ePlus (PLUS) provides IT solutions to a number of industries. The company has had a good long-term history of organic growth and select acquisitions to enlarge ePlus’ footprint. The company has achieved clearly higher margins from FY2021 forward after almost a decade of very stable EBIT margins. The company seems reasonably priced at a forward P/E of 12.0. To get a further look into the valuation, I constructed a discounted cash flow model in this text, estimating a fair value quite near the stock’s price at the time of writing.

The Company & Stock

Founded in 1990, ePlus provides a large range of information technology solutions and services. The company’s offering ranges from cloud, data center, security, networking, collaboration, and artificial intelligence solutions to services ranging from advisory and consulting services to software license optimization:

ePlus’ Offering (ePlus September 2023 Investor Presentation)

The company’s offering helps customers create a good technological infrastructure. ePlus has a good amount of large customers that the company helps in achieving better operations – ePlus’ customers include names such as Adobe, Cisco, Disney, Columbia University, Bloomberg, Geico, EA, and Verizon. ePlus’ customers operate on a range of industries, including technology, government & education, entertainment & media, healthcare, and financial services among other industries.

As a part of ePlus’ strategy, the company focuses on doing select acquisitions. In total, ePlus’ cash acquisitions add up to an amount of $252 million from FY2014 to the current date as of Q1/FY2024. Compared to the company’s current market capitalization of $1.7 billion. The acquisitions improve ePlus’ nationwide footprint:

ePlus’ Acquisitions (ePlus September 2023 Investor Presentation)

ePlus’ strategy has proven quite successful. In the past ten years, ePlus has achieved a stock appreciation CAGR of 16.9% as a result of share buybacks, and growth through acquisitions and organic efforts:

Ten-Year Stock Chart (Seeking Alpha)

Financials

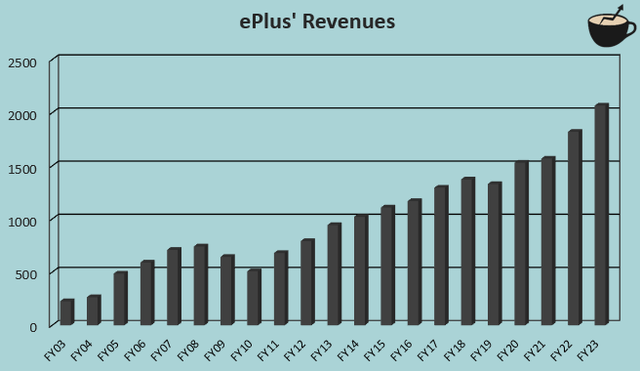

ePlus’ revenue history is excellent. The company has achieved a compounded annual growth rate of 11.7% from FY2003 to FY2023. For FY2024, ePlus is guiding for a growth of 8% to 13% – the growth seems to be continuing near the company’s long-term average rate despite economic turbulence.

Author’s Calculation Using TIKR Data

ePlus’ EBIT margin has been very stable from FY2012 to FY2020 with the margin staying very near six percent. On a more long-term basis, ePlus’ average EBIT margin from FY2003 to FY2023 has been 5.8%. In recent years, though, the company has been able to scale its margins quite significantly for shareholders – currently, the EBIT margin stands at a trailing level of 8.4%, significantly above the historical level of 5.8%:

Author’s Calculation Using TIKR Data

Valuation

Currently, ePlus trades at a forward P/E of 12.0, around 17% below the stock’s ten-year average of 14.4:

Historical Forward P/E (TIKR)

The P/E ratio alone seems quite low, as ePlus has been able to create shareholder value through organic growth and acquisitions. To further analyse the valuation and to estimate a rough fair value for the stock, I constructed a discounted cash flow model in my usual manner. The model only includes ePlus’ organic performance, as acquisitions are challenging to model in terms of cash flows as acquisition prices and timings largely vary.

In the model, I estimate ePlus’ revenues to grow by 11% in FY2024, representing a figure that’s slightly above the guidance of 8% to 13% growth. After FY2024, I estimate the revenue growth to come down slowly in steps throughout the years – for FY2025, I estimate a growth of 10%, only one percentage point below FY2024. The growth finally slows down into a perpetual growth rate of 3%. In complete, the revenue estimates represent a CAGR of 6.9% from FY2023 to FY2033.

I believe that the higher EBIT margin achieved from FY2021 forward is mostly sustainable. For FY2024, I estimate a slightly lower EBIT margin as I believe it is line with ePlus’ guidance for adjusted EBITDA. After the year, I estimate the margin to start scaling very slightly into a figure of 8.3%, achieved in FY2033 – ePlus’ amortizations should lower as time goes on, as my DCF model only estimates organic figures. Also, as the company scales, ePlus should achieve very slight operating leverage. ePlus’ cash flow conversion is decent, but the company does have a long track record of increasing net working capital due to the company’s growth.

The mentioned estimates along with a weighted average cost of capital of 11.91% craft the following DCF model with a fair value estimate of $68.33, around 9% above the price at the time of writing. The DCF model implies that ePlus is very slightly undervalued:

DCF Model (Author’s Calculation)

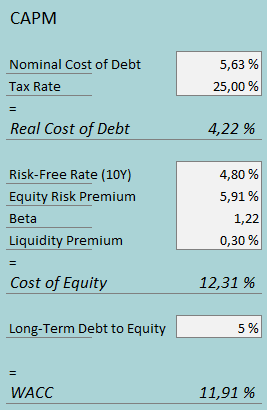

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In the past twelve months, ePlus has had $4.6 million in interest expenses. With the company’s current amount of interest-bearing debt, ePlus’ interest rate comes up to a figure of 5.64%. ePlus uses a very low amount of debt in the company’s financing with a current debt balance of around $81 million in long-term debt – I estimate ePlus’ long-term debt-to-equity ratio to stay low at an estimated 5%. I believe that the company could use further debt as a form of cheaper financing, but I don’t see it as likely that the company does so in the short- to medium term, or the long-term either.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.80% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates ePlus’ beta at a figure of 1.22. Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity of 12.31% and a WACC of 11.91%, used in the DCF model.

Takeaway

At the current price, ePlus seems to be priced for a performance that’s near the company’s long-term average in terms of revenue growth. In addition, the price mostly reflects the achieved higher EBIT margin to stay as a sustainable level. I see both of the mentioned assumptions as reasonable, as ePlus has continued to perform well in the current economy. Although the DCF model estimates ePlus to be slightly undervalued, I don’t see the undervaluation wide enough for a buy rating – for the time being, I have a hold rating for ePlus.

Read the full article here