The Eaton Vance Risk-Managed Diversified Equity Income Fund (NYSE:ETJ) is a closed-end fund that income-minded investors can purchase to obtain a very high level of current income without sacrificing their equity exposure. I have explained in a few recent articles that it is important for income-focused investors to maintain a healthy allocation to equity securities in a portfolio as a hedge against inflation. For example, in this report, I showed that the true rate of inflation might be higher than the official numbers state and fixed-income securities might still have yields that are too low to offset the loss of purchasing power. We saw further evidence that inflation might be higher than the official numbers suggest in an article published to Zero Hedge this morning. This article starts off with the following observation:

The most startling moment in the CNN debate last week between President Joe Biden and former President Donald Trump was not from the candidates. It was from moderator Jake Tapper, who said with a straight face as if it were just the science that grocery prices were up by 20 percent since President Biden was elected.

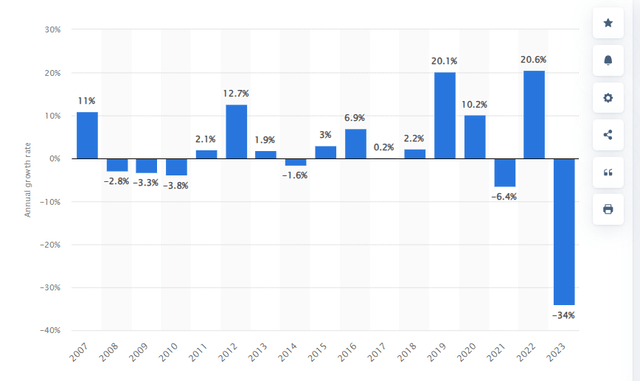

I do not think that anyone in this country believes that food prices have only risen by 20% since the start of 2021. Personally, my recent grocery bills are at least double or triple what I was paying in 2021, but there have been no real changes to my shopping habits. Restaurant prices have more than doubled since 2021, but that could be driven by other factors. The consumer price index also says that healthcare dropped 6.4% in 2021 and 34% in 2023:

Annual Rate of Change For Health Insurance Prices in CPI (Statista)

I certainly do not remember health insurance premiums dropping since 2021, as these numbers would require. Thus, we can logically conclude that inflation is higher than the official numbers suggest. Thus, the 4.491% yield on ten-year U.S. Treasury securities could easily be lower than the real level of inflation, particularly when we consider that investors need to pay income taxes on the payments that they receive from those securities. Equities usually deliver much stronger total returns, and the fact that they deliver much of their returns in the form of capital gains reduces the drag from income taxes. In fact, equities should at least keep up with inflation over the long term because inflation causes corporate profits to rise. For this reason, every investor should keep at least some of their portfolio invested in equities as protection against inflation. The Eaton Vance Risk-Managed Diversified Equity Income Fund is one way to maintain that exposure to equities while still earning a yield that most income investors will be satisfied with.

As of the time of writing, the Eaton Vance Risk-Managed Diversified Equity Income Fund boasts an 8.90% distribution yield. This is not as high as the best fixed-income funds deliver, but it is in line with its peers:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

Eaton Vance Risk-Managed Diversified Equity Income Fund |

Equity-Covered-Call Funds |

8.90% |

|

BlackRock Enhanced Capital and Income Fund (CII) |

Equity-Covered-Call Funds |

5.97% |

|

First Trust Enhanced Equity Income Fund (FFA) |

Equity-Covered-Call Funds |

7.03% |

|

Madison Covered Call & Equity Strategy Fund (MCN) |

Equity-Covered-Call Funds |

9.47% |

|

Voya Global Advantage and Premium Opportunity Fund (IGA) |

Equity-Covered-Call Funds |

11.53% |

|

Columbia Seligman Premium Technology Growth Fund (STK) |

Equity-Covered Call Funds |

5.56% |

As we can see, the current yield of the Eaton Vance Risk-Managed Diversified Equity Income Fund compares pretty well to the other funds in this category. The fund’s yield does not appear to be excessively high, so we probably do not need to worry about a distribution cut in the near future. However, it is not so low as to be unattractive to an income-seeking investor.

As regular readers might remember, we previously discussed the Eaton Vance Risk-Managed Diversified Equity Income Fund in late February 2024. The domestic equity market in general has been fairly strong since that time, but most of Eaton Vance’s option-income funds tend to lag the major indices during strong markets. This is quite understandable given the strategy that these funds use. As such, we might expect that this fund has delivered a reasonable but not awe-inspiring performance since the previous article was published. This is indeed the case, as shares of this fund have appreciated by 5.66% since that article was published:

Seeking Alpha

We can immediately see that this performance was worse than the 7.71% gain that the S&P 500 Index (SP500) delivered over the period. As just mentioned, this was expected to occur. The performance of this fund was therefore pretty much what we would have thought. The fact that it underperformed the index might cause some investors to look down on it, though, but many investors who have income as their primary goal are willing to accept a certain amount of underperformance in exchange for a higher yield. This fund certainly beats the 1.33% yield of the S&P 500 Index, so it does seem like it could be satisfactory.

However, as I stated in the previous article:

The Eaton Vance Risk-Managed Diversified Equity Income Fund is a closed-end fund, and as such, it delivers the majority of its total investment return in the form of direct payments to its shareholders. Thus, it is necessary to consider the distributions that investors received in any analysis of the fund’s performance because they will always result in the fund’s shareholders doing a lot better than the share price alone would indicate.

When we include all of the distributions that this fund has paid out since the previous publication date, we get this alternative chart:

Seeking Alpha

This chart seems almost certain to appeal to any investors, regardless of their overall goal. The fund’s distributions over the period were sufficient to allow it to beat the S&P 500 Index by 116 basis points since the end of February. There appears to be very little to complain about with respect to the fund’s recent performance.

As roughly three months have passed since we last discussed this fund, there have been quite a few changes. This article will focus specifically on these changes and attempt to determine if we need to update our thesis surrounding it.

About The Fund

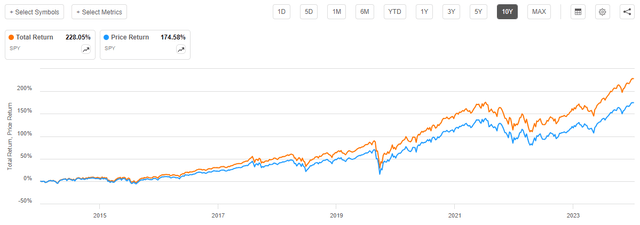

According to the fund’s website, the primary objective of the Eaton Vance Risk-Managed Diversified Equity Income Fund is to provide its investors with current income and current gains. This is an uncommon objective for an equity fund because of the fact that equities deliver almost all of their investment return in the form of capital gains. For example, take a look at the price return versus the total return of the SPDR S&P 500 ETF Trust (SPY) over the past ten years:

Seeking Alpha

The index fund, which ostensibly tracks the U.S. large-cap equity market, returned a total of 228.05% over the trailing ten-year period. However, 174.58% of that was capital gains. The dividends paid out by large-cap stocks accounted for a much smaller 53.47% in aggregate. That means that 23.45% of the total return of the domestic large-cap common stock index came from dividends over the past ten years. This is, admittedly, a historic outlier as historically about 32% of the total return of the S&P 500 Index comes from dividends. According to Investopedia:

Since 1926, dividends make up approximately 32% of the returns of the S&P 500, while appreciation makes up the remaining 68%.

While 32% is not a low figure, the fact that the S&P 500 Index only yields 1.33% today means that it will be very difficult for any equity fund to provide a high level of current income. The fund’s desire to provide current gains makes more sense, especially considering how quickly common stocks can appreciate during a bull market. However, most people consider common stocks to be long-term plays and as such long-term capital appreciation (or total return) is probably the best objective for any equity closed-end fund.

With that said, many of Eaton Vance’s equity closed-end funds do not simply buy a portfolio of stocks and hold them for long-term capital appreciation. The Eaton Vance Risk-Managed Diversified Equity Income Fund is no exception to this. As is the case with most Eaton Vance funds (and a common complaint of mine), the website does not provide any insight into the strategy that this particular fund employs. However, the fund’s annual report includes a pretty good description:

Under normal market conditions, the Fund’s investment program consists primarily of owning a diversified portfolio of common stocks and employing a variety of options strategies. The Fund seeks to earn high levels of tax-advantaged income and gains by (1) investing in stocks that pay dividends that qualify for favorable federal income tax treatment, (2) writing (selling) put options on individual stocks deemed attractive for purchase, and/or (3) writing (selling) stock index call options with respect to a portion of its common stock portfolio value. To reduce the Fund’s risk of loss due to a decline in the value of the general equity market, the Fund intends to purchase index put options with respect to a substantial portion of the value of its common stock holdings and stocks subject to written put options.

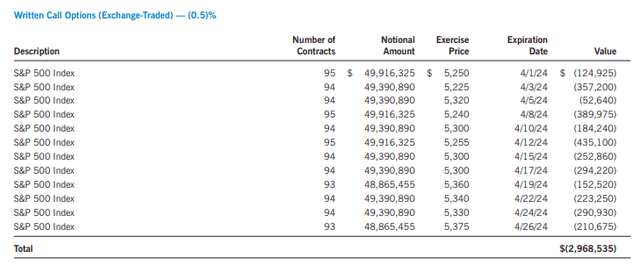

This is a fairly unique investment strategy, and it is very different from that of covered call funds. Indeed, this fund is not writing covered call options at all, despite the Morningstar Classification stating that it does. The fund is writing call options on an index without actually owning the actual index. The first-quarter 2024 holdings report states that these are entirely S&P 500 Index call options:

First Quarter 2024 Holdings Report

The fund only owns 56 stocks, though, so it definitely does not have sufficient holdings to duplicate the index. The fund is therefore writing naked call options, similar to Eaton Vance’s other option-income funds.

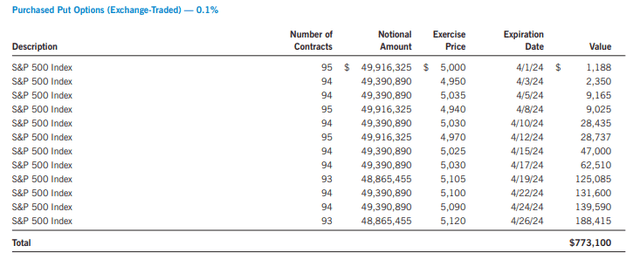

However, the Eaton Vance Risk-Managed Diversified Equity Income Fund is doing something that the manager’s other option-income funds do not. It is purchasing put options against the S&P 500 Index:

First Quarter 2024 Holdings Report

This is a modified form of the options strategy known as a protective collar. As Investopedia explains:

A protective collar strategy is performed by purchasing an out-of-the-money put option and simultaneously writing an OTM call option (of the same expiration) when you already own the underlying asset. This strategy is often used by investors after a long position in a stock has experienced substantial gains. This helps investors to have downside protection as the long put helps lock in the potential sale price. However, the trade-off is that they may be obligated to sell shares at a higher price, thereby forgoing the possibility of further profits.

The fund does not already have the underlying asset (the S&P 500 Index) so its strategy is not an actual protective call. As we can see in the two images above, though, the call and put options in the fund’s portfolio do have the same expiration date. The fund is also buying the put and writing the call.

The unfortunate problem here is that the written call option is still naked. Thus, the fund can have potentially unlimited losses if the S&P 500 Index goes up quickly. The fund appears to be trying to mitigate this risk by only writing options that expire within a few weeks at most (at the end of March, all of the options that this fund held expired before the end of April), but it is possible for the S&P 500 Index to move very rapidly in a month’s time. For example, in November 2023, the S&P 500 Index went up 8.62%.

The S&P 500 Index can also decline very rapidly. For example, the index declined 20.05% in March 2020. The fund’s put options protect it against events such as this, though. This is an advantage that this fund has over Eaton Vance’s other option-income fund offerings. The real risk here is that the market will appreciate too rapidly and cause the fund to take losses on the naked short-call options. It seems that rapid declines are much more common than rapid market gains, however. The largest one-month gain in recent years was the 12.68% gain in April 2020. There have only been two months in the past five years in which the S&P 500 Index gained more than 10%:

YCharts

The largest one-month gain in the S&P 500 Index since 1950 was 16.30% in October 1974. We note in the chart above that April and November 2020 were the only two months in the past five years in which the S&P 500 Index gained more than 10%. The first of these came in response to the CARES Act of 2020, which was the largest fiscal stimulus package in U.S. history. That naturally resulted in a flood of newly printed money entering the economy and the market. In November 2020, there was very promising data coming out from Moderna (MRNA) and Pfizer (PFE) with respect to their COVID-19 vaccines that resulted in investors becoming optimistic that the pandemic would soon be over. In addition, there was speculation about a second fiscal stimulus package that almost certainly drove some of the market gains. In short, we can see that huge one-month stock market gains are not a regular occurrence, and as such the risk that this fund’s naked call-writing strategy poses is probably pretty low. However, it is not something that should be completely ignored.

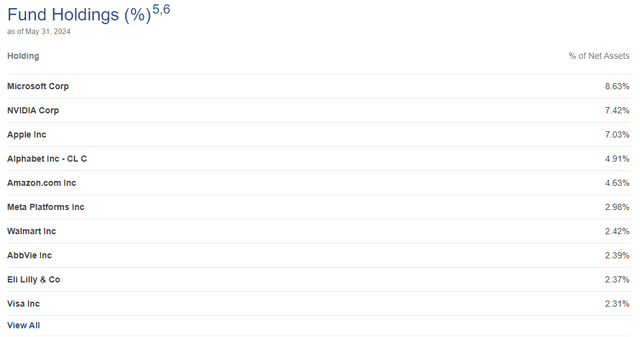

In the previous article on this fund, I pointed out that the portfolio was very concentrated around technology and pharmaceuticals. This continues to be the case today. Here are the largest positions in the fund:

Eaton Vance

Many of these holdings are the same as they were the last time that we looked at this fund. There have been a few changes, though. The most important of these is that TransUnion (TRU) was removed from the largest positions list. In its place, we have Visa (V). The remainder of the companies are the same as the last time that we discussed this fund, but the weightings and order have changed.

It is rather surprising that we see Visa replacing TransUnion, as TransUnion has outperformed Visa rather substantially over the past three months:

Seeking Alpha

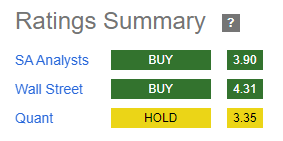

We can clearly see that, unlike the rest of the market, TransUnion and Visa have both declined since the publication date of the previous article on this fund. However, Visa has declined to a much larger extent. The fact that we now see Visa on the largest positions list must mean that the fund managers actively bought shares of the company at some point during the past few months. They might be speculating that the company will rebound, which I suppose is possible. Visa is pretty highly rated by both Seeking Alpha analysts and by Wall Street analysts, as both have assigned “Buy” ratings on the stock:

Seeking Alpha

However, the Quant tool is less fond of Visa, due mostly to the stock’s very high valuation. As of right now, Visa has a very high forward price-to-earnings ratio of 26.35 compared to the 24.05 forward price-to-earnings ratio of the S&P 500 Index. The company might be facing some pressure from Congress too, as the Credit Card Competition Act keeps being reintroduced into Congress, and it would almost certainly have an adverse effect on Visa’s business if it passes. So far, the bill keeps getting defeated, but there is no guarantee that some future Congress will not take it up and pass it. Thus, the risk should not be overlooked, even though many articles on Visa in the financial media seem to ignore it.

The basic objective of the fund’s portfolio seems to be to at least try to match or outperform the S&P 500 Index with fewer stocks. This is pretty much necessary because of the naked short calls, as the fund would need to make sure that it earns enough investment profits from its stock portfolio to cover any potential losses that might come from this strategy. This certainly explains why the fund has such a high concentration of technology stocks in its largest positions, as these stocks account for an outsized proportion of the S&P 500 Index. While this makes sense given the fund’s strategy, it does mean that investors who are looking to reduce their own exposure to the “Magnificent 7” stocks or to the mega-cap American technology stocks will probably not be happy with this fund’s portfolio.

Distribution Analysis

The primary objective of the Eaton Vance Risk-Managed Diversified Equity Income Fund is to provide its investors with a very high level of current income and current gains. As is the case with most closed-end funds, it aims to deliver on this objective by making direct payments to its shareholders. To this end, the fund makes a monthly distribution of $0.0651 per share ($0.7812 per share annually) to its investors. This gives the fund an 8.90% yield at the current stock price.

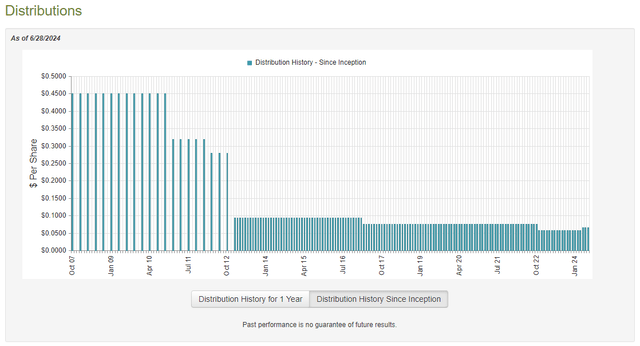

The fund’s distribution history is overall rather disappointing, as it has declined over the years:

CEF Connect

As I stated in the previous article on this fund:

This is a trend that could prove objectionable for those investors who are seeking to earn a safe and consistent income from the assets in their portfolios. The fund has obviously failed to do that, although it does appear to try to keep the distribution stable over multi-year periods, such as the extended stretch that lasted from early 2017 until late 2022. The fund still reduced the payout in 2022 though, which was a period of high inflation. A distribution cut during an inflationary period is the last thing that income-focused investors want, since it serves as a double hit to their well-being. After all, inflation is already reducing the standard of living that can be obtained with a given level of income, and then the distribution cut comes along and reduces income. Thus, the fund’s investors and potential investors have a reason to be rather put off.

The fund increased its distribution back in April, which was rather nice. However, the new distribution of $0.0651 per share monthly is still below the $0.0760 per share monthly distribution that the fund was paying out prior to the 2022 cut. Thus, the trend of declining income over time remains intact.

In the previous article on this fund, we saw that the Eaton Vance Risk-Managed Diversified Equity Income Fund fully covered its distributions for the full-year 2023 period. The fund has not released its financial statements for the first half of 2024 yet, so there is no point in repeating our analysis.

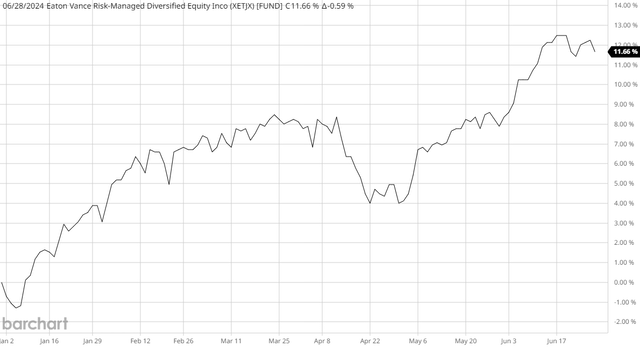

With that said, it does appear that the fund did successfully cover all of its distributions for the first half of 2024. This chart shows the fund’s net asset value since December 29, 2023:

Barchart

As we can see, the fund’s net asset value has increased by 11.66% since the start of this year. That tells us that the fund has managed to earn sufficient investment profits to fully cover its payouts and still has quite a bit left over. In other words, it does not appear that the increased distribution is presenting a burden on this fund, and we should not need to worry about a distribution cut.

Valuation

Shares of the Eaton Vance Risk-Managed Diversified Equity Income Fund are currently trading at a 6.96% discount to net asset value. This is slightly more expensive than the 7.17% discount that the shares have had on average over the past month. Thus, it might be possible to obtain a better price by waiting for a little bit, but overall today’s price is not too bad.

Conclusion

In conclusion, the Eaton Vance Risk-Managed Diversified Equity Income Fund is a unique option-income fund that risk-averse investors might appreciate. The fund’s strategy serves to protect it against market crashes and similar events that some investors dread. Unfortunately, the fund’s portfolio is not nearly as diverse as it claims, and it is exposed to losses if the S&P 500 Index appreciates very rapidly. Such rapid price appreciation is very rare, but it does happen, and that is a risk that should not be ignored. The fund’s heavy exposure to the mega-cap technology companies is also something that could be problematic due to the fact that pretty much every American investor already has substantial exposure to these companies. If we can get past those problems, though, this is one of Eaton Vance’s better option-income funds.

Read the full article here