Thesis

Exponent, Inc. (NASDAQ:EXPO) valuation indicates the share price performance has exceeded earnings growth with the PE at 46x 2024 earnings. Billable hours increased 2% YoY in 2023, and forecasts for 2024 are low-single digit growth. With a mere $24 million of debt and $168 million of cash on the balance sheet, there is no concern with debt; however, the expected 5-6% YoY decline in headcount suggests revenue growth may continue to slow. I believe Exponent is a good business; however, the valuation is stretched, and I believe there are better investment options, so I will not be adding EXPO to my portfolio at this time.

Introduction

Exponents Business has cornered a very niche area of the consulting market, focusing on specialty areas within servicing a variety of corporations, where a subject-matter expert is required to advise the client. Billable rates range from $200 to an impressive $985 per hour. The business operates across a series of practices with differing specialties across Engineering, Science, Environment and Health disciplines, servicing clients with specialist consultant advisors.

A brief outline of the practices within Exponent Inc. is below:

Engineering & Other Scientific

•Biomechanics

•Biomedical Engineering & Sciences

•Buildings & Structures

•Civil Engineering

•Construction Consulting

•Data Sciences

•Electrical Engineering & Computer Science

•Human Factors

•Materials & Corrosion Engineering

•Mechanical Engineering

•Polymer Science & Materials Chemistry

•Thermal Sciences

•Vehicle Engineering

Environmental & Health

•Chemical Regulation & Food Safety

•Ecological & Biological Sciences

•Environmental & Earth Sciences

•Health Sciences

Business Update

Q2 2024 earnings are scheduled for release on July 25th, and based on the information provided in Q1, forecast low single-digit annual revenue growth for 2024. Full-year utilization of technical staff is expected to be 69.5% to 71.5% as compared to 69.9% in 2023. Q1 2024 posted an improved 75% utilization rate, which should support the impact of the expected 5-6% YoY headcount reduction.

Billable hours for 2023 amounted to 1,495,000 an increase of 2% on 2022’s 1,465,000 hours. The billable hours provide a useful data point to track business progress YoY, and when combined with the 75% utilization rate in Q1, that leaves plenty of room to increased billable hours, management have stated the mid-70s percentage target in 2024 is achievable based on the existing market demand for their services. To achieve the 75% utilization rate across the business in a labor-constrained market could be achieved through headcount reductions, as is expected for the full year 2024; perhaps the billable rates are putting off clients?

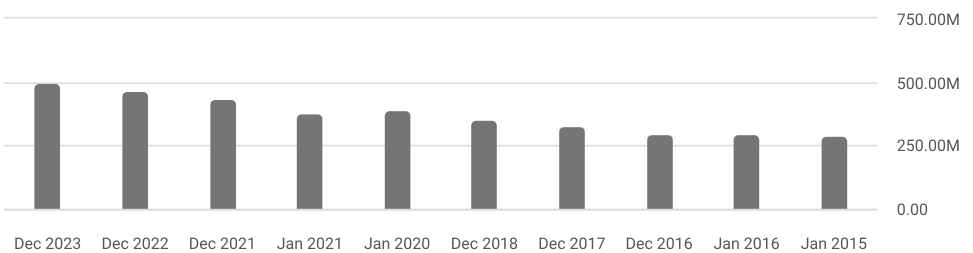

The below chart shows the revenue increasing from $290 million in 2015 to $505 million by the end of 2023, a very respectable 86% increase over 10 years. Nevertheless, a 5.7% CAGR does not substantiate the share price increase and expanded PE ratio over the same period.

EXPO Revenue History (SA)

When compared to the share price growth, it becomes apparent that revenue growth has not kept pace with the share price increase, which returned 409% over the 10-year period.

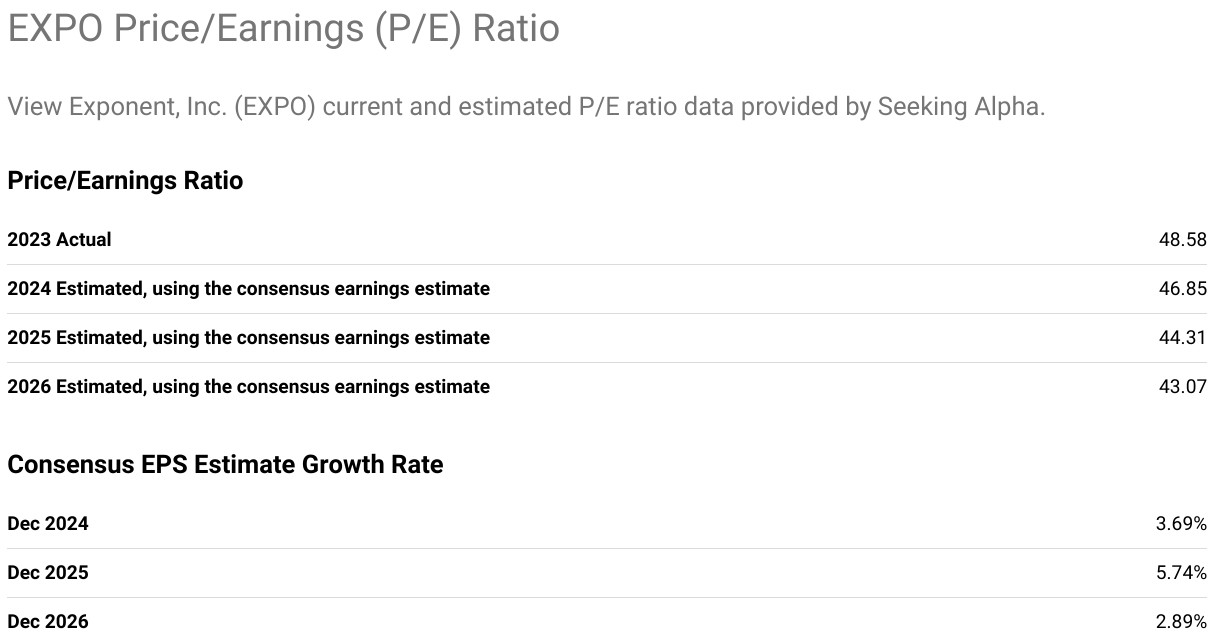

I believe the price-to-earnings ratio expansion to 46x highlights the issue, that the share price has accelerated ahead of the business growth, estimated to be 3-6% over the next 3 years.

EXPO PE Ratios (SA)

While it may seem like I am pessimistic about Exponent, that’s not entirely true. I like the dividend policy: a 1.2% dividend yield, with annual increases of 13.2% over the past five years. The payout ratio is low at 53.5%, leaving room for continued annual increases despite the share price overvaluation. So for those already invested, holding an existing position whilst receiving 13% dividend increases could prove to be a wise decision rather than pay capital gains tax.

Competitors

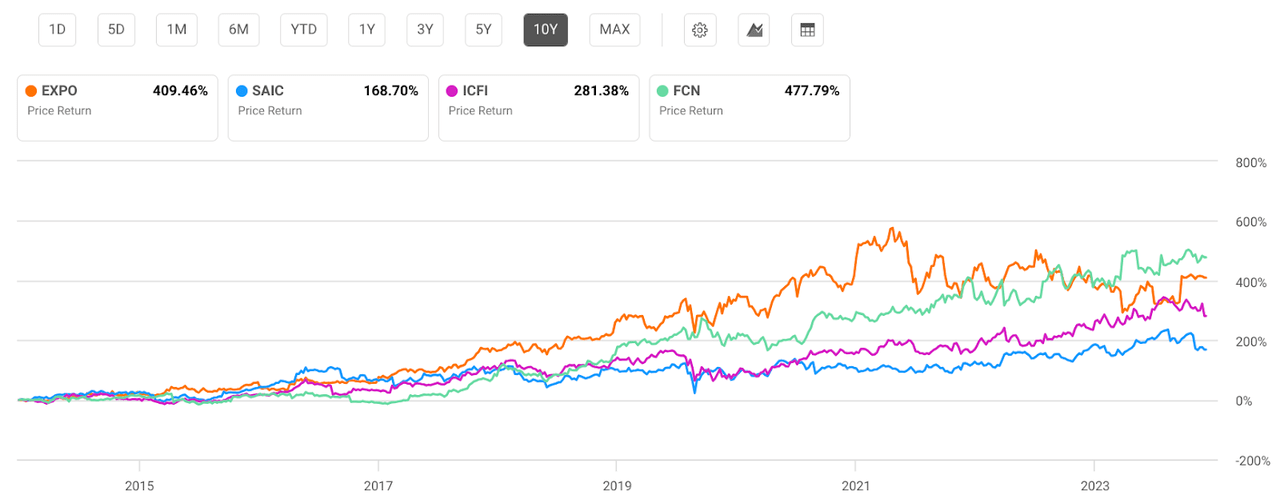

Through benchmarking with their closest competitors, we can see Exponents share price increase has mostly outperformed amongst the group of competitors, which includes; Science Applications International Corp. (SAIC), ICF International, Inc. (ICFI), and FTI Consulting, Inc. (FCN)

Each business competes across various industries, including Energy, Consumer products, Manufacturing, Pharmaceuticals, Transportation, Aerospace and Defense.

Peer Group Share Price Return (SA)

Seeking Alpha’s Quant rating aligns with my view on Exponent’s valuation with an F grade, however profitability has an A rating which stands out among the competition.

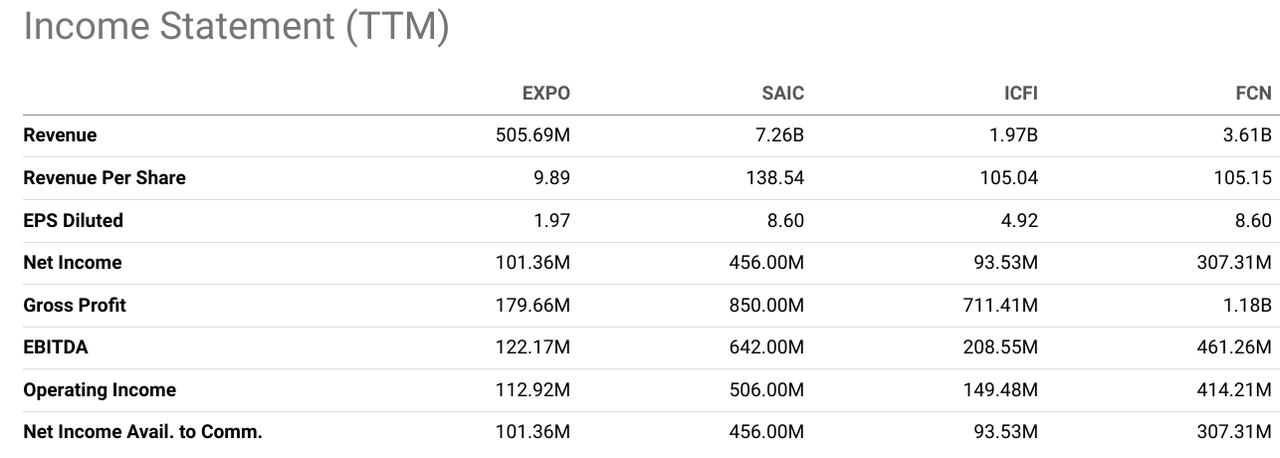

Comparing the income statement, we can see Exponent is considerably smaller by revenue compared to the group. To put the valuation into perspective, Exponent’s market cap is $4.8 billion while Science Applications International Corp. produces over 14 times the revenue and has a market cap of $5.85 billion.

Peer Group Income Statement (SA)

Risks

The availability of skilled and qualified technical employees poses a risk to the business. Talent retention needs to be a top priority for management in order not to lose talent to competitors. The YoY headcount reduction is not good news for Exponent. Although the second half of 2024 is expected to experience improvements. Regardless, headcount reduction is concerning given the difficulty in finding suitably qualified and experienced candidates who also hold a PhD, as is the case for 67% of Exponents technical workforce.

Macroeconomic conditions have caused a wait-and-see approach as elevated interest rates have caused delays in funding release from large corporations as AI capabilities become more apparent and how it will change outsourcing requirements. Exponent typically has a very small order book of billable projects, meaning economic declines can immediately impact revenue, something to bear in mind given the PE of 46x.

Changing client requirements as industries evolve has always been a risk to consulting firms. The advancement of AI has the ability to disrupt the consulting industry. Clients moving from an outsourced consulting model to direct-hire for specific business requirements can impact Exponents business.

Conclusion

From the perspective of existing shareholders, selling seems like the wrong thing to do, as it would likely trigger a taxable event. The dividend looks safe and set to continue its strong growth, with a safe 54% payout ratio. The business in which Exponent operates is difficult, with a highly skilled workforce, replacing staff who depart and growing headcount is an ongoing challenge.

The current utilization rate of 75% in Q1 should help bolster the earnings growth if this can be maintained for the remainder of the year. However, I believe there is a lot of work to be done to maintain this 75% target, with headcount set to decline year over year; nevertheless, the utilization rate indicates the need to reduce headcount in order to improve margins. Based on 2023’s weak growth and low-single digit EPS guidance for the next three years, I rate Exponent a Hold.

Read the full article here