trade towards the bottom end of its 52-week range and will likely be passed over by peers, IRT and NXRT, who each trade at a significant discount despite similar operating performance. More concrete results from ELME’s recent property acquisition may help shape a more bullish view on the stock. But until then, I view shares best left on hold.

Read the full article here