I recently initiated my coverage of US-midstream giant Energy Transfer (NYSE:ET) when I assigned it an Overweight rating based on 1) its strong track record of organic and inorganic growth, 2) a sector-leading and well-covered dividend yield and 3) a heavily discounted valuation. The company reported its Q1 results on May 8, revealing a very strong start to the year, both operational and financial. Boosted by the Crestwood acquisition, transported volumes rose significantly with crude volumes surging more than 40%, in turn driving revenue and DCF growth of 14% and 17% YoY. On the back of a strong quarter and expecting further strength, management also upgraded its full-year EBITDA guidance by ~3-4% to now expect up to $15.3B.

With the recent results highlighting the company’s continued strong execution, I reiterate ET at Overweight and slightly raise my price target to $20/unit to account for raised estimates and a 3% raised annualized distribution. Risks remain in commodity market downturns as well as unplanned maintenance needs across the portfolio, which could temporarily depress earnings.

[Note: Peers refer to Enbridge (ENB), Enterprise Products Partners (EPD), Williams Companies (WMB), ONEOK (OKE), Kinder Morgan (KMI) and TC Energy (TRP). All financials and company projections taken from the most recent 10-Q and Q1 earnings call.]

Key Discussion Points

Stellar Q1 with DCF up 17% and crude volumes surging 44% YoY on new investments, Crestwood acquisition

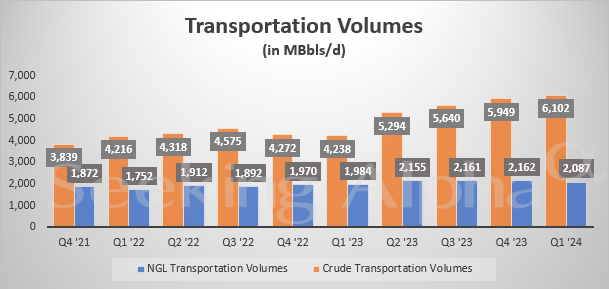

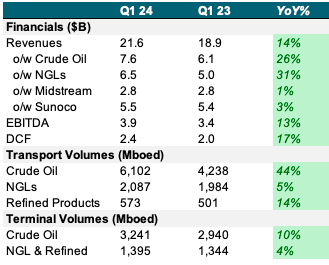

ET reported a very strong Q1 with revenue growth across all of its divisions, which was driven by significantly stronger volumes in both transportation and terminals. Most notably, crude oil transported volumes surged 44% YoY to over 6,000Mboed (a new record for the company) while NGLs grew 5% and refined products (gasoline, diesel) were up 14% vs Q1 23. YoY terminal volume growth came in slightly softer, with crude oil up 10% and NGLs and refined product climbing 4%. Management attributes this throughput growth largely to new investments and the company’s recent acquisition of Crestwood Equity Partners, closed in late 2023.

Seeking Alpha

Driven by strong operating results, total consolidated sales came in at $21.6B for Q1, up 14% YoY with segment sales in crude oil and NGLs surging 26% and 31% respectively. Midstream sales grew 1% as gathering and processing volumes remained largely flat YoY while revenue from ET’s stake in Sunoco (SUN) was up 3% YoY. EBITDA grew 13% YoY as margins decreased slightly from 18.1% to 18% while quarterly DCF surged 17% to ~$2.4B.

YoY Matrix (Company Filings)

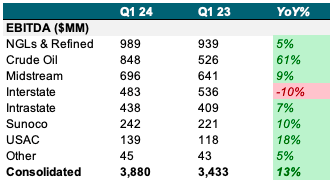

Breaking earnings down by segment, the majority of EBITDA gains came from crude oil, with segment EBITDA up 61% YoY to $848MM. Notably, interstate represented a net headwind to consolidated EBITDA with segment earnings falling 10% YoY largely related to unplanned maintenance and lower proceeds from natural gas sales.

YoY EBITDA Matrix (Company Filings)

I do want to note that the company formally missed on profit estimates, recording quarterly EPS of $0.32 vs $0.39 expected by Wall Street. However, given the fact that midstreams do not really trade on EPS given sector accounting practices and the significant amount of debt in the capital structure, I do not find the miss concerning. I also want to note that lower than consensus EPS was majority-driven by additional units issued in the Crestwood acquisition, and actual net profits were up 11% YoY.

Full-year guidance raised to now expect EBITDA of $15-15.3B vs. previously $14.5-14.8B

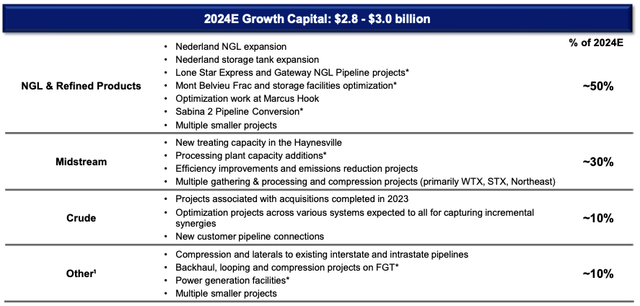

As part of the release and in line with strong growth seen during Q1, management raised its forecast for FY24 EBITDA by ~3-4%. At the midpoint of guidance, ET therefore now expects an 11% YoY expansion in EBITDA. Management also slightly adjusted its guidance for annual growth capex to now lie between $2.8B and $3B, of which roughly half is to be spent on further building out the company’s Nederland Texas hub and the Lone Star Express pipeline. Crude oil and other projects account for ~10% respectively, while midstream will receive ~30% of planned investments, largely concentrated on additions to ET’s Haynesville basin gathering and processing capacity.

Energy Transfer IR

In line with higher expected earnings, ET management also announced an increase in quarterly distributions to $0.3175/unit, implying a ~3.3% growth vs the prior year’s Q1.

Management hints at more M&A in the future

An interesting topic that management briefly touched upon during the conference call was the potential for more consolidation in the US midstream space. While the large headlines in energy M&A have recently been definitely more on the E&P side, I do note that ET has a strong track record of inorganic expansion, most recently acquiring Crestwood during late 2023. Responding to an analyst question, management noted it was consistently monitoring markets for any potential accretive targets:

We still fully intend on evaluating various opportunities as we look out. So we’re not going to slow down on that front […] Now, as far as what we look at is going to be always trying to look at those things that feed all the way downstream. We always like to talk about how we go from wellhead to the water and we do it across all the commodities”

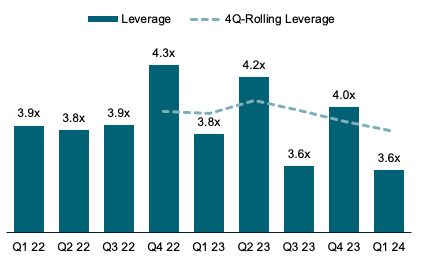

And while I do not want to dive into more detail here regarding possible acquisition targets, I believe ET’s balance sheet is well positioned for additional M&A, both paid for in cash or by stock. As of Q1 24, net leverage as measured by net debt over annualized EBITDA hit 3.6x, down significantly from the 4.0x in Q4 23 and among the lowest post-Covid. It also continues the broader trend which saw 4Q-rolling leverage fall from 4.0x as of YE22 to currently 3.8x, setting ET up well for inorganic expansion.

Company Filings

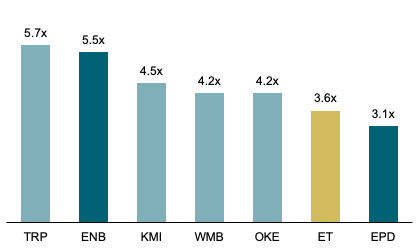

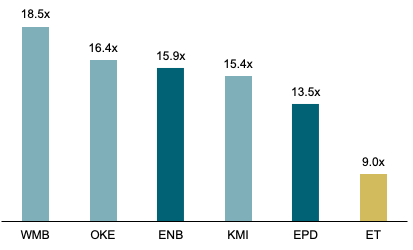

To further highlight the strength of ET’s balance sheet, I want to note that the company remains one of the lowest-levered companies among large-cap NA midstreams with peer average at 4.2x and MLP peer Enbridge at 5.5x.

Leverage vs Peers (Company Filing)

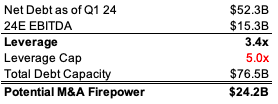

In estimating ET’s potential firepower for additional M&A, I assume an upper leverage bound of 5.0x, which, I believe, is appropriate given leverage levels at peers and the high predictability and stability of its business. At 5x 24E consensus EBITDA of ~$15.3B, I estimate ET could hold up to $77B in total net debt, implying a net firepower of $24B to be deployed towards potential M&A.

Company Filings, WSR Estimates

I also want to note that during Q1, ET’s senior unsecured debt was upgraded by Fitch to BBB with a stable outlook, highlighting the company’s strong debt profile and underscoring my assumption of a potential 5x leverage cap.

Valuation remains highly discounted vs. peers

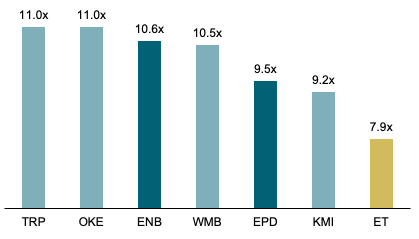

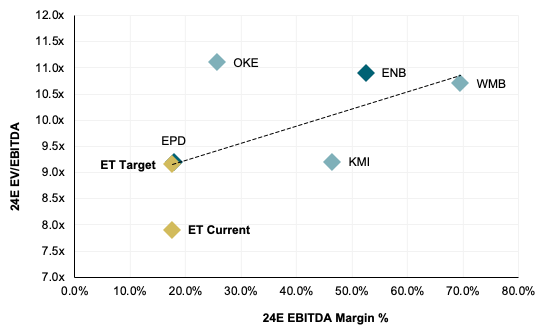

Despite the strong performance, I find ET continues to trade at a significant discount to both MPL and corp peers across metrics. Based on consensus 24E EBITDA of ~$15.3B, units are currently valued at only 7.9x EBITDA which is significantly below the broader sector average of 10.3x as well as its large-cap MLP peers ENB and EPD which trade at 10.6x and 9.5x respectively.

EV/EBITDA vs Peers (Bloomberg)

Considering 24E EBITDA margins, which in ET’s case are expected at ~18%, I find the valuation even more depressed and continue to assume that the company could trade at a “fair” 9.2x multiple based on a peer regression.

Company Filings, WSR Estimates

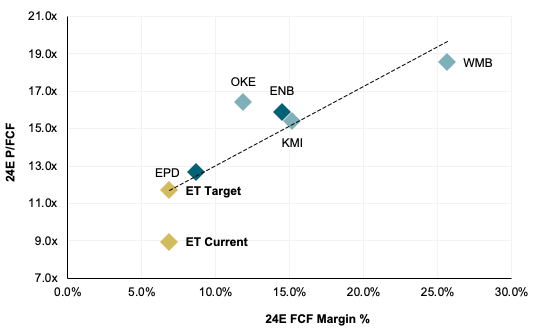

I see similar diversions between ET’s and peers’ valuations when considering the P/FCF (inverse FCF yield). At current estimates, ET units trade at ~9x 24E FCF/unit, again significantly below both the sector (15.9x) and its MLP peers ENB (15.9x) and EPD (13.5x).

P/FCF vs Peers (Bloomberg)

Assuming consensus FCF margin of ~7% for 24E, I estimate ET could trade at a “fair” 11.7x P/FCF multiple based on a peer regression.

Company Filings, WSR Estimates

Valuation Update

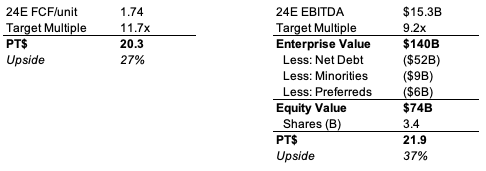

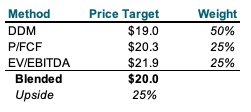

I continue to value ET via a blend of 3 methods: a fundamental DDM model, and regression-derived multiples on 24E EBITDA and FCF estimates.

Given the raised guidance and strong performance during Q1, I upgrade my EBITDA estimate to ~$15.3B (upper end of guidance) and my FCF/unit estimate to $1.74. Assuming multiples derived from above peer regressions, I apply an 11.7x P/FCF and a 9.2x EV/EBITDA multiple for respective unit price targets of $20.3 and $21.9.

Company Filings, WSR Estimates

Flowing through the raised distributions which now stand at $1.27/unit annualized and keeping my assumptions for discount rates and LT growth constant from my last analysis (see here), I also adjusted my DDM-based price target slightly upwards to $19/unit. Continuing to weigh DDM at 50% and EV/EBITDA and P/FCF at 25% each, I raise my blended price target by ~2% to $20/unit, implying 25% potential price upside.

Company Filings, WSR Estimates

Read the full article here