Even as electric vehicle (“EV”) demand grows, EVgo, Inc. (NASDAQ:EVGO) has hardly made any progress towards being profitable. The EV charging station business remains bleeding edge, leaving shareholders subsidizing losses for EV users. My investment thesis remains ultra Bearish on the stock, even close to the all-time lows below $4.

Source: Finviz

Mounting Losses

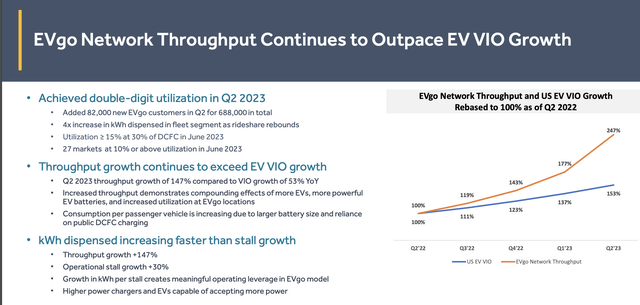

One of the biggest issues facing EV charging networks is the pressure to add additional charging stations, though the current chargers aren’t highly utilized. With the Q2’23 earnings report, EVgo highlighted how the current charging stations struggle to reach even 10% utilization.

Source: EVgo Q2’23 presentation

The company suggests 70% of DCFC stations are utilized less than 15% of the time. EVgo has seen explosive growth in kWh usage, reaching 24.9 GWh in Q2, but it hasn’t changed the financial picture of the business.

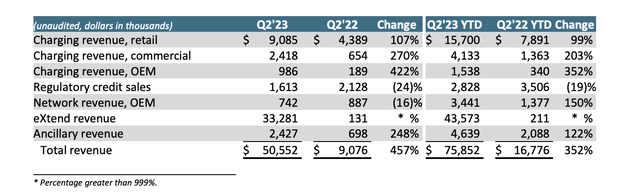

EVgo reported Q2’23 revenues hit a record $50.6 million, but the company still reported an adjusted EBITDA loss to $10.6 million in the quarter. In addition, the revenue level isn’t sustainable with limited revenues from actually charging vehicles.

All of the revenue growth came from the eXtend business, which went from only $0.1 million to $33.3 million in Q2. The key charging revenues were up slightly above 100% for a quarterly total of only $12.5 million.

Source: EVgo Q2’23 earnings release

The eXtend revenue is generally all pass-through equipment costs with OEM partners. EVgo only reported adjusted gross profits of just $12.9 million in the quarter and those revenues are set to disappear in the 2H due to lack of Build America, Buy America compliant chargers for the Pilot and Flying J locations in collaboration with General Motors (GM).

EVgo has announced the first shipment of 10 350kW fast chargers manufactured under the new standards in early September. The company wasn’t clear on how many, if any, will be installed this year.

The company guided to 2023 revenues of only $120 to $150 million due to the eXtend revenues being pushed out into 2024. EVgo has already produced 1H revenues of $76 million, with the forecast that revenues may dip to only $44 million in the 2H.

More Dilution

Clearly, EV charging stations have to be built out before people will purchase EVs, but the big question is why EVgo and other charging station shareholders are paying the upfront costs while diluting shareholders. The business model was flawed from the beginning.

EVgo has to raise $129 million via selling both shares in an equity offering at $4.25 per share and shares via an ATM. The stock only has a current market cap of $1.2 million, causing massive share dilution, and the company hasn’t provided a convincing path to profitability.

At the end of June, the business now has $257 million in cash. The company guided to an adjusted EBITDA loss of $73 million for 2023 after only reporting an EBITDA loss for the 1H of the year of $31 million.

In addition, the company has a new CEO starting in November following the next earnings call. Cathy Zoi is stepping down, with the lead Independent Director taking over the business. New CEOs have a tendency to restructure businesses, or at least adjust the business mode, causing short-term disruption to the business and hitting the stock.

The stock now has a market cap of $1.2 billion while only producing revenues below $150 million this year. The charging revenues are only running at a $100 million run rate, suggesting a very elevated valuation for the stock considering the ongoing losses and weak business model.

The biggest concern is that EVgo currently has ~3,200 charging stalls in operation and construction. The company wants to end the year with 3,400 to 4,000 DCFC stalls, leading to the potential cannibalization of existing stalls.

EV charging stations are one of the few businesses where a company wants to add more locations when utilization rates are very low. Usually, high utilization rates and positive cash flows are the signal and capital used to build the next location.

The company does appear to have the cash for operations into 2025, but EVgo has to solve the charging revenue disconnect with costs.

Takeaway

The key investor takeaway is that investors should continue avoiding EVgo, Inc. Even at $4, the stock is far too expensive for a money-losing business in a tough sector requiring additional funding to buildout a network of charging stations with low utilization.

Read the full article here