The purpose of this article is to examine EQB (TSX:EQB:CA) (OTCPK:EQGPF) from the perspective of a long-term investor and try and project what they will be worth in 4-5 years. I believe EQB is a buy at its current valuation, as it is uniquely positioned to take advantage of demographic and economic trends in Canada that will enable them to continue growing at a fast rate. In this article, I will break down the mechanics of EQB’s loan portfolio, as well as the key trends currently happening in Canada that I believe uniquely play into EQB’s favor.

Thesis

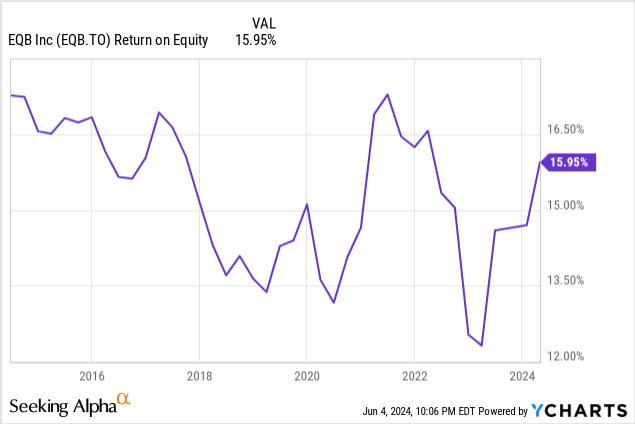

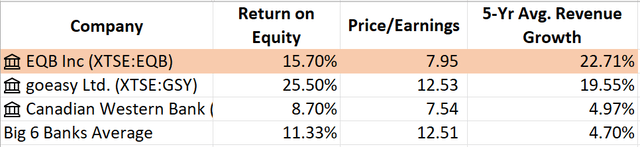

The thesis with EQB is quite simple. It is an extremely fast-growing bank with high return on equity that trades at a cheap valuation multiple. EQB has grown revenues over 20% annualized over the past 5 years and has consistently maintained ROE in the 14-16% range:

EQB Metric Comparison (Author, Company Financial Filings)

Despite this, EQB currently trades at a valuation that looks cheap, especially when compared to other Canadian bank stocks.

Personally, I believe that EQB’s P/E ratio is fair, and I am not banking on this P/E ratio expanding as part of my reason for investing in them. The reason EQB trades at a relative discount is because they are highly exposed to the Canadian real estate market, which many believe to be overvalued and due for a correction. Whether you think it is overvalued or not, the fact that EQB is hyper-exposed to one specific market in one specific country will naturally make it trade at a discount. Especially when you compare it to Canada’s big 6 banks which are significantly larger and more diversified in terms of their loan portfolios and also their businesses (many of the big 6 also have other business lines like wealth management, insurance, investment banking, etc.). Until EQB can diversify away from Canadian housing, they will always look “cheap”. Thus, I would expect the P/E to continue to hover in the 6-10x range for the foreseeable future.

What I am expecting to happen is EQB continues to grow their loan portfolio at a high rate and maintains return on equity in the same 14-16% range. These are the two most important things that need to happen for EQB.

Operating Efficiency and ROE

EQB is one of the most operationally efficient banks in North America. Their efficiency ratio (non-interest expenses/total revenue) has historically been in the mid-40s. The main reason they are able to achieve this is because they are an entirely digital bank that doesn’t have any physical branches. This ability to keep costs low will ensure their ROE remains in the 15-17% range for the foreseeable future.

Loan Portfolio

For any bank stock, expanding the loan portfolio with high-quality borrowers that meet the bank’s credit requirements (i.e., they don’t have to loosen credit standards to drum up new business with potential borrowers) is key to success. EQB has proven they can do this well, even during a time when interest rates were raised at the fastest rate in over 30 years.

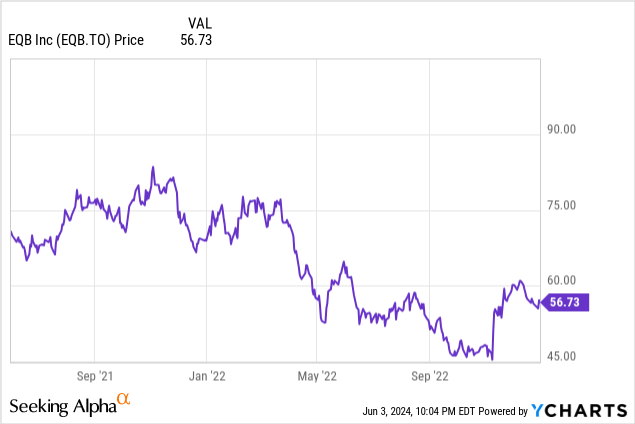

Whenever we enter a rising interest rate environment, it’s always a question of whether or not rising interest rates are good or bad for bank stocks. The answer, like most things, is that it depends. Rising interest rates hurt bank stocks because the demand for money slows down when interest rates are higher, and since banks have a natural run off in their loan portfolios where borrowers pay back loans, if they can’t renew those loans or originate new loans with new borrowers, their total loan portfolio will shrink and interest income will keep going down until they can originate new loans. Rising rates can also help bank stocks because interest income goes up. So when the Bank of Canada started to signal that they would be raising rates in early 2022, EQB stock dropped:

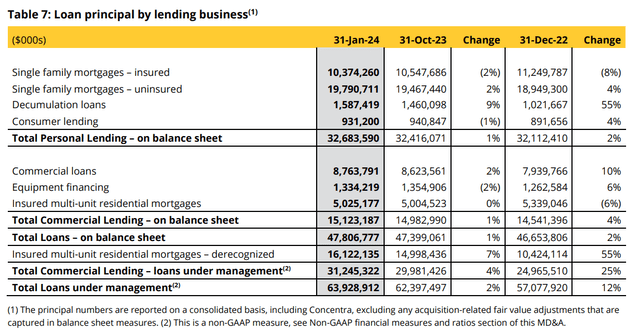

By the end of 2022, the BoC’s rate hikes were largely finished (4.25% at that time versus 5% currently). However, EQB was actually able to grow both of their personal and commercial portfolios from the end of 2022 to Q1’24 during that high interest rate environment:

EQB Loan Portfolio (Q1’24 MD&A Table 7)

This was a surprise for investors and led to EQB doing much better than expected to the point where they were the best performing bank stock in Canada during 2023. The reason EQB was able to do this was because their lending products are well positioned to take advantage of demographic trends occurring in Canada right now and in the coming years.

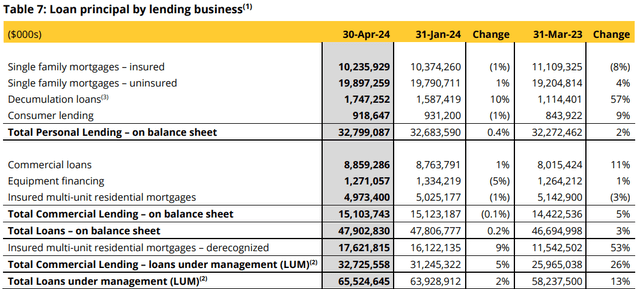

Additionally, EQB recently reported their Q2’24 results and showed a slight increase in on balance sheet loans, primarily driven by a 10% QoQ increase in decumulation loans, which is primarily due to reverse mortgages which I will discuss in more depth later.

EQB Table 7: Loan Portfolio Q2’24 (Q2’24 MD&A)

There was also a 9% increase in derecognized multi-unit insured residential mortgages. These are loans that EQB securitizes as part of the CMHC’s Canada Mortgage Bond program, where the CMHC guarantees these bonds, which in essence means that they are government-backed. These bonds are typically purchased by institutional investors like pension funds, insurance companies, banks, and even the Government of Canada has committed to purchasing $40B in 2024. Although it is good EQB is having success in this area and is able to diversify their revenue streams by increasing their non-interest revenue (non-interest revenue represented 16% of total Q2’24 revenue, up from 11% in Q1’23), ultimately the income they receive from this securitization activity is small.

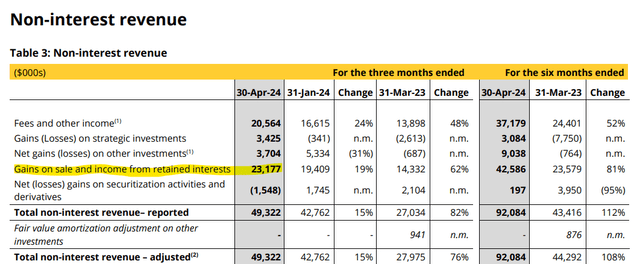

EQB Q2’24 Non Interest Revenue (Q2’24 MD&A)

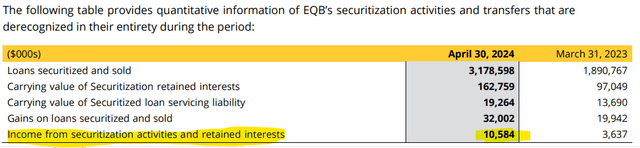

The non interest revenue line item “Gain on sale and income from retained interests” which was $23MM in Q2’24 is partially driven by “Income from securitization activities and retained interests”, which contributed ~$10.5M to the bottom line in Q2’24:

Q2’24 Note 9 (Q2’24 MD&A)

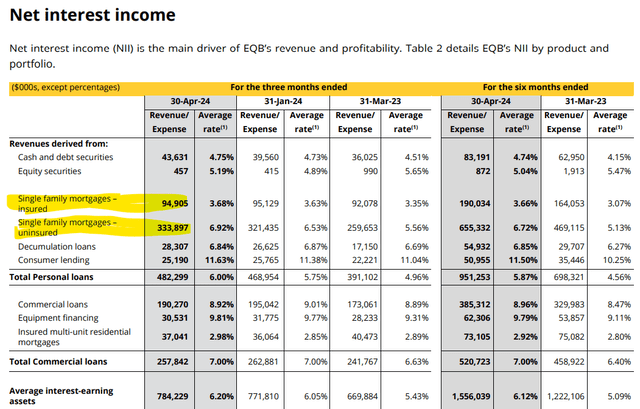

The reason I am pointing this out is to show that this revenue source is comparably much smaller versus the interest income they earn from single family residential mortgages, which was $429 million for the quarter:

EQB Q2’24 Net Interest Income (EQB Q2’24 MD&A)

So despite the high rate of growth in the multi-unit residential mortgages, the contribution to EQB’s bottom line is not significant. Overall, higher interest rates provided a boost to EQB because their interest income increased while they were able to slightly grow their loan book.

Key Trends

Let’s now dive into some demographic/macro trends happening in Canada which I believe favor EQB not just this year, or next quarter, but well into the long term.

Trend #1: Canada’s Limited Housing Supply

There is a great need for new housing units to be built in Canada right now, especially in major metropolitan areas like Toronto, the GTA (greater Toronto area), and Vancouver. Average rent for a 1 bedroom apartment in Toronto is currently $2,459/month and in Vancouver it is $2,646/month. To put this into perspective, someone earning a “decent” salary of $85,000/year in Toronto would have roughly 50% of their after-tax pay go towards rent. As such, new housing starts are needed in Canada, and these have actually increased in the period 2022-present (i.e., the higher interest rate environment) versus the pre-COVID era. Housing starts increasing is crucial to EQB’s success as this supplies them with a pipeline of potential future mortgages to originate from. This was a key focal point in the 2024 federal budget where the Government of Canada set the target of 3.87 million new homes by 2031. This is a lofty goal, and there are challenges that Canadian developers face in expanding Canada’s housing supply whether it’s restrictive zoning laws, obtaining permits to develop new units, or just the availability of labour to construct the housing. But the incentives exist for Canada and EQB is at the forefront of financing this as they offer both single family mortgages and multi-unit residential mortgages.

Trend #2: Canada’s Aging Population

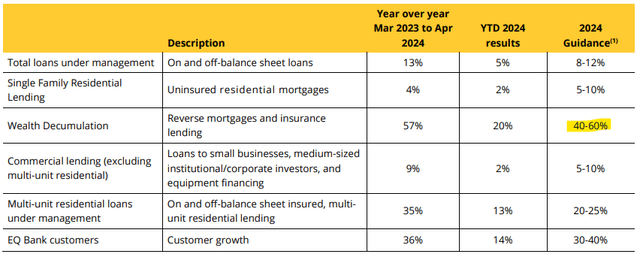

The late-baby boomer and early-Gen X cohorts in Canada are increasingly starting to reach retirement age, and many of these cohorts are homeowners with significant equity built up in their homes. As mentioned earlier, EQB offers reverse mortgages which allow homeowners to access this equity they’ve built up in their homes. Reverse mortgages are typically used by retirees that are house rich but cash poor and don’t wish to leave their home. It’s not a product for everyone, but there is a cohort of This product has been growing very fast for EQB and they guided for this business line to grow 40-60% YoY in F2024:

EQB Loan Portfolio Guidance (EQB Q2’24 MD&A)

Trend #3: Immigration

Regardless of what your stance is on immigration in Canada, it is something that has bipartisan support and will likely be high for the foreseeable future. Immigration in Canada has skyrocketed over the past ~18 months from an already elevated level that we saw pre-COVID. EQB’s biggest money maker is single family mortgages and majority of those are alternative mortgages. These are designed for borrowers who the bigger banks won’t lend to, such as self-employed workers, those who lack a long enough credit history, and recent immigrants.

Valuation & Price Prediction

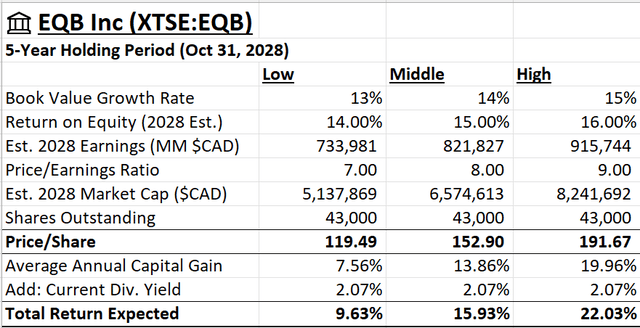

To determine if EQB represents good value to investors at its current stock price/valuation, I’ll use a bull, bear, and middle case and project what I think the stock will be worth 5 years out (i.e., by Year-End 2028) under different assumptions. The assumptions in each case are based on what management has guided for, what they have done historically, and what i think is reasonable for EQB going forward.

EQB is obviously a bank so we cannot use a DCF to value them. So I will project their book value growth rate out for the next 5 years, multiply book value by return on equity to calculate an earnings estimate for FYE2028, apply a P/E ratio to the earnings to calculate a market cap estimate, and then divide by shares outstanding to get an estimated price/share.

Here are the assumptions under each scenario:

Bull Case

- 15% annual book value growth each year for the next 5 years – book value grew at 17.3% CAGR F2018-F2023.

- 16% return on equity in F2028 – ROE has historically been in the 14-17% range

- 9.00x P/E ratio in 2028 – EQB’s P/E ratio has historically hovered in the 6.00 – 10.00 range.

- 43 million shares outstanding in 2028 – currently has 38.3 million shares outstanding, assumes ~2% annual dilution which is in line with historical rate of dilution

Middle Case

- 14% annual book value growth each year for the next 5 years

- 15% return on equity in F2028

- 8.00x P/E ratio in 2028

- 43 million shares outstanding in 2028

Bear Case

- 13% annual book value growth each year for the next 5 years

- 14% return on equity in F2028

- 7.00x P/E ratio in 2028

- 43 million shares outstanding in 2028

EQB Stock Price Projection (Author, EQB Quarterly Reports)

It’s also important to note that since I used 2023 Year-End book value as the base for my projections, and dividends paid to shareholders reduce the book value, I have added the current dividend yield of 2.07% to the return projections (i.e., this model assumes you bought the stock now and held for 5 years).

As we can see, even in the more conservative case we are still projecting ~10% annual returns, and in the bull case (which I think is more likely) annual returns are projected at over 20%. This does assume some multiple expansion from EQB’s current PE of ~7.50x to 9.00x, but it’s not uncommon for their PE ratio to exceed that level from time to time. I would remain a buyer of EQB at any price point below $90 CAD/share.

Key Risks

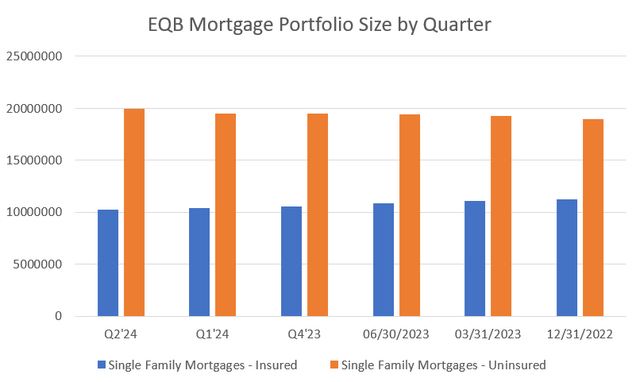

The biggest risk facing EQB is their exposure to Canada’s housing market, as discussed earlier. I believe this risk is partially reflected in EQB’s valuation, given its discount to other Canadian banks despite having higher historical growth and ROE. But overall, this is a risk that investors in EQB will have to accept. Another key risk is if the Bank of Canada keeps interest higher for longer than expected. This still remains a question, but the BoC just cut rates by 0.25bps in June, and some economists in Canada expecting more rate cuts in the second half of the year. Due to Canada’s high household debt level, the BoC may look to cut rates faster than the Federal Reserve. A rate cut will likely cause an increase in mortgage origination activity for EQB, which has essentially been flat for the past ~18 months:

EQB Mortgage Portfolio Size (Author, EQB Historical MD&A)

Conclusion

EQB is currently valued at a discount relative to Canadian banking peers due to the perceived risk it has by being highly exposed to Canadian real estate. I believe there are several demographic trends as discussed above that play into EQB’s favor and will help ensure they can maintain a high ROE and book value growth rate in the coming years, and they represent solid value to investors at their current valuation of CAD 87/share.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here