I last wrote about Exelon Corporation (NASDAQ:EXC) in January 2024. At that time, I concluded the shares were slightly undervalued and that the company had a stable, growing dividend. I still believe that to be the case for both these factors. Shares are underpriced right now and the dividend has gone up this year.

As a brief review, Exelon Corporation (EXC) is a holding company for six regulated gas and electric utilities serving 10.6 million customers. The total market cap is $34.7 billion, making it the eighth-largest public utility, just behind PG&E Corporation (PCG). Notably, Exelon claims to have the largest transmission system in the country. Its current S&P credit rating is BBB or lower investment grade. Exelon’s utility subsidiaries include Baltimore Gas & Electric (BGE), Commonwealth Edison (ComEd), Philadelphia Electric (PECO), Atlantic City Electric (ACE), Delmarva Power (DPL) and Potomac Electric Power (Pepco or PHI). BGE, DPL, and PECO have both gas and electric operations; the other utilities are purely electric. This is a utility focused on urban areas: Philadelphia, Baltimore, Washington, D.C. and their suburbs, and Chicago. The regulatory environment in all these areas is relatively favorable, except Illinois, which remains thorny and is continuing to hold back the company’s returns, as it represents 37.0% of the rate base.

Exelon Territory (2023 Annual Report)

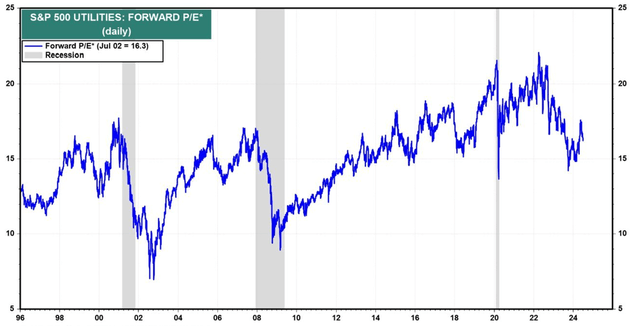

In January, Exelon’s price was $35.90 and I estimated the value at around $40 per share. Since then, the stock hit a six-month high of $38.73 in May of 2024, but as of July 5, it’s back down to $34.31 per share. The dividend was increased this year to $0.38 per quarter from $0.36, for a yield of 4.4%. The beta of the stock is 0.59, so it is significantly less volatile than the overall market, but Exelon has generally tracked the utility sector overall, reacting to the possibility of rate cuts (or not) by the Fed. According to Morningstar, over the last few years “the utilities sector took investors on a wild ride, crushing the market in 2022 and getting crushed in 2023. But most of the pain is over.” October 2023 was the low point, and while the sector has rebounded, it is still trading just below its 20-year average P/E of 16.7. There are still utility values to be had and Exelon is one.

Transmission Only, for Better or Worse

At the beginning of 2022, Exelon spun off its power generation group, Constellation Energy Corporation (CEG). Exelon shareholders received one share of CEG for every three shares of Exelon they owned, and the company’s basis after the split was 70.0 percent of what it was before. The goal of the spinoff was to even out the company’s earnings and make them more predictable year by year, as a pure transmission play. Exelon no longer has to worry about complying with the Inflation Reduction Act of 2022, and its goals of reducing greenhouse gasses 40% below 2005 levels by 2030. But now it is subjected to buying energy in the open market or through pre-negotiating contracts.

2023 and Q1 Earnings as Expected

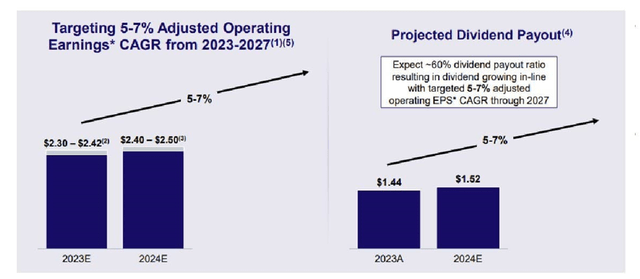

Last year, the estimate for 2023 non-GAAP earnings was $2.30 to $2.42 per share. Year-end earnings came in at $2.38, up 4.8% from $2.27 in 2022. The early estimate for 2024 earnings is $2.40 to $2.50 per share, so on average 3.0% higher. Earnings growth is now estimated by Exelon at 5-7.0% per year moving forward, versus the 6-8.0% estimate of last year. This has been a common trend for utilities in today’s higher interest rate environment. 2023’s increased earnings were largely due to higher electric revenues from better regulatory return on equity, with rate increases at PECO, BGE, and PHI, and even a slightly higher rate base at ComEd.

At the end of the first quarter of 2024, earnings were $0.68 per share versus $0.70 per share in Q1 2023. Earnings would have been $0.03 per share higher, but the Q1 Investor Presentation cited added interest expense from higher rates, the cost of repairs from winter storms, and a warmer winter overall. This was particularly the case in Illinois where temperatures averaged 4-7 degrees above normal this winter.

Earnings per Share, Growth (Spring 2024 Investor Presentation)

Dividend Track Record Starts in 2022

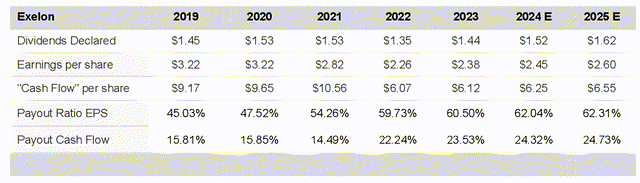

Without Constellation Energy, Exelon’s dividend track record really starts in early 2022. The dividend began at $0.338 per quarter then jumped to $0.36 per quarter in 2023 (up 6.5%), then $0.38 per quarter in 2024 (up another 5.6%). The yield is currently 4.4%. The logical increase for 2025 would be $0.40 (+5.3%) or $0.41 (+7.9%). Exelon has pledged to increase the dividend by 5-7.0% per year through 2027, with an estimated 60.0% payout ratio. This appears to be easily sustainable, in earnings and cash flow, as illustrated below:

Payout Ratio Over Time (Value Line and Author Calculated)

The payout ratio based on cash flow per share is in the 20.0% range, and earnings per share are around 60.0%, even after the departure of Constellation Energy. According to Edison Electric Institute’s 2023 Industry Report, the average industry payout ratio is 64.2% while the average sector yield for 2023 was 3.8%, so Exelon is ahead in both these metrics. Of course, the current treasury yield is 5.30% for 6 months, so you have to count on either lower treasury/money market rates in the future, or share price appreciation, or both to come out ahead.

So, What are Shares Worth Now?

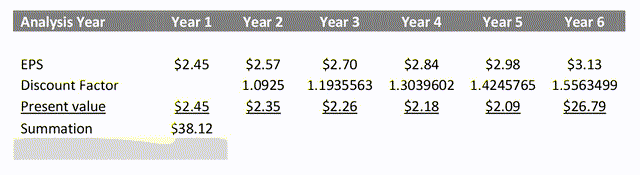

My current estimate is $38.00 per share, lower than the $40.00 I projected in January. This is mostly due to the lower 5-7.0% growth rate. I’ve valued Exelon’s shares here using two methods: a discounted cash flow and a P/E multiple comparison. The projected range of earnings is $2.40-$2.50 for 2024, so I chose the mid-point of $2.45. Again, annual EPS growth has been lowered to 5-7.0% annually, from 6-8.0%, and I’ll use 5% for this factor (I used 6.0% in January). As a discount rate, I used 9.25%, near the average annual return of the S&P 500, which approximates 9.8%. The reversion rate was 7.5%, so the value by discounted cash flow is $38.12 per share.

Discounted Cash Flow (Author Calculated)

To do a P/E-based valuation, I consulted Yardeni Research, which tracks the utility sector. The industry-wide P/E ratio was 16.3 as of July 2. At a $2.45 per share earnings estimate for 2024, and the current industry P/E ratio of 16.3, the valuation would be $39.94 slightly above the DCF. I am concluding here at a value equal to the discounted cash flow, as it incorporates more data over time. So, at the July 5 price of $34.31, shares are still about 10.0% undervalued, based on my updated $38.00 estimate.

Utility Sector P/E Multiple (Yardeni Research)

Illinois Regulators are Exelon’s Problem

Standard & Poor issued a utility research note in May of 2024, which stated that “the average ROE authorized for electric utilities was 9.60% for rate cases decided in 2023, up from the 9.54% average observed in the full year 2022. The average ROE authorized for gas utilities was 9.64% for cases decided in 2023, up from the 9.53% average observed in the full year 2022.”

Exelon is doing well compared to these benchmarks everywhere except Illinois. The Illinois Commerce Commission (ICC) set return on equity levels at 8.91% for ComEd, 69 basis points below the national average, and denied Exelon’s multi-year capital expenditure plans. This unfavorable decision came in December of 2023 and the board said that ” Exelon’s grid plans failed to adequately incorporate customer affordability into their proposals or outline how 40% of plan benefits would go to low-income and environmental justice communities, as required by the Climate and Equitable Jobs Act.” They did approve a $259.0 million revenue increase that took effect in January, however.

In comparison, Pepco (Potomac Electric) has a return on equity of 9.55% with an increase request to 10.55% likely to take effect in September 2024. PECO (Philadelphia Electric) has an allowed ROE of 9.5% on electric and 9.65% on gas operations. DPL (Delmarva Power) has an allowed electric return on equity of 9.6% with a requested increase of 10.5% pending. BGE (Baltimore Gas & Electric) has a rate of 9.5% for electricity and 9.45% for gas. DPL (Delmarva Power) has an electric return on equity of 9.6%, with a request to raise this to 10.5%, that should be decided shortly.

Despite the low Illinois return on equity, it should be noted that ComEd rates are decoupled, meaning they are not reliant on the volume of usage. Perhaps when the current board turns over, the return on equity in that state will improve. The Commerce Commission has five governor-appointed members serving staggered five-year terms. Under Illinois law, no more than three Commissioners may belong to the same political party. One member’s term expires in 2026, another in 2027, and three in 2028. But right now, the allowed return on equity in Illinois is 7.2% below the national utility average and I estimated it lowers Exelon’s revenues overall by 5.0%. The ICC issue may be a reaction to a 2020 bribery scandal involving ComEd and Illinois. In this event, Exelon “admitted that it arranged jobs, vendor subcontracts, and monetary payments for various high-level elected state officials to influence and assist the subsidiary with state utility legislation.” Having the ICC grant a higher rate of return right now would not be good optics. Maybe more time will improve the ICC and Exelon relationship.

New AI and Data Centers Will Drive Growth

In a world of milder winter weather and higher interest rates lowering earnings, what will move utility growth going forward, beyond population increases? Between 2013 and 2022, electric demand grew only by 5.0%. But new electric demand types are likely to change this. According to Gabelli Funds “after a decade of flat growth, many US electric utilities and the North American Electric Reliability Council (NERC) are raising previous forecasts to reflect stronger sales growth driven by the growing use of power-hungry technology (artificial intelligence), data centers, electrification, reshoring of manufacturing, and bitcoin mining.” This is now true for Exelon, which is anticipating new data centers in its suburban Philadelphia market, according to its first quarter conference call. Outside Philadelphia, developers are planning a 2.0 million square foot data center. Overall Exelon expects 6 gigawatts of data center growth in its territory over the next few years. Dominion Energy, Inc. (D), American Electric Power Company, Inc. (AEP), and The Southern Company (SO) are all utilities that have benefitted from new data center electric demand, AEP in particular with an 8.0% annual increase in usage.

Capital expenditures will drive growth too. In its markets, Exelon has plans to invest $34.5 billion in capital between 2024 and 2027, in order to upgrade its electric and gas distribution systems to provide more energy and to improve their resilience to climate and cybersecurity issues. A small portion of this money will be funded through grants. In 2021, the Bipartisan Infrastructure Bill was signed into law, providing grant money to utilities to help with these issues. In 2023, the U.S. Department of Energy selected ComEd and PECO to receive $150 million in federal grants to improve the power grids in Illinois and Pennsylvania. Pepco and Delmarva Power have also applied for grants. Part of the money will be used for an “undergrounding cable initiative” for Washington, D.C., so that the most vulnerable overhead distribution lines will survive major storms. In Illinois, ComEd is installing new cables, which can handle 200 times the load of standard copper wire.

So Why Buy Exelon Shares Now?

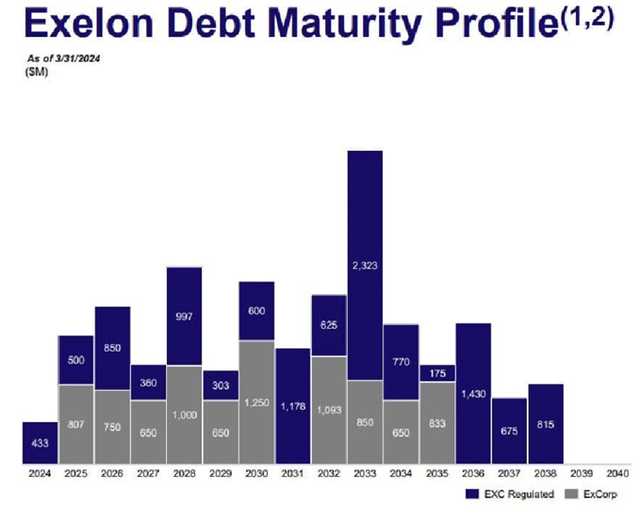

Exelon shares are about 10.0% undervalued at their current $34.31 share price. Since the company’s spinoff of Constellation Energy Corporation (CEG), its income has become more stable, as the company expected. Exelon has increased its dividend by 5.6% to a yield of 4.4% in 2024 and plans to increase again in 2025. I expect this trend to continue as the payout ratio is easily managed. While the 4.4% yield is below current treasury rates, the Fed is likely to make one rate cut this year, making the dividend relatively more attractive. Given the location of Exelon’s utilities in urban and suburban areas, growth in energy demand in its markets is likely through new data centers and we already have evidence of this in Pennsylvania. So, there is a probable demand upside here, along with the possibility of improvement in the Illinois Commerce Commission’s point of view, which could not get any worse. This is an east of the Mississippi utility for diversification, and the amount of debt that has to be refinanced at current high interest rates is low, as shown below. In short, there is a lot of upside potential to Exelon.

Debt Maturity by Year (Spring 2024 Investor Presentation)

Risks to Outlook

The risks to my outlook remain the same as in January. Exelon is now a transmission and distribution-only utility and has been since 2022, and this is a positive and a negative. This means it must go to the open market to buy energy, so in periods of peak demand, it may be subjected to surging prices. This is offset by the fact that three-quarters of Exelon’s territory is rate decoupled, meaning ultimately most fluctuations in energy costs will be passed on to consumers. While the unfavorable Illinois regulatory environment is an ongoing problem, the worst-case scenario already exists with one of the lowest allowed return on equity rates in the country. This is already baked into the share price, so any improvement in Illinois will boost revenues and will boost demand from new data centers in Exelon’s largely urban markets.

Read the full article here