By Melda Mergen, CFA, CAIA

We sat down with Melda Mergen, Global Head of Equities, to talk about timely trends and opportunities equity investors should be paying attention to.

One market trend we’ve observed is that a lot of performance has been concentrated in just a few stocks – the so-called “Magnificent 7.” Do you think this will continue?

When we see that kind of concentration of performance (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla), we don’t believe it’s likely to be sustainable. But that doesn’t mean we’re not going to take advantage of it. Those companies continue to have great free cash flow and what we see as strong, long-term growth potential. But, as expected, that outsized performance decelerated year-to-date in 2024. At the same time, we’re seeing performance expand into other areas of the market, which we view as much better longer term – a healthier breadth in the marketplace and more participation in outperformance from different sectors.

We’ve also observed that recent strong performance has boosted valuations. Do you think equities are too expensive now relative to their growth potential?

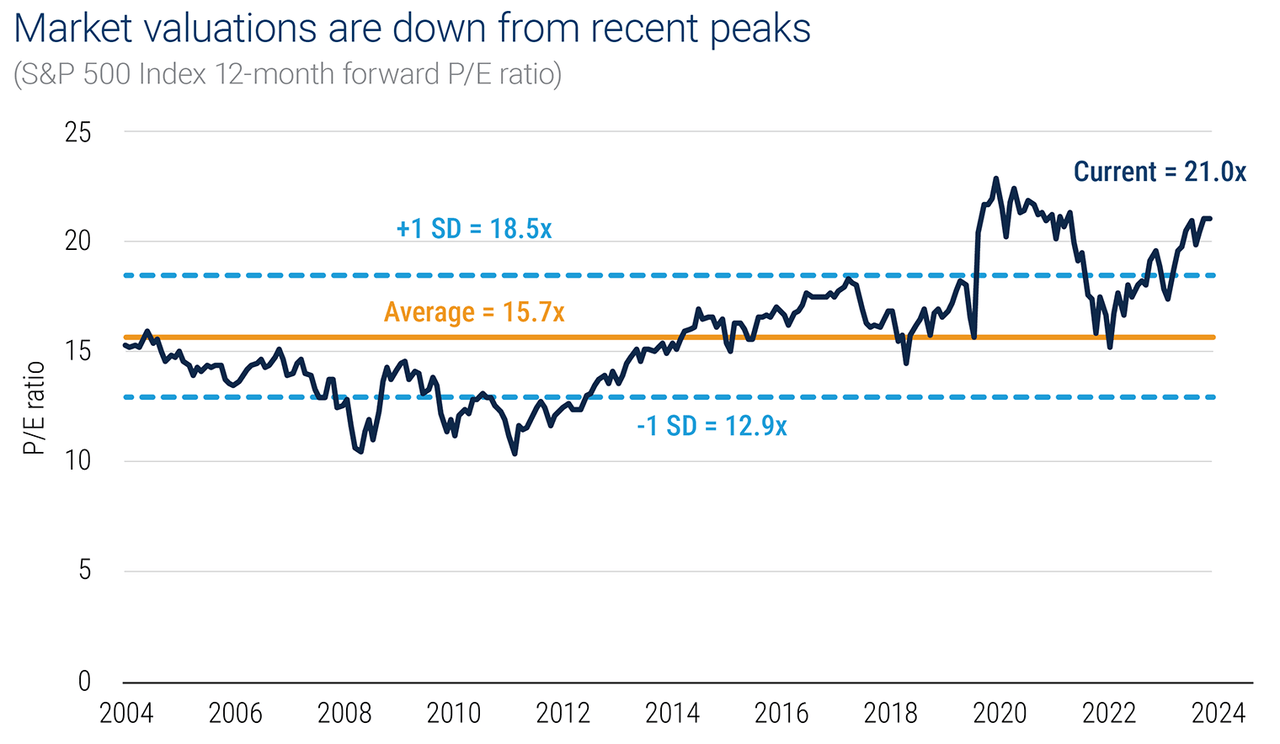

If you look at the S&P 500, there’s no question that large-cap equities look expensive right now. But when we look at valuations from the previous peak, which was at the end of 2021, we see that valuations have actually come down. Also, the strong performance that got us to these valuations was supported primarily by the earnings growth, which is a healthy outcome.

Source: FactSet as of July 31, 2024. Stocks are represented by the S&P 500 Index. It is not possible to invest directly in an index. Past performance does not guarantee future results.

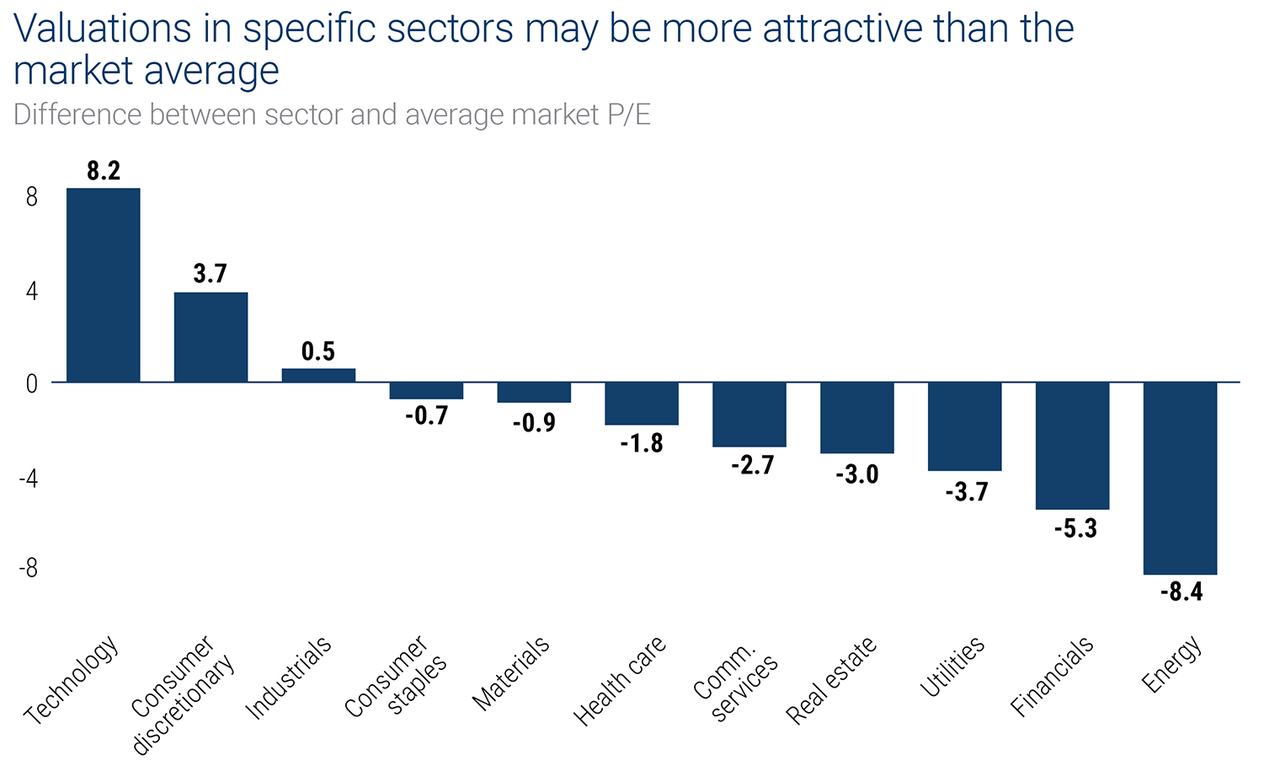

You also can’t paint the whole market with the same brush. When you dig down to the sector level, there are different opportunities at different levels of valuation. We see many opportunities where valuations are supported by strong fundamentals, and therefore make good investments.

Source: FactSet as of July 31, 2024. Stocks are represented by the S&P 500 Index. It is not possible to invest directly in an index. Past performance does not guarantee future results.

The question is whether that strong earnings growth will continue, and the answer to that is company-specific. In the previous 10 to 15 years, it was much easier for companies to allocate capital. Interest rates were very low, so they were able to borrow cheaply to fund future growth. That environment has changed dramatically. The most important thing investors want to know now is what companies are investing in and why, and, more importantly, where the revenue will come from. For their part, companies have reacted by becoming much more transparent about their capital spending, which is going to be very important for investor conviction and confidence.

AI continues to drive the market and intrigue equity investors. What is your approach to investing in AI?

We are always looking to invest in longer-term opportunities, and AI is one of them. We started investing in AI seven or eight years ago, so we have benefited from the increased interest and hype. Rather than direct uses of AI, we focus more on innovation through AI. We’re watching it happen in health care, medical equipment, pharmaceuticals – even industrials. AI is even affecting another theme we’re invested in: energy transition. It’s changing the way we think about using energy and what we use it for. For example, powering a training model for AI is a different use of energy than pushing it to users through the grid. There are going to be major adjustments and realignments in that regard, and we plan to invest in those opportunities as they evolve. As this continues, we expect that companies across a wide range of sectors will be creating new services and goods we can invest in.

Are there any risks that you’re worried about?

For many companies, geopolitical risk is going to be part of the reality of doing business over the next three to five years. It’s not necessarily going to impact fundamentals, but rather the way companies think about their short- and medium-term operating environments. The impacts could be significant, and it’s something we’re always paying very close attention to in our portfolio.

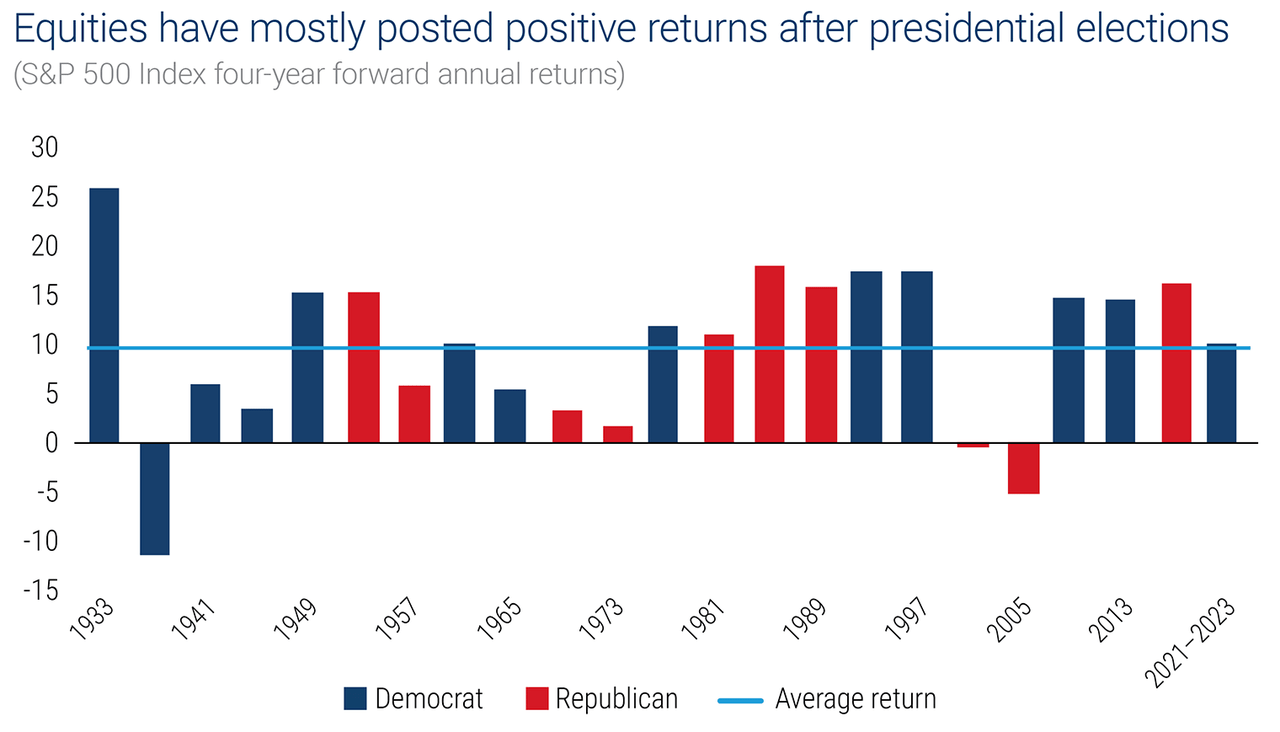

Shorter term, in the U.S., we have the potential for volatility around the election. Historically, volatility increases heading into big national elections because there’s more headline risk and more uncertainty – and so we are expecting market volatility to increase as we get closer to November. But investors tend to benefit when they take a long-term view: Since 1932, the average four-year forward annualized return of the S&P 500 after an election has been 9.5%, and only three presidential elections out of 22 resulted in a negative forward result. That’s why it’s important for investors to stay focused on their goals and look past short-term election-year volatility.

Source: Columbia Threadneedle Investments. Stocks are represented by the S&P 500 Index. It is not possible to invest directly in an index. Past performance does not guarantee future results.

Disclosures

Investing involves risk, including the risk of loss of principal. In general, equity securities tend to have greater price volatility than fixed-income securities. The market value of securities may fall, fail to rise or fluctuate, sometimes rapidly and unpredictably.

The products of technology companies may be subject to severe competition and rapid obsolescence, and their stocks may be subject to greater price fluctuations.

Additional Disclosures

© 2016-2024 Columbia Management Investment Advisers, LLC. All rights reserved.

Use of products, materials and services available through Columbia Threadneedle Investments may be subject to approval by your home office.

With respect to mutual funds, ETFs and Tri-Continental Corporation, investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. To learn more about this and other important information about each fund, download a free prospectus. The prospectus should be read carefully before investing. Investors should consider the investment objectives, risks, charges, and expenses of Columbia Seligman Premium Technology Growth Fund carefully before investing. To obtain the Fund’s most recent periodic reports and other regulatory filings, contact your financial advisor or download reports here. These reports and other filings can also be found on the Securities and Exchange Commission’s EDGAR Database. You should read these reports and other filings carefully before investing.

The views expressed are as of the date given, may change as market or other conditions change and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, may not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not take into consideration individual investor circumstances. Investment decisions should always be made based on an investor’s specific financial needs, objectives, goals, time horizon and risk tolerance. Asset classes described may not be appropriate for all investors. Past performance does not guarantee future results, and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that any forecasts are accurate.

Columbia Funds and Columbia Acorn Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA. Columbia Funds are managed by Columbia Management Investment Advisers, LLC and Columbia Acorn Funds are managed by Columbia Wanger Asset Management, LLC, a subsidiary of Columbia Management Investment Advisers, LLC. ETFs are distributed by ALPS Distributors, Inc., member FINRA, an unaffiliated entity.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here