Investment Thesis

The energy sector has been an interesting space for the last few years.

First, Europe began seeking alternative energy partners after Russia invaded Ukraine, causing prices to spike. American companies benefited massively from this. Now, with developing technologies like artificial intelligence, we need more power and more commodities to produce power.

Enbridge (NYSE:ENB) (TSX:ENB:CA) facilitates the transportation of these commodities from their extraction points to their destinations. The company has strong long-term drivers. Unfortunately, this is not the best time to invest in this company.

The company struggles to generate higher returns on its assets, and the high interest rate environment hinders growth investments. Additionally, the dividend is a big burden on the credit structure, and Enbridge will have to choose between cutting its dividend or continuing to raise cash at the expense of its shareholders.

Given these concerns and historical multiples, I believe the stock is accurately priced. Therefore, Enbridge receives a “Hold” rating from The Alpha Oracle.

Business Description

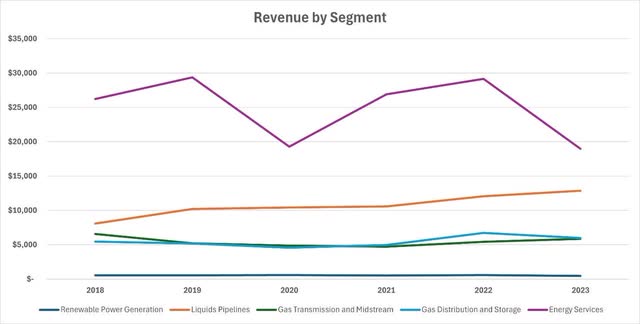

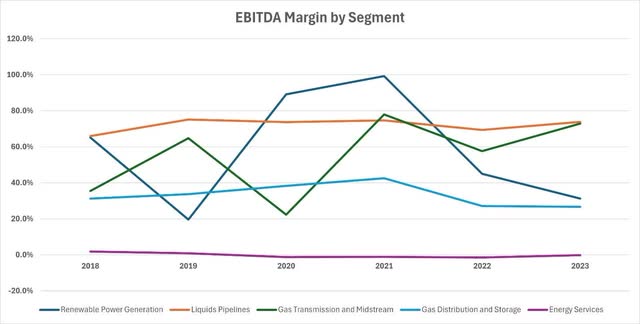

Enbridge is a leading oil and gas infrastructure company. Its diversified asset base allows it to benefit from multiple revenue sources and regions. The company operates under five business segments.

The largest segment in terms of revenue is Energy Services. Through this segment, the company provides physical commodity marketing and logistics services to refiners, producers, and other customers. Although revenue is relatively high, this is a very low profitability business. The EBITDA margin has consistently been around 0% and has been negative since 2020.

This year, Enbridge decided to discontinue this operating segment. Some parts were included in the Liquids Pipelines business in 2023 (hence the revenue drop) and the remainder will be reported in eliminations and others from now on.

This brings us to the second-largest segment: Liquids Pipelines. The company owns pipelines and terminals throughout North America that transport and export various types of crude oil and other hydrocarbons. With its established asset base, the company earns revenue based on the volume that uses its infrastructure. The footprint of this business is extensive across North America.

Following Liquids Pipelines in terms of revenue are the Gas Transmission and Midstream, and Gas Distribution and Storage segments. While the Transmission and Midstream business operates natural gas pipelines and gathering and processing facilities in North America, the Distribution and Storage business focuses specifically on serving residential, commercial, and industrial customers in Ontario and Québec.

The smallest business segment is Renewable Power Generation. The company has investments in solar, wind, geothermal, and waste heat recovery assets. However, this segment is very small and does not significantly drive the overall business.

Charts showing revenue and EBITDA margin by segment can be found below.

S&P Capital IQ

S&P Capital IQ

Although the company has not grown much compared to historical levels, Enbridge’s established infrastructure and presence throughout the North American geography has ensured stable returns over the last years.

Since 2018, it has achieved an ROA of above 7%, with the exception of 2022.

S&P Capital IQ

S&P Capital IQ

Business Drivers

The biggest long-term thesis for this business remains the increasing energy trend, driven by two main factors.

The first factor is the rapid pace of technological advancements outpacing energy production globally. Especially this year, people started understanding the potential of artificial intelligence, and the infrastructure requirements for it. That’s why data center growth has been immense. This is expected to continue for years to come.

And it’s not only AI. In general, technologies like the Internet of Everything, electric vehicles, big data, and smart homes all generate data that needs to be stored and processed. This requires an increasing amount of data centers, which means increasing electricity consumption.

In 2023, the US generated 43% of its electricity from natural gas. Fossil fuels, in total, accounted for 60% of electricity production, while renewables were used for 21%. As the need for more power grows, North America will need more natural gas and renewable energy assets – energy sources Enbridge has or helps transport.

The second factor is less discussed nowadays. However, Europe is still looking for a partner it can source energy from. It has been made clear that Russia is not this partner anymore. And with Russian gas unavailable, the US stands out as a natural partner.

This might increase the demand for American natural gas for the next decade, leading to higher utilization of Enbridge’s infrastructure.

Markets Understand The Long-Term Value

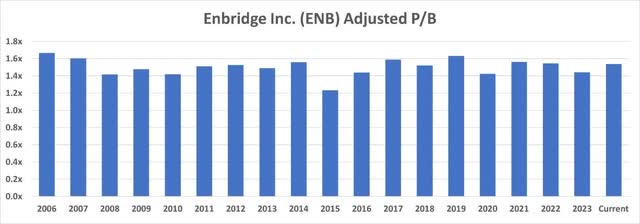

I believe investors do an amazing job understanding the value of this company. As a typical energy utilities company, Enbridge earns more the more assets it has, but it is difficult to increase the return on assets, as seen from the chart shared above.

Historically, the market has priced the company within a narrow adjusted price-to-book range. This implies that the expected asset growth rate and return on assets do not change significantly over time.

S&P Capital IQ & Author

From an assets perspective, the stock price is a function of the P/B multiple and asset growth. As the multiple has remained flat over the years, the Enbridge stock has primarily been an asset growth story so far. Let’s examine this.

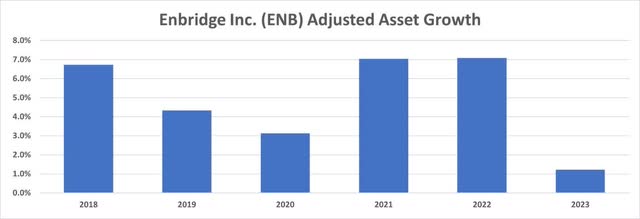

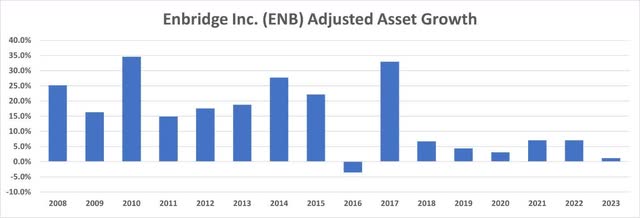

Below is Enbridge’s asset growth chart since 2008. The company grew a lot faster before 2017 compared to years after. The asset CAGR was 18% between 2008 and 2017, while, it has been 5% since 2017.

S&P Capital IQ

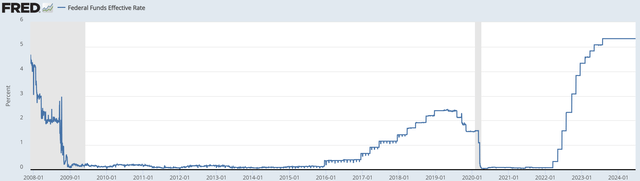

Unsurprisingly, times of high asset growth coincide with low interest rates, and vice versa. After rates declined rapidly in 2009, they were near 0% until 2016. This is when Enbridge grew aggressively with access to cheap financing. However, when interest rates started increasing in 2016, this growth slowed down.

FRED – Federal Reserve Bank of St. Louis

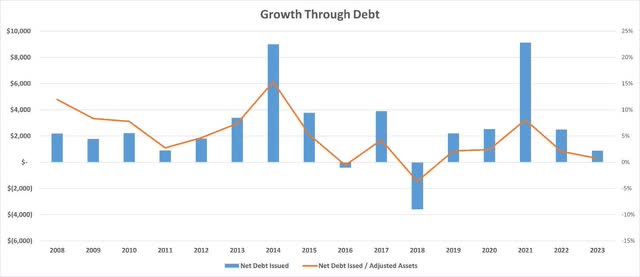

We can also see how much of this growth was financed by debt issuances since 2008. The chart below shows the nominal amount of net debt issuances, as well as net debt issuance as a percentage of adjusted assets, to show how much percentage growth the financing allowed. Expectedly, the average contribution of debt financing to asset growth declined after 2016.

S&P Capital IQ

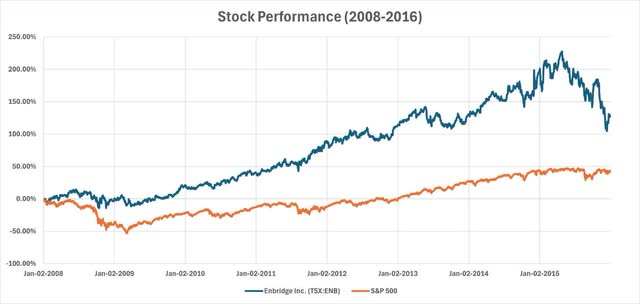

This is all that matters. It’s not easy for the company to earn more on its assets, so it grows whenever it has access to cheap financing. The market is aware of this, and awards the company for growth, while it waits for the growth period when rates are high. Below, you will see the stock performance in high growth and more moderate growth environments. The stock price kept increasing until 2016 and has been flat since then.

S&P Capital IQ

S&P Capital IQ

This is why I believe right now, when rates are higher for longer, is not the ideal growth environment for Enbridge. Therefore, I don’t expect a strong appreciation in the stock price.

Dividend May Be At Risk

The dividend yield on the stock is currently 7.73%, attracting many investors. However, the credit structure of the company is worse than it appears.

Enbridge paid $7.6 billion in dividends in 2023. In that same year, the company generated $14.2 billion in cash from operations but invested back $6 billion of these earnings. Based on these metrics, the dividend might seem sustainable.

However, the company has big debt maturities coming up in each of the next several years. Enbridge will have to refinance at higher rates, resulting in higher interest expenses each year, or issue common stock as they did last year and dilute existing shareholders.

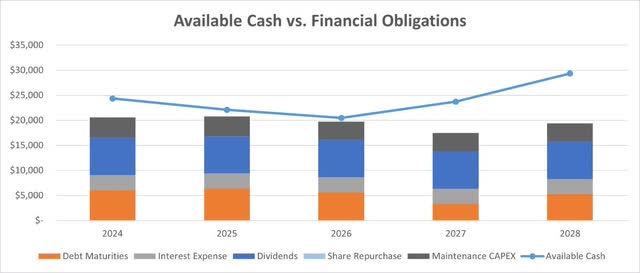

Even if they manage to have $7.5 billion each year for the next five years, based on my projections, not much cash will remain after covering financial obligations. Have a look at this scenario below. The line represents cash at hand at the end of the period, and the stacked bars represent financial obligations.

S&P Capital IQ & Author

While it is not unrealistic for the company to raise this amount of cash, it will be costly. Issuing debt or common stock to pay a large dividend is not a sustainable business model.

If the company cuts its dividend, the stock price will surely fall. Many investors see this name as a dividend play and would not like that scenario.

Conclusion

I like the business model Enbridge has developed. The company has built its scale over time and established a strong presence in North America, making it a profitable enterprise. I also believe long-term growth can be achieved as the fundamental business drivers remain intact.

However, this is not the time to invest in it. The stock has historically performed badly when interest rates are high, as debt has been the primary means of financing growth. The market is aware of this and prices the stock accordingly.

Additionally, issuing debt or common stock to keep paying dividends is not a sustainable business model. The company will either cut its dividend or will continue to raise cash, which would hurt shareholders.

That is why I am assigning a “Hold” rating to this company. That means I think investors should stay away from this stock for now. This idea can be reconsidered when the growth environment improves.

Read the full article here