Investment thesis

Whether things are measured from an economic point of view or whether things are measured in terms of the evolving global geopolitical situation or in terms of political stability, the situation is arguably starting to look shaky in the EU. Short ETFs can provide well-timed opportunities to take advantage of any particular asset seeing a downturn in fortunes. The one asset that I am looking at, which I regard to have a very high probability of seeing a severe downturn, in the near future is the euro currency. The ProShares UltraShort Euro ETF (NYSEARCA:EUO) is one way to place a well-timed bet against the euro currency asset and potentially see some impressive short-term returns if the timing of the trade is right. This potential opportunity could appear within a matter of months.

About the EUO ETF

The EUO ETF is set up to provide a 2x inverse return on the movement of the euro currency versus the US dollar. In other words, when the euro declines 1% versus the dollar, the fund goes up by 2%.

EUO share price chart (Seeking Alpha)

There are a number of factors that make this ETF a short-term bet only, including the expense ratio of just under 1%. The net effect of the daily moves of an amplified ETF also makes it arguably risky to hold for the long term. For instance, in case my thesis is wrong, and ECB rates will keep pushing higher relative to the US Federal Reserve’s own rates, pushing the euro 30% higher over a 5-year period for instance, this ETF will go down about 65% in value. That is about a 60% decline in the share price, in addition to about a 5% loss in fees. In other words a share today at just under $29 will be worth just over $10 five years from now. The fund would then have to more or less triple the price for investors to ever recover their investment. In other words, there is little chance of investors recovering their investment after riding out a 30% increase in the value of the euro relative to the dollar. It is very different from holding on to ordinary stock in a company.

The threats to the long-term viability of the euro currency are growing exponentially

Since the launch of the euro more than two decades ago, there have always been doubters about the long-term viability of the project. Its biggest test arguably came in the aftermath of the 2008 financial crisis, which in Europe morphed into a euro sovereign debt crisis. The cracks that appeared a decade ago were largely papered over since then. However many of the root problems, such as the fact that the euro is perpetually too strong for some euro currency member states to thrive, while it is perpetually too weak to reflect some of the export-oriented economies such as Germany & The Netherlands are still prevalent.

The fact that the EU managed to muddle through those problems provides supporters of the project with a powerful talking point, whenever anyone raises fresh doubts about the long-term viability of the euro. The argument goes that since there were many doubters then and they were wrong, they must always and forever be perpetually wrong, regardless of whether the old root problems were resolved or not, or whether or not the eurozone is ready to face new problems that are arising.

The problems that the EU’s common currency is facing are multiplying and intensifying in terms of severity & magnitude. This comes in addition to the already-existing structural problems I already touched on that are still prevalent. The following list represents just a sample:

- EU low-yielding debt on the books.

A problem that we first saw surface in the US, namely that of low-yielding debt assets on the books of a number of banks, is probably lurking below the surface in Europe as well. We should keep in mind that interest rates were even lower in the EU than they were in the US for the past decade. An FT article highlighted this problem as being a potentially destabilizing factor for the EU banking industry.

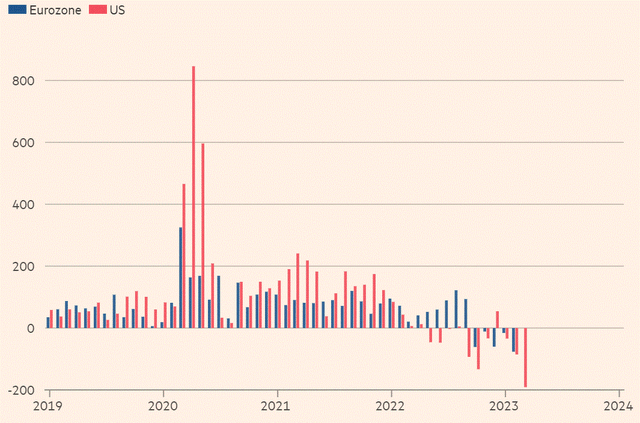

The danger I see in Europe is the fact that EU consumers are being squeezed in terms of negative real wage growth harder than they are in the US. This problem is arguably reflected in a decline in net aggregate deposits.

Aggregate bank deposits (FT)

While the problem surfaced more prominently in the US, with a number of high-profile bank bailouts, my view is that European households are likely to dip into their savings in order to keep themselves afloat as they are more likely to face utility price hikes in the coming winter, higher food prices, and higher overall prices, since inflation is still running at a significantly higher rate in the EU than in the US. On the other hand, the ECB has nowhere near as much room to at the very least pause rate hikes as the US Federal Reserve does, because inflation is still running hot at 5.5% in the euro area, compared with the fresh printout of 3% in the US.

Rising interest rates in the EU mean that old debt, like negative-yielding German 10-year bonds that were issued in the past decade, will depreciate significantly on the books of financial institutions. If EU consumers start to accelerate the withdrawal of their savings from banks in order to make ends meet, or in order to invest the money in something that might help to keep up with inflation, banks will have to sell those low-yielding bonds and other debt assets at a loss given that low-yielding debt is now unattractive. This can lead to massive banking sector defaults in Europe, which will prompt governments to engage in debt-financed bailouts. The ECB will then have to reverse course, even if it means losing control of inflation, in order to support debt issuance in euros.

The combination of the ECB lowering interest rates, even as inflation continues to surge, while EU governments is potentially forced to access the bond markets for extra funds in order to bail out the banking sector has the potential to crash the euro currency. The timing of such a hypothetical event occurring is very uncertain, if it will happen at all. If it does, things could potentially get out of control, with no real limit on how low the euro can go. It can potentially even go to zero in the event that things get really bad and it is abandoned in favor of EU nations returning to their national currencies. I am sure that a grace period where people would be able to convert their euros would be made available, after which it can just disappear.

- The EU will always be a harsh winter away from a severe energy crisis.

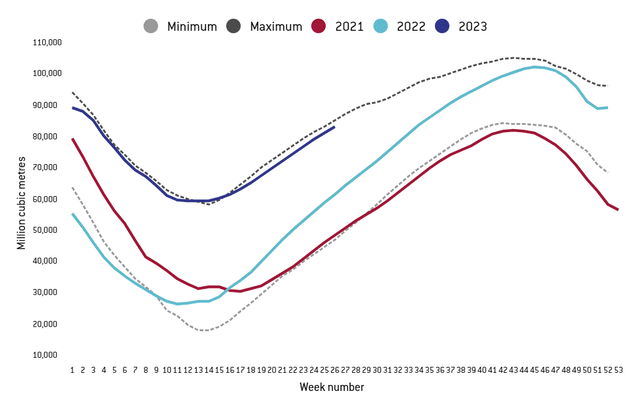

After last year’s panic buying of LNG at any price, as well as a very mild winter, the EU ended the winter heating season with nearly enough gas in storage to be able to comfortably start the next heating season.

EU natural gas inventories (Bruegel)

With the market focused mostly on inventories, it seems to be missing the underlying trend picture. The EU is currently adding about 1 Bcm of natural gas less per week than it did last year on average. The situation is seen as being normal at the moment, given that if it were to fill its facilities at the same pace as it did last year, by around the end of August all facilities would be near 100% filled to capacity.

The problem I see arising is when the massive seasonal surplus in stored supplies will diminish, which will happen at some point in the fall if the current trend continues. In other words, the EU will have to start bidding for about an extra 1 Bcm/week in extra supplies as early as this fall, at which point, we will see a return to the sharp natural gas spot price spikes we saw last year. That in turn can lead to a sharp drop in the value of the euro.

- An almost endless list of risk factors that can negatively impact the euro currency.

While I cannot focus on them all, as I have with the previous two factors that I chose to analyze in more detail, there are many other potential factors that put the future of the value of the euro currency into doubt. These factors can occur in conjunction with each other or together with the two major sources of danger I already highlighted.

There is rising political risk in the EU in my view. The collapse of the Netherlands’ governing coalition is perhaps the latest symptom of growing public discontent across the union. The coming election will see a new farmer’s party that just emerged in the past year or so take first place, based on the latest polls. German polls show the anti-establishment AfD in second place now, just a few points away from the long-dominant CDU which is in first place. In France, President Macron is shown to be losing by a wide margin to the anti-establishment hypothetical candidacy of LePen if elections were to be held today.

There seems to be growing disillusionment all across the board in Europe with the long-term cumulative effects of environmental policies on the economy, as well as the negative effects that the EU endured in the past year due to the Ukraine conflict, and the resulting economic war with Russia. There is also rising friction among nations. For instance on the migration policy issue, where it seems regardless of what is proposed there will never be unity. Then there is the misguided, short-sighted decision to tie funds from the EU budget to the internal affairs of certain nations like Hungary & Poland, where they are currently being denied EU funds. It is short-sighted in my view, because I don’t believe that these countries will cave to the arguably ideological demands made on them. However, any new budgetary decisions will need to gain their consent. We may be headed for a situation where the EU will not be able to pass new budgets or be able to make amendments to the current one.

There is a rebellion of sorts we are seeing against the Western-dominated global financial system arguably taking root. The economic & financial sanctions on Russia seem to have been the triggering factor. In the past year, we have seen not only Russia but also China, Brazil, and India taking very notable steps in the direction of setting up facilities meant to encourage the bilateral use of local currencies in trade. Much of the focus is on “de-dollarization”, but in my view, the euro might end up being the more likely currency to be dumped in favor of alternative options. The US dollar is far too entrenched in the international fiat currency system to be easily discarded. The euro on the other hand is expendable. The fact that Russia is set to stop accepting both dollars & euros for its exports is in my view a major long-term blow to the euro currency in particular. All major net importers of Russian exports could potentially end up reducing their euro FX holdings in response, which could in theory trigger an emerging trend of certain countries refusing to accept euros as payment.

The list of potential pitfalls for the euro currency is virtually endless. We could add the high sovereign debt level that many countries in the South of the EU have as a potential re-emerging cause for crisis, which could in theory explode at any moment. We have the decline in economic growth, which could prompt the ECB to give up on its inflation-fighting policies and opt to defend economic growth, at the price of higher inflation and a plummeting euro currency. There are also potentially unforeseen events that could emerge, which is not uncommon when an economy tends to show signs of significant fundamental ailments.

Investment implications

There is no clear incentive at the moment to buy shares in the EUO ETF. I expect the USD/euro exchange rate to remain stable over the summer, or even see an improvement in the euro’s value relative to the dollar. Things may start to look different by the fall, especially if a harsher-than-average plunge in temperatures will start to drain Europe’s currently more than ample gas reserves. Beyond that, there is growing evidence of political fallout caused by declining living standards in the EU, as well as many other factors I mentioned, or did not mention, which could come into play. The EUO ETF is a good short-term investment opportunity to keep an eye on, as we watch the overall economic, political, and geopolitical situation of the EU within the broader world arguably continue to deteriorate. If or when an opportunity will arise, a well-timed entry & then exit could potentially yield decent positive results for investors.

Read the full article here