Introduction

Escalade (NASDAQ:ESCA) has seen massive gains and subsequent losses in its share value since the first time I covered it back in May of ’23 when I argued that the company has a catalyst in Pickleball, which grew at an unexpected pace. I wanted to revisit the company to see how it did over the last year and whether the declines were justified. With the decline in revenues, which led to decreases in margins, the company has seen somewhat of a bottom in the latest quarter and a decent improvement in efficiency, giving me hope that the worst for the company has passed, and the outlook is going to improve. A buy rating was retained, and a small position was initiated.

Briefly on Financials

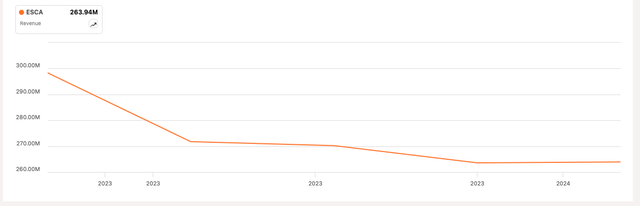

For the revenues, we can see the company saw a bit of a struggle throughout ’23. The elevated interest rates and softening demand for outdoor sports, which came in below COVID levels pent-up demand, but over time it still was higher than pre-COVID levels. We can also see that in the latest quarter, the demand seemed to have somewhat returned, and we can see a bottom setting in. However, I would need to see another couple of quarters before coming to this conclusion.

Seeking Alpha

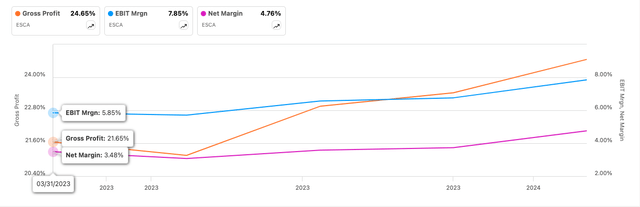

The metrics I am very happy with are its margins. These have seen a steady improvement throughout the year and in the latest quarter, the company saw an increase of 560bps in gross margins, which is a fantastic result of the company’s cost-cutting efforts, like normalization of inventory costs, shutdown costs of its Rosarito facilities in Mexico, and a slowed production to reduce inventory to match the softness in demand throughout ’23.

Seeking Alpha

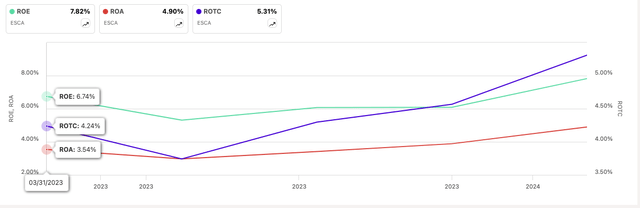

Continuing with efficiency and profitability, the company’s ROA and ROE have seen a similar uptrend as the margins above, which indicates that the management is doing a much better job at utilizing the company’s assets and shareholder capital, evident in vast improvements across margins. Furthermore, the company’s ROTC, which measures how efficient the management is at allocating capital to profitable projects has also seen a decent increase from the bottom about a year ago, which means the company is reclaiming its competitive edge as demand picks up and costs continue to decline.

Seeking Alpha

Overall, the company has been improving since most of the metrics bottomed out in the second half of ’23. As freight costs began to ease, interest rates and inventory levels stabilized, the company’s profitability and efficiency improved. Over the last few quarters, the company’s efficiency and profitability took a big hit, and so did its share price, which was expected. However, since the company is a small cap, a couple of misses on earnings means high volatility and exaggerated price movements.

Comments on the Outlook

It looks like it all depends now on the company’s ability to return to top-line growth. The year-over-year increase of less than 1% in sales is a good start, however, it doesn’t seem to help the company’s growth narrative since it is minuscule, but it may indicate a bottom has set. However, more quarters are needed to decide if that is the case.

The company’s clients have worked through the main issue of having too much inventory, which should help ESCA regain growth on the top line in the future as inventory levels continue to normalize. A lot of the issues over the last couple of quarters were due to an oversupply of inventory, which led to much softer demand, which led to a massive decrease in the company’s gross margins. Higher freight costs and fixed costs of facilities, especially in the facilities in Mexico, didn’t help the company’s efficiency and profitability at all, which also added to the gross margin pressures. Now, with the latest quarter showing a massive improvement in gross margins, the only problem I am seeing right now that may hinder the company’s return to overall growth in the top line and subsequent reversal of the direction of the share price is the return of the demand. As I mentioned before, clients have worked on their inventory levels over the last half a year, which means I expect to see some sort of growth returning. What is also a positive for the company is we are entering a time of increased spend on outdoor sports products because the summer is here. The pent-up demand post-covid drove up inventory levels, so now that everything has finally normalized, I am expecting a return to growth going forward. According to this post, sports products will see an 8.6% CAGR over the next 8 years, which means ESCA should benefit from this in one way or another. Furthermore, the company’s target demographic is of higher income, which means the demand should be much more resilient to economic downturns.

I am also seeing some more improvements in margins going forward as the company ramps up production to match the increase in demand, as economies of scale kick in. It is hard to tell how much that would help, but it will be a positive. Additionally, as the company divests its facilities in Mexico, I am also expecting to see improvements in the company’s EBITDA figures overall.

Valuation

It’s been a year since I did a DCF analysis of the company, and now the company’s share price is basically back where it was a year ago, so no better time than the present to see what the numbers will tell us.

For revenue growth, I am going to be on the conservative end and model 0% growth for FY24. We already saw some growth returning, but to be safe, I will model no growth, which will act as a margin of safety. After FY24, I am going to grow the company’s top line at around 4% CAGR, which is about half what the research above suggests, which was 8.8%. The reason I feel confident that the company will see some sort of growth over the coming years is that inventory normalization, as I mentioned above, should bring back demand for the products. Also, by growing at around 4% a year and not by 8.8%, I am getting even more downside protection, and it is always better to be safe than sorry when it comes to the company’s potential. Since the company is not heavily covered, I believe these growth rates are a good estimation. Furthermore, I am also going to model a more conservative case and a more optimistic case, to give myself a range of possible outcomes. Below are those estimates.

Author

For the margins, I am modeling slightly lower margin improvements than what the company saw in Q1 due to uncertainty that the company will manage to sustain it. I went with around 24.5% on gross margins instead of 25%. I will be updating these numbers later on when we have a couple of more quarters released to make sure that the company is going to be able to sustain these increases. Over time, as the demand returns, the company’s operations should improve; therefore, I’m modeling a modest increase of 100bps over the next decade.

Author

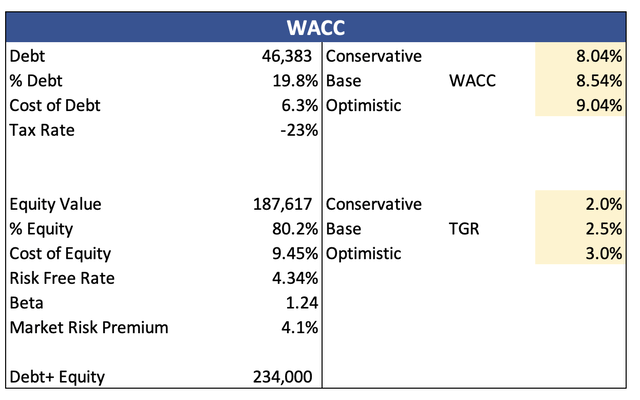

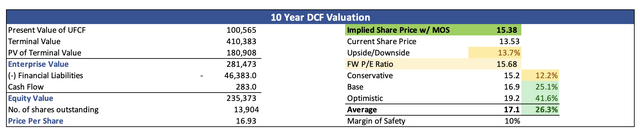

For the DCF analysis, I am using the company’s WACC of around 8.5% as my discount rate and a 2.5% terminal growth rate because I would like the company to at least grow at the long-term US inflation goal.

Author

Furthermore, to give myself even more room for error in these estimates, I am going to add another 10% discount to the final intrinsic value. With that said, the company’s intrinsic value is around $15.38 a share, meaning the company is trading at a decent discount to its fair value.

Author

Risks

The demand continues to be subdued, which will lead to the company’s deterioration of its margins once again. The Q1 massive improvements would end up being unsustainable and be seen as a fluke.

The company hasn’t completely divested its facilities in Mexico and may incur further costs associated with the disposal, which will affect the company’s profitability in the short run.

The company needs to continue to work on paying off its variable interest-denominated debt. The company’s average interest rate on debt was over 6%, so if there are more interest rate uncertainties in the long run, for instance, an interest rate hike, this will affect the company’s cash flow materially.

The company is a small cap, so expect massive fluctuations in prices even on days where there is no news apparent, just because of the nature of such companies that are thinly traded.

Closing Comments

I believe the worst has passed, and the above risks are not as prevalent as they may have been before, when the company saw a 25%+ decrease in sales, and when the FED was still considering interest rate hikes, but seems a lot more dovish these days, however, higher for longer is the theme on the markets.

I would like to see the company continue to pay down that rather high debt pile, and I am glad that they have been addressing it in the last couple of earnings calls, especially the high variable interest debt.

The summer is here so I expect some boost to the company’s top-line growth and since inventory levels have normalized, I expect this growth to remain going forward. Therefore, I am bullish on the company’s prospects going forward and maintaining a buy rating, as I open a small position and will wait until the next earnings to decide whether I am going to increase my holdings or not.

Read the full article here