My original thesis on buying The Estée Lauder Companies (NYSE:EL) was a variant of the dogs of the Dow theory, though they are not one of the 30 stocks in the Dow Jones index. In 2023, Estée Lauder lost 40% of its market value, coming off a poor 2022. That price movement alone is obviously not a reason to buy or sell a company, but it was a filter to assess whether a company’s stock might be selling at a discount.

I like buying companies that have durable competitive advantages that are discounted. It’s great when the reason that a company is discounted is market-specific and there’s no turmoil within the company, but that doesn’t happen every day. I would love to have that type of patience, but I’m not a market timer, and waiting for the perfect market opportunity could leave me on the sidelines for many bull runs. I believe it is better to be fully invested than try to time it perfectly. As a result, many of the companies I buy have some issues that I deem as temporary in nature.

For Estée Lauder, I happened to be reviewing a list of the worst returns in the S&P 500 for the past two years and was surprised to see a company that I had always thought of as a blue-chip quality company on this list. Here’s the 5-year chart, which shows the performance since the end of 2022:

EL 5 Year Chart (Seeking Alpha)

As a result, I decided to look further into Estée Lauder and see if this was a stock worth buying.

Estée Lauder is a diversified beauty products company, which sells makeup, perfumes, skincare and hair care products. It is the second-largest beauty company in the world, behind L’Oréal. (OTCPK:LRLCF). The beauty industry is heavily focused on branding, and Estée Lauder’s brands are one of its competitive advantages. I can go to any retailer and buy moisturizer for my face for under $10. Some of these products are even from brands under the Estée Lauder umbrella, such as the Ordinary. I can also spend over $200 for a more complex product that is also owned by Estée Lauder brands such as La Mer or Clinique. These diverse price points are true for its other beauty lines as well, which typically allow companies in this industry to flourish, no matter what economic environment we’re in. Below is an illustration of Estée Lauder’s brands:

Estée Lauder Brands (Estée Lauder’s Annual Report)

Beauty is an inexpensive luxury, relatively speaking, and has historically been a pretty good industry to be in as it tends to be more resilient.

How Did Estée Lauder Get Here?

Estée Lauder’s troubles really seem to have been mostly self-inflicted, though partially driven by the dynamics of the post-COVID supply chain environment. Back in 2021, it seemed that the company could do no wrong. The long periods of time people spent in the home by themselves in Spring 2020 and then again in Winter 2021 led to a surge in the purchase of beauty products once people began to gather together again. This was aided by a massive amount of government stimulus that helped disposable income of the average consumer in the U.S.

This surge of business drove very strong financial results, but also an extrapolation of those results and expectation that this would continue indefinitely by the market. It’s actually pretty amazing going through their last few years, including many of the Seeking Alpha articles at the time. Back when they were trading in the higher 200s to 300s, investors could not get enough of this company. The vast majority of the articles were glowing, buy rated articles. The company was backing it up with its results, too. I’m not sure anyone could have predicted that the company that earned $7.79 per share in fiscal 2021 would have earned only $2.79 two years later.

Cracks began to show in 2022 as Estée Lauder’s stock price began to drop with COVID related issues in China, but the company still had relatively strong results throughout much of fiscal 2022. That changed sharply in the fall of 2022 with Q1 2023 (quarter ended 9/30/2022) results and forecast. Despite headwinds, they continued to project confidence for the second half of fiscal 2023, which never came to fruition. The stock continued to decline.

Estée Lauder faced a significant issue. The post-COVID supply chain environment and China shutdown was outside of their control and caused shifts in demand for their products. However, the much larger issue for the company was their inability to forecast and react accordingly.

Barclays analysts had this to say of Estée Lauder’s predicament:

If we had to summarize how Estée Lauder ended up in the situation it is in, we believe the two biggest issues are poor demand forecasting and a lengthy legacy supply chain. The way we see it, these are specifically operational challenges to work through and not related to EL’s brand equities, which we believe remain strong.”

Another Barclays analyst, Lauren Lieberman, said Estée Lauder’s revised 2023 forecast was the “last thing” expected by Wall Street and questioned whether management has any “control or visibility” of sales through its China travel retail channel.

That’s not exactly something you’d expect from a company with $16 billion of annual revenues. The poor forecasting resulted in manufacturing far too much inventory that was shipped to their channel partners, resulting in a glut of inventory that took several quarters to work off. While the supply chain environment contributed to the issues, this seems to be mostly a self-inflicted problem.

The Case to Buy Now:

So, now that we know what happened in the past, the question remains whether this is fixable? I think the answer is yes.

The issues that Estée Lauder has faced are unfortunate, but certainly not fatal. The brands still have shown to hold value, and it has not been impaired because the company hasn’t done a great job forecasting or the economy in China has changed. While their current earnings have been impacted, the long-term earnings prospects of this company remain unchanged and the current issues are a good opportunity to buy as long as they don’t continue to persist. Certainly, the market’s view of the company has changed and now is the time to be contrarian.

Management has been very clear that the second half of fiscal 2024 is an inflection point for the company – so clear that they mentioned the inflection point five times on their Q3 2024 earnings call. Given that Q3 ended on March 31, we are at the time of year that Estée Lauder should be turning the corner and returning to the growth and profitability we had come to expect. The channel inventory issues have been cleared as of the end of Q3, according to the company’s latest earnings call.

Additionally, the profit recovery program, which focuses on reconstructing their gross margins, expects to add $1.1 to $1.4 billion of incremental profit in the 2025 to 2026 timeframe, which is consistent with their previous statements. They expect to have more granular detail on this in August after they release their Q4 earnings, but these savings should come from the better control on inventory they now have, which will reduce discounts and write-downs. But more importantly, they are working with their supply chain to gain greater savings through leveraging their expense base.

Risks

The most significant risk I see to my thesis is that somehow Estée Lauder’s durable competitive advantage in its brands has been eroded. In today’s social media influencer world, brands are established and driven in many different ways than the makeup counters at Macy’s or Bloomingdales in the mall. My concern is whether those brands are likely to become stagnant over time while the next generation buys products that are marketed on TikTok by some influencer that I’ve never heard of but somehow has 15 million followers. While I do think that can allow for the explosion of previously unknown brands, I don’t think it actually hurts a company like Estée Lauder. They employ the same techniques using Instagram and TikTok, but also have the marketing budgets to compete with any startup.

My other big question is whether management has oversold this turnaround to Wall Street and that they can actually deliver on the Profit Recovery program. This is less concerning to me because it would only be a delay in the recovery. In addition, their Q3 call referred to the rollout of their new “integrated business planning process” which sounds a lot like a basic forecasting/FP&A function that you would expect a company valued at $45 billion to have. They also mentioned that they complemented their advanced planning technologies using AI to improve accuracy, which is an immediate red flag for me, as it seems to me that management is trying to inject AI into the discussion where it isn’t necessary. With that said, the management may be viewed as a question mark to some, and I can understand if that causes any investor to immediately walk away.

Valuation – yet another risk

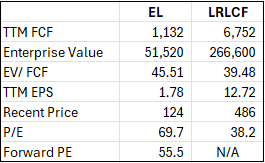

Even with the stock at these levels, the valuation is not compelling. For someone who fancies themselves a value investor, Estée Lauder, along with many of my other holdings, is not exactly a picture of value. Right now, P/Es are in the stratosphere, with even forward P/Es very elevated at 55x. EV / FCF is at an elevated 43x, which makes no sense for a company that has had such struggles. Obviously, this is not the expectation going forward, especially given the restructuring and profit recovery program. Can the Company return to earning approximately $2-3 billion per year in FY25 or FY26, as it did in the 2021-2022? Right now, analysts are understandably skeptical, and currently no analyst has them reaching these levels by the end of next fiscal year – they will have to prove it with their results.

But to be clear, this is a company that is making money, and has positive free cash flows, it is not in danger of going out of business. It also pays a nice dividend of over 2% that is more than covered by its annual free cash flow, so you’ll be paid modestly to wait for the recovery.

For comparison purposes, I considered two other beauty companies that sell similar items to Estée Lauder. However, the only competitor that is directly comparable is L’Oréal, even though it remains three times the revenue of EL. These are both large cap, mature beauty companies that have storied histories and very similar characteristics. The other company considered, e.l.f. Beauty (ELF) has been a great story, but it has only $1 billion in revenue and was founded relatively recently in the world of beauty / fashion. It really is not a comparable company.

Valuation Comparison of Estee Lauder vs. L’Oreal (Author Calculations Using Financial Data from Seeking Alpha)

As you can see, Estée Lauder’s valuation is elevated compared to L’Oréal, given its recent execution struggles. L’Oréal doesn’t really offer a compelling value either compared to other market opportunities, but that seems to be due to its strong stock performance rather than lower earnings in recent years.

Conclusion

Investing in what essentially amounts to a turnaround situation is never easy. I feel like I’ve made more points above that would lead you to be cautious rather than bullish on Estée Lauder. All you have to do is read the latest analyses of the company to see the pessimism in the market, which seems to be absolutely deserved. However, the time to get bullish on a company is not once the turnaround has already happened; you’ll miss the largest gains. Sometimes you have to take a chance that the inflection point that management has emphasized is real.

The sentiment around the company is very negative right now. That is one reason that I feel my downside is limited. If they are able to execute on their profit recovery plan, I believe I have a much larger upside potential than downside if they don’t. I would be a buyer of this stock at these levels and continue to have interest in the $130-$135 range.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here