Embracer (OTCPK:THQQF)(OTCPK:EBCRY) has been making moves. In addition to the relatively uneconomical Saber Interactive and Gearbox Entertainment disposals, the latter to Take-Two Interactive (TTWO), which salved the market’s leverage concern that sustained the sharp Embracer discount, they’ve also announced a strategic shift whereby they plan on splitting off the businesses. We’d watch out for RemainCo. As focused on in our last analysis, they’ve been really gutted with the disposals, and are really counting on the Middle Earth MMO, which, as we also mentioned in our last article, is not guaranteed to be well received. With some sensitivity analysis for the spun off and residual elements, you’ll know what to buy and sell as things split off. Basically, RemainCo will be the AAA studio and the most concerning entities for shareholders, with tabletop in Asmodee and mobile and other AA and indie gaming in Coffee Stain and Friends. With the two spinoffs slated for over the next 12 months and/or in calendar year 2025, it’s going to be important to know whether markets are missing something in the spun-off issues. Spinoffs tend to be great opportunities to make money and buy things before markets have understood what properties are in which securities.

Quick Look At Quarterly Results

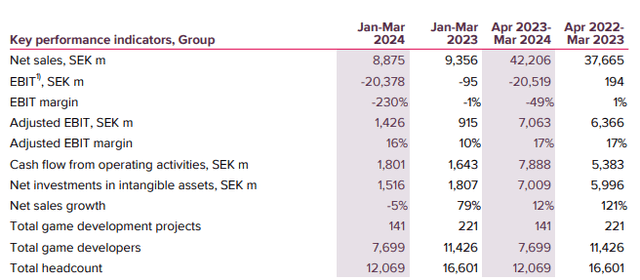

So far, there has been recent closure on the Saber Interactive disposals, but it seems only after the close of the FY books. Gearbox is not done yet and is expected to close next quarter. We are still looking at a complete Embracer. Sales are down slightly, but the major headcount cuts have meant a decent growth in adjusted EBIT.

Headline IS (FY PR)

The difference between EBIT and adjusted EBIT is a heap on non-cash write-downs, including losses on investments for both Gearbox and Saber Interactive, which they disposed of at a loss. Even Asmodee assets have been terribly impaired by almost 7 billion SEK in the annual impairment tests.

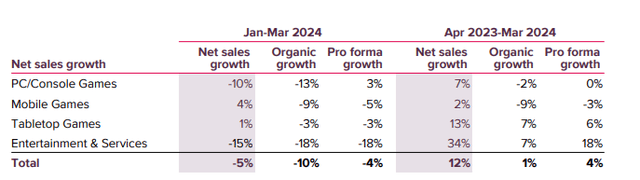

Segment Sales (FY PR)

For sales evolutions by segment, YoY evolutions are bad for the Q4 on an organic basis in the PC gaming segment. Mobile was bad for the year but not for the quarter, and E&S was bad for the quarter but not for the year. E&S declines are due to tough comps, since they had fewer animation releases.

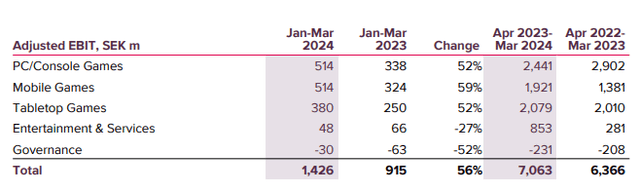

Segment Adjusted EBIT (FY PR)

Profits are up in general from the meaningful layoffs that have been happening across segments.

There is stuff going on for E&S. A new Gollum movie with New Line Cinema (Peter Jackson) will mean royalties for Embracer. The LoTR MMO is also coming at some point from Amazon, which will also mean royalties. Could be years for that, towards late 2020s. They are also a LoTR musical coming into production as well as a Rohirrim anime as the property gets milked. Dark Horse is doing alright with Berserk and is managing growth. The Avatar: The Last Airbender graphic novels are also performing well, helped by the live action series release, which galvanised fans into buying more Avatar merchandise.

Tabletop games, which include great properties like Catan, decelerated a bit now after a year of holding the fort, but Star Wars: Unlimited just released and should generate some activity in the coming quarter. Demand had outpaced supply. There are more sets coming, things are looking alright here.

For mobile games, LiveOps continues to drive the portfolio. Cash flow focus at DECA means weaker growth from there. Overall, the quarter’s performance has been good here.

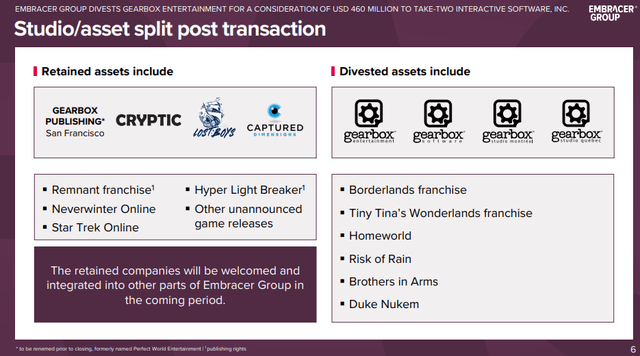

For PC gaming, there was pro forma growth when excluding Saber Interactive from last year’s comps. But otherwise there are clearly declines, and Saber was coming out with the new 40k game, Space Marine 2, which would have been a major element in this year’s pipeline. Gearbox will be gone soon as well, taking with it most of the valuable IPs except for Remnant and Hyper Light Breaker, the sequel of Drifter. As we discussed in previous coverage, it was South Park and Tomb Raider that held up the quarter. There was also the Star Wars: Battlefront Classic Collection, which was another fail where the company took games that were perfectly good and had longstanding followings and found a way to anger fans. But it has performed so far.

Remaining Gearbox Titles (Gearbox Disposal Pres)

The growth engine in the PC gaming segment is gone. The upcoming year will be quiet here, and we expect nothing from the segment’s topline in terms of growth. Gigantic, the MOBA game from some years ago, is releasing, but now it won’t be free. It was a good game, but it wasn’t popular then, so it won’t be now, is our bet. The only good stuff that’s left is Breaker, Kingdom Come: Deliverance 2, Gothic Remakes. Kingdom Come hopefully doesn’t drop the ball after a strong first entry. Gothic remakes are cool, but the markets might not be that large there. Breaker should be solid, but it’s a thin pipeline.

Spin-offs and our Bottom Line

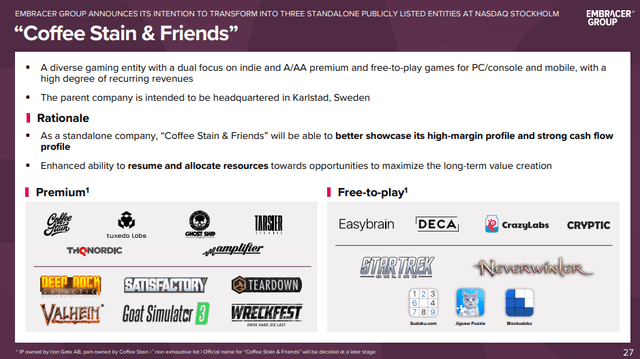

There is going to be a major change in the company at some point this year, where Asmodee, the tabletop segment, is going to get spun-off to shareholders, possibly this year. So is Coffee Stain and some other businesses (they’re calling it Coffee Stain and Friends), namely a lot from the mobile gaming segment.

Coffee Stain & Friends Properties (Spin-off Pres)

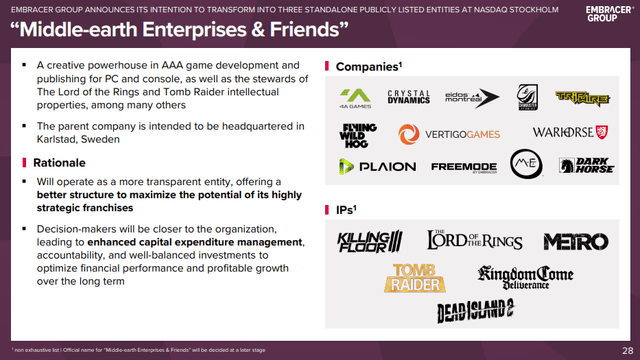

RemainCo (Middle-earth Enterprises and Friends) will be the AAA titles, and a thinning pipeline lacking Borderlands and Space Marine 2.

RemainCo Properties (Spin-off Pres)

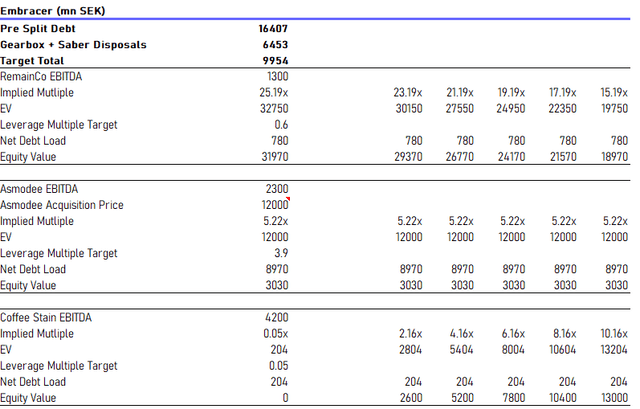

The company has given us pro forma data and debt targets for the planned spun off elements. We also have the disclosure of net proceeds from Saber and Gearbox. With debt targets for RemainCo and Asmodee, we can imply debt load for Coffee Stain and Friends from the current group’s debt load. Also, spin-offs shouldn’t create value, so we have the current market cap as a reference for what the total stock values of the spun off elements should be worth.

Our Valuation Table, with Asmodee Set at 12 Bn SEK (VTS)

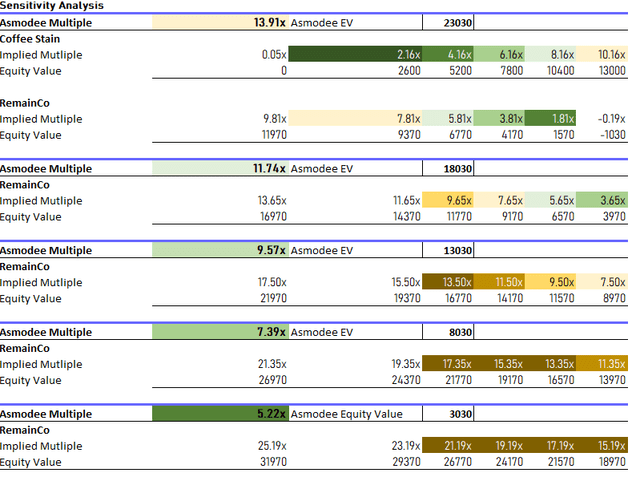

We have a fixed Asmodee multiple that we use in sensitivity analysis. Here the proposed EV for Asmodee is low, but when it was acquired, it was at around 32,000 million SEK, which is our upper band for the sensitivity analysis. The total of each company’s value needs to be today’s market cap at 35 billion SEK. Fixing Asmodee’s multiple, we can see what the implied multiples will be for the other businesses depending on how the market distributes Embracer’s valuation to each of the components, which we cannot know until the spin-off happens. That way, we have some framework for knowing what to buy and sell at the moment that the spin-offs happen, first for Asmodee and probably at a later date for Coffee Stain and Friends, although it may all happen on the same day.

Sensitivity Analysis for Valuation Scenarios of Spun off elements, based on today’s market cap and fixed value assumption (VTS)

Based on comps from our previous article, where we believe Embracer is a discount company compared to the best and the brightest in gaming, we have highlighted the favourable valuations as green in our snapshot sensitivity analysis, which captures a range of possible valuations for each property at spin-off (obviously we cannot know how markets will react in the spin-off days). Depending on what the components are worth at spinoff, we’d buy the green and sell the brown. The colour intensity matches how favourable/unfavourable we think the valuation is based on comps.

In all, the disposals from RemainCo have us requiring pretty large margins of safety to take it on, since we think their growth is pretty jeopardised and the economics of game development are really tough right now. We don’t expect them to launch many great titles from nothing, and that they’ll have to acquire studios that have been successful in going from AA to AAA level, where AAA economics are tougher to deal with, spurring massive layoffs as they adjust to structural challenges due to larger budgets, more risk, more short-termism and tougher human capital challenges. We think that the upper end of fair multiples here are around what the Embracer Group as a whole is currently valued at, 4x EV/EBITDA.

Coffee Stain and Friends include some AA and indie studios, so there’s a chance of performance there since they’re going to be more independent and closer to the consumer, and unlikely to disappoint in the way that AAA have started to systematically do. We have them at fair values at higher multiples than RemainCo, around 6-8x EV/EBITDA.

Asmodee, being the more resilient and consistently growing segment even after the pandemic, is the business we chose to fix a value for, also because it was acquired by Embracer relatively recently at around 32 billion SEK. Its properties are pretty unique, and they have a leading edge in tabletop that makes it more marquee.

With spun off elements typically spending some time as independent entities before price discovery happens, we’d expect that opportunities may arise in their valuations more than with RemainCo, particularly as RemainCo was the set of businesses that were gutted the worst by the disposals meant to tackle the leverage, which was the market’s primary concern based on the run-up in prices, even though the disposals were at a loss.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here